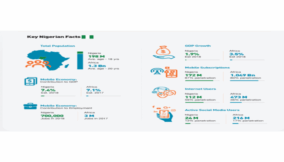

The International Finance Corporation (IFC) estimates that approximately 80 percent of women-owned businesses with credit needs in low-income countries are either unserved or underserved. This is equivalent to a $1.7 trillion financing gap; the difference between funding available and funding needed. Consequently, the global economy does not materialise an annual $330 billion in turnover due to this financing gap.

In Nigeria, there is a 14 percent gap between the portion of men and women that own bank accounts – twice the size globally. While a bank account is a gateway to other financial services, it does not automatically translate into the actual use of or access to these financial services. However, the evidence on the broader inclusion of women into formal finance is disappointing.

All data points in the same direction: the current financial sector landscape, especially in low-income countries and marginalised communities, makes it easier for men to access financial services than women.

For these women, this means the odds are already stacked against the growth potential of their businesses, despite their significant contributions to Gross Domestic Product (GDP) and employment. Women own and lead approximately 40 percent of Nigeria’s 41.5 million micro, small and medium enterprises (MSMEs). MSMEs do not only represent a significant part of the world economy, but they are also one of the strongest drivers of economic development, innovation and employment in Nigeria.

Yet, work for women in African countries is characterised by low-paid and less secure jobs, so that 92.1 percent of women make up employment in the informal sector. Considering that the informal sector contributes about 41 percent of Nigeria’s economic output, there are no labour standards to protect the workers, so exploitation and discrimination are rife, with women feeling the worst brunt of it.

At the same time, women are more intentional savers (with lower loan-to-deposit ratios than men), more prudent borrowers (with lower nonperforming loans than men) and calculated risk-takers. Giving women better access to credit and other financial tools and services is considered a critical enabler to achieving several Sustainable Development Goals (SDGs), including eliminating poverty (SDG 1), reducing hunger and food security (SDG 2), achieving good health and well-being (SDG 3), fostering quality education (SDG 4), promoting gender equality (SDG 5), and equitable and peaceful societies (SDGs 10 and 16). Yet, the potential of women-owned businesses is an investment that is largely overlooked and unexplored.

This persistent financial inclusion gender gap continually challenges the sustainable development of Nigeria. With less than four years left to attain 95 percent Financial Inclusion by 2024, it is time to step up the focus on gender equality and financial inclusion as a driver for positive change for women as well as for our economic growth and development. Regulators view financial inclusion predominantly as an important but largely gender-neutral policy issue. But in reality, access to finance in Nigeria appears to depend on one’s gender.

To borrow from the words of the H&M Foundation, “By not giving women entrepreneurs equal access to finance, investors keep missing out on what could become the new Apple Inc or Amazon.com – every year.” So, this begs this question: How can the government, private sector and key developmental organisations expand financial inclusion and bring more women into the economy?

Leverage digital technology

As we search for a solution to the inequality between men and women in accessing finance around the world, the answer could be simple: digital financial services.

Expanding financial inclusion ensures that women have access to financial tools and services to save for family needs, borrow to support a business (access to credit) and build a cushion against emergency (insurance). Most importantly, expanding financial inclusion ensures that women have the financial knowledge to make the right decisions and improve their economic resilience.

Our world is becoming increasingly more digital and new data by the World Bank Group suggests that mobile phone ownership and internet access show unprecedented opportunities to use technology to achieve universal financial inclusion. The proportion of Kenya’s population with access to formal financial services rose to 83 percent in 2019 from 75 percent in 2016, primarily driven by mobile technology. Kenya’s mobile money system, M-PESA, has been critical in Kenya’s Financial Inclusion Drive by providing a platform for even the marginalised households in Kenya to move money quickly and cheaply from one person to another.

Let’s consider Asabe Yusuf, a young widow with four children. Asabe owns and runs a small business of selling bananas and other seasonal fruits at Apo Junction in Nigeria’s capital, to keep a steady income stream — a typical female-owned micro business that does not hold much physical collateral. Like many women in Nigeria and other developing countries, Asabe does not have an official form of identification, the minimum requirement for opening accounts in formal financial institutions. Over the years, she has had to pass on several opportunities to get an account and access credit from the bank because she lacked the requisite requirements mandated by most financial institutions.

That was until we met her and told her about Kudeena – our financial inclusion and literacy vehicle targeted at low-income and forcibly displaced women in the North. Asabe not only opened a bank account but became our spokesperson at the junction where she trades and in her community. By saving consistently in her new bank account over a period of time, she is now able to buy larger amounts of produce thereby increasing her margins.

In addition, after successfully undergoing our financial literacy training, we were able to provide Halima with a loan via our microcredit scheme and this helped scale her business further.

Solving the access to finance – especially for women – requires community engagement and a nuanced understanding of the women these services are being developed for. Digital financial tools and services – and the associated learning to aid adoption – can help to drive adoption at scale.

Women entrepreneurs like Halima may lack the capacity to produce collateral or sufficient credit information to access loans from traditional financial institutions. Still, they continue to generate cash in their businesses. Therefore, they can benefit substantially from an increased availability of cash-flow-based loans without collateral or formal credit history.

Financial Technology (FinTech) players are pivotal in reshaping how the unserved and underserved at the bottom of the pyramid can access working capital and cash-flow finance. Digital technology takes advantage of existing cash transactions to provide innovative methods of credit scoring, risk assessment and disbursement. After all, cash is the only factor that can repay a loan; collateral is only the second way out if money cannot be generated.

A good example is India’s ‘Capital Float’, a digital financing platform that provides quick and easy working capital loans for small entrepreneurs to address immediate business requirements. The platform analyses borrower’s cash flow using data from e-commerce payment systems and mobile financial payment systems. The results from the analysis identify creditworthy borrowers. They then carry out an electronic know-your-customer (KYC) authentication, receive the loan offer, confirm acceptance, and sign the loan agreement, all on a mobile app.

Having acknowledged that no single type of loan can meet the needs of every kind of business, Capital Float launched the “business loan for women programme”, specially tailored to the needs of women-owned businesses in India. Under the initiative, women entrepreneurs can apply for collateral-free working capital without any processing fees. The Capital Float platform was launched in 2015 and has already reduced cash-flow challenges of more than 500,000 MSMEs with loan disbursements of $1.2 billion as working capital for these businesses.

The financial footprint made possible through digital payments allows for innovative methods of assessing the creditworthiness of women like Asabe. They could run service-oriented businesses that have the possibility of maintaining very high margins but lack enough hard assets to offer as collateral.

Cash flow loans are an excellent example of the targeted delivery and development of financial products and services that specifically meet the needs of marginalised women. As innovation marches toward risk-sensitive and highly regulated industries such as financial services, there must be a balance from the public sector between allowing creative solutions to emerge while simultaneously ensuring consumers and local economies are protected from risk.

The government can help by ensuring that legal and regulatory frameworks are ‘digital-ready’ to support FinTech innovation; reducing administrative obstacles and regulatory complexity, especially around multiple taxations; endorsing the adoption of efficient digitisation solutions, and introducing regulatory sandboxes that allow fintech to test solutions/products in a controlled environment.

We all benefit

Investing in women entrepreneurs is a trillion-dollar opportunity. A recent analysis by Boston Consulting Group (BCG) suggests that global GDP could rise from approximately 3 percent to 6 percent, boosting the global economy from $2.5 trillion to $5 trillion.

Investing in women goes beyond social responsibility: there is a business case for financial institutions; it improves the lives of women; and the domino effect of equality will be felt in their countries and beyond, influencing everything from its politics to its economic growth and development.

So, it is no exaggeration to say that women’s entrepreneurship has the power to change the world—and the benefits go far beyond boosting global GDP. Closing the gender gap in financial inclusion and fuelling the growth of women-owned enterprises will spur innovation, unleash new ideas, services, and products into our markets. And ultimately, those forces may redefine the future.

We cannot overcome poverty until men and women have equal rights and opportunities. Failure to address this gap means any policy initiatives that boost the supply of financial services in Nigeria are more likely to benefit Nigerian men and undermine the CBN’s ability to hit its 95 percent target. Put simply, Financial Inclusion policies are less effective, or may not succeed at all, if the different impact on women and men is not taken into account.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp