Chukwuemeka ran a printing business in Onitsha. In May 2023, he imported paper and ink from China, paying roughly N460 to the dollar at the official window. By December that year, the same dollar cost him N900. By the end of 2024, it was N1,535. His input costs more than tripled in eighteen months. He raised prices. Clients went elsewhere. He laid off three workers. He is still in business, barely.

His story is not unusual. It sits on one side of the biggest currency reform Nigeria has attempted in a generation. On the other side are reserve figures that have not looked this healthy in 17 years, a monetary policy system that actually works again, and foreign investors who came back in numbers not seen since the oil boom. Both stories are true. Neither cancels the other out.

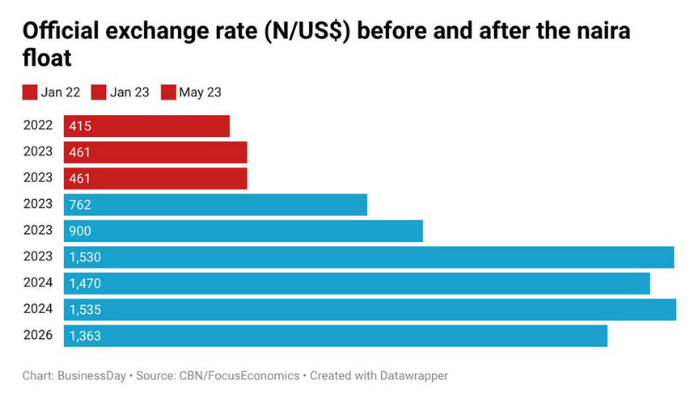

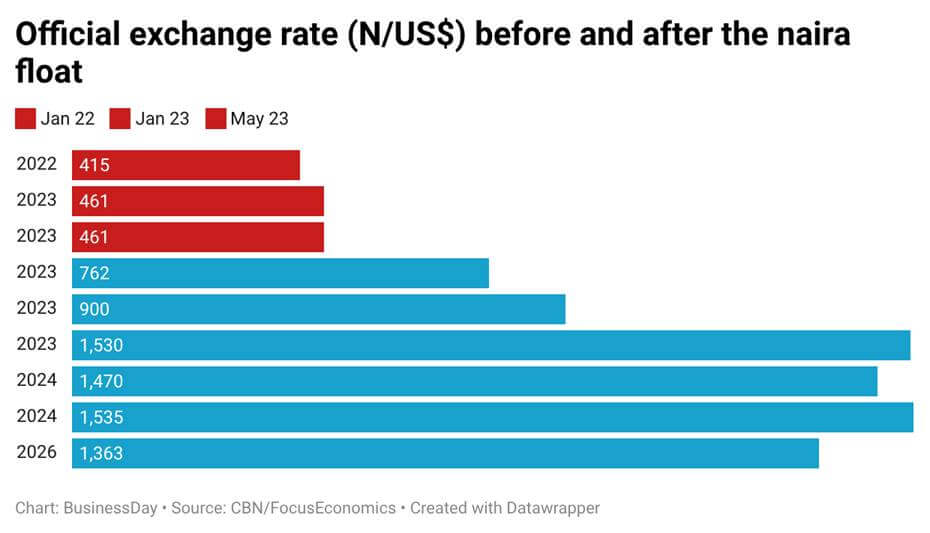

On June 14, 2023, the CBN abolished Nigeria’s tangle of multiple exchange-rate windows and told the naira to find its own price. It found one quickly. The currency moved from N461 to N762 against the dollar in a single session. Three years on, this is what the data show about what that decision delivered and what it cost.

Why the policy was introduced

Nigeria’s FX system by 2023 was one of the most distorted in the world. The official rate sat at N461 per dollar. The street market traded at N740. That 60 percent gap was not just an inconvenience. It was an entire shadow economy: importers round-tripped dollars for profit, fuel was smuggled across borders, businesses bypassed official channels entirely, and foreign companies that had invested in Nigeria found they could not take their money out.

The distortion had been building since 2016, when the CBN introduced a managed float and then refused to let it float. By 2021, the official I&E window averaged N410 to N420 per dollar while the parallel market had crossed N570. Total FX market turnover fell below $35 billion a year, a 40 percent drop from 2018, according to FMDQ 2022 data. The backlog of unpaid foreign exchange owed to companies trying to repatriate capital reached $7 billion. The IMF, World Bank and Moody’s had all called for reform, repeatedly.

President Tinubu declared the fuel subsidy dead on May 29, 2023, and instructed the CBN to follow. Olayemi Cardoso did so on June 14. Every window closed. One market replaced seven. The willing-buyer-willing-seller principle replaced administrative pricing that had created the distortions in the first place.

Did the government deliver what it promised?

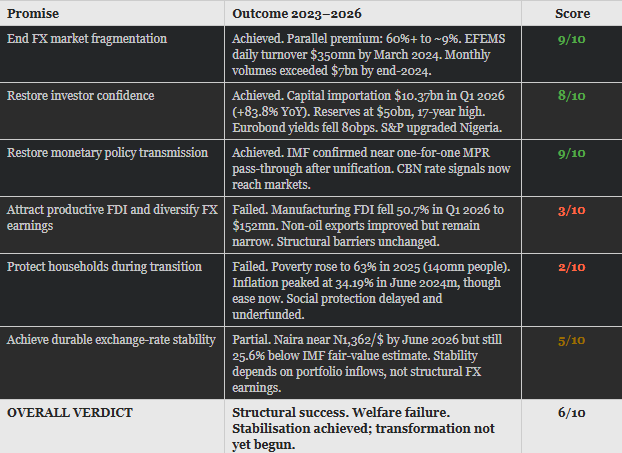

Four things were promised: end the market chaos, bring investors back, make monetary policy work again, and signal to the world that Nigeria was serious about reform. On three of the four, the data support the government’s case.

The parallel market premium, which had run above 60 percent before the reform, narrowed to about 9 percent after unification, according to the IMF’s June 2026 Selected Issues report. The Electronic Foreign Exchange Matching System, launched by March 2024, brought daily FX market turnover to $350 million, the highest since 2014, according to FMDQ 2024 data. By end-2024, monthly volumes exceeded $7 billion. The market was working.

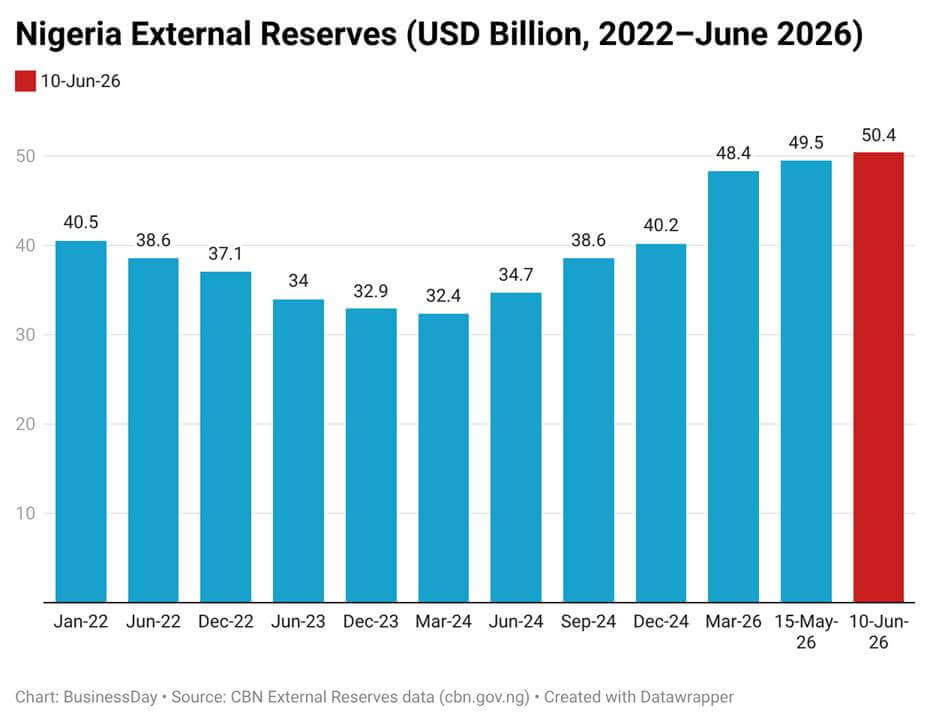

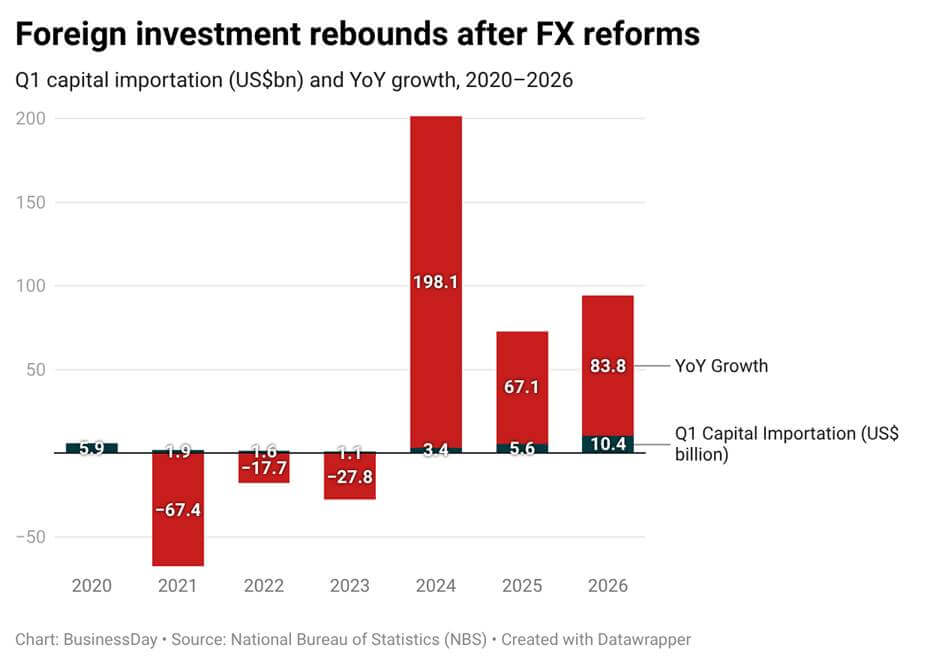

Investors came back. Capital importation reached $10.37 billion in Q1 2026, according to NBS data, an 83.8 percent increase year-on-year. External reserves crossed $50 billion in June 2026, a 17-year high, according to CBN. Nigeria’s 2031 Eurobond yields fell 80 basis points between Q3 2024 and Q1 2025, according to Bloomberg. S&P upgraded the country’s credit rating.

On monetary policy, the IMF’s June 2026 Selected Issues paper delivered the most important finding of the reform’s record: between 2016 and 2023, monetary policy transmission had broken down completely. When the CBN raised rates, commercial lending rates barely moved, because every tightening signal was offset by the FX liquidity injections needed to defend the fixed rate. After unification, the interbank call rate moved in near-lockstep with MPR changes. The central bank got its instrument back.

What was not delivered was affordability. The naira fell from N461 in May 2023 to N1,535 at end-2024, a 233 percent decline, according to FocusEconomics citing CBN data. By mid-2026 the official rate sat near N1,363 per dollar. The IMF’s June 2026 assessment found the naira still undervalued by approximately 25.6 percent against its estimated fair value. Chukwuemeka’s dollar is cheaper to buy than it was at the black market in 2022. It is still three times more expensive than it was at the official window before the reform.

Who won? Who lost?

The winners

The federal government won fastest and most completely. Oil receipts converted at N1,200 to N1,400 per dollar in 2024 generated roughly N12 trillion more in naira than the same oil revenue would have produced at the old N460 rate, according to CBN Fiscal Bulletin 2024. The fiscal deficit narrowed from 6.1 percent of GDP in 2023 to 5.0 percent in 2024, according to IMF 2025 data. FAAC allocations rose to record levels. Exporters benefited: total exports surged 38 percent year-on-year in 2024 to $67 billion, according to NBS 2025, and non-oil exports hit a record $4.8 billion, led by cocoa, cashew and fertiliser, according to CBN Trade Data 2024. Foreign portfolio investors drew $9.86 billion in Q1 2026 alone, chasing treasury bill yields approaching 20 percent.

The losers

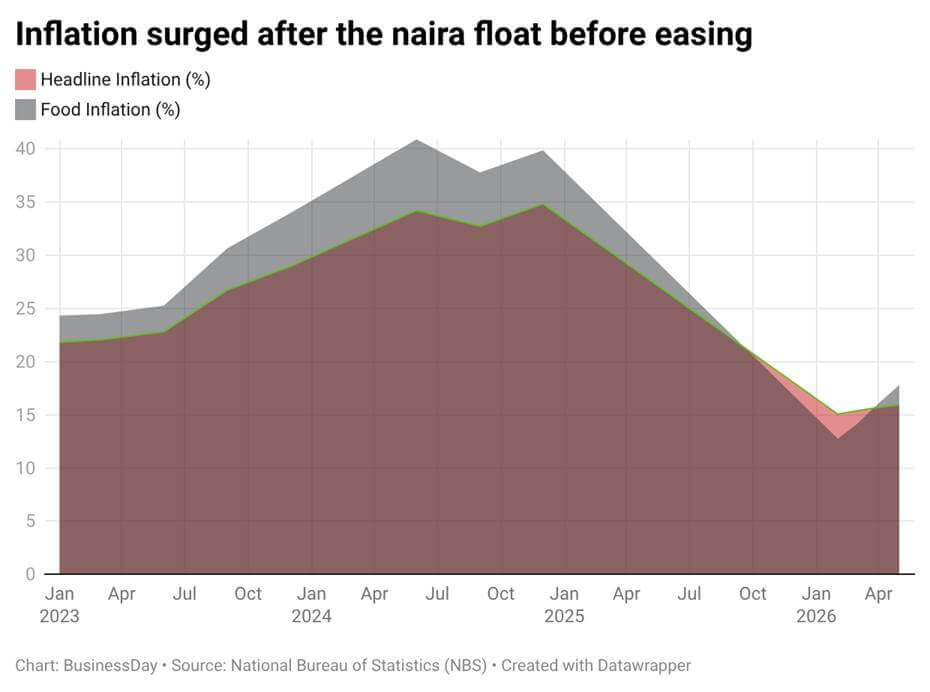

Households bore the cost with almost no cushion. Headline inflation peaked at 34.19 percent in June 2024 according to NBS. Food inflation hit 40.87 percent. The World Bank’s April 2026 Nigeria Development Update put the poverty rate at 63 percent of the population in 2025, approximately 140 million people, even as inflation subsequently fell. Chukwuemeka’s workers earn N120,000 today against N80,000 in 2022, a 50 percent nominal rise against a 200 percent price increase. Small businesses were squeezed from both sides: rising input costs and commercial lending rates between 32 and 37 percent, according to MAN’s June 2026 data. FDI into manufacturing fell 50.7 percent in Q1 2026 to $152.27 million, according to NBS Capital Importation data, because power, logistics and insecurity, the structural barriers that deter serious long-term investors, have not moved.

What the critics get right

Nobody serious argues the old system was better. The criticism is about timing, sequence and what was left out.

Food inflation hit 24 percent immediately after unification and kept rising faster than every other price category. Research by Zakari, Bakkihs and Asue, published in Journal of Economics and Social Research in 2025, put the problem plainly: “exchange rate reform works effectively only in production economies, not consumption economies.” Nigeria fits the second category. When the naira falls, import costs rise sharply. Output does not follow, because the factories that could benefit from a cheaper currency still cannot get reliable power, decent roads or affordable credit to actually produce more.

The IMF was direct in its 2024 Article IV consultation: the reform “imposed significant short-term hardship on households” at precisely the moment Nigeria had almost no fiscal room to absorb it, with a revenue-to-GDP ratio of only 9.4 percent in 2023. Egypt ran the same reform twice, in 2016 and 2022, but each time arrived with IMF financing and cash transfers already covering more than five million poor households. Nigeria moved first and compensated later. Most households are still waiting.

The World Bank put the remaining risk plainly in its October 2025 Nigeria Development Update: the FX market “still heavily relies on inflows from foreign portfolio investors and CBN interventions to stay stable.” Portfolio money is quick to arrive and quick to leave. The reserve cushion is real. The stable rate is real. But both rest on short-term capital flows, not on the export earnings and productive investment that would make them durable.

Policy scorecard: Did the reform succeed?

Naira Float Policy Scorecard (June 2023 – June 2026)

The naira float fixed something that was genuinely broken. An artificial price system that was draining reserves, destroying investor confidence and making monetary policy operationally useless has been replaced with a market that functions. On those measures, the reform succeeded in ways the old system never could have.

But it did not protect the people who paid for it. Poverty rose while the fiscal position improved. The depreciation that boosted government naira revenues destroyed household purchasing power. The interest rates that restored monetary credibility made it impossible for manufacturers to borrow and grow. And the stability visible in today’s reserve figures rests on portfolio capital rather than on the export earnings and productive investment that would make it last.

Three years on, Nigeria has a better exchange rate system. It does not yet have a better exchange rate. Chukwuemeka’s dollar still costs three times what it did. The reform bought the conditions for transformation. Whether it arrives depends on the harder agenda that no exchange rate policy, on its own, was ever going to deliver.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp