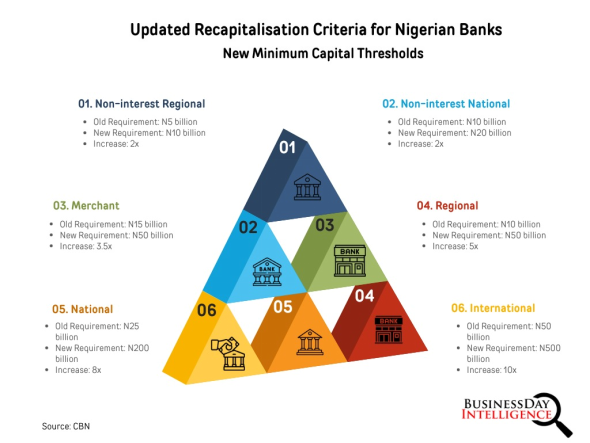

Nigeria’s banking system is getting a major overhaul! This is after the sector underwent its last major recapitalisation exercise two decades ago. In March 2024, the Central Bank of Nigeria (CBN) issued a directive, through the circular numbered FPR/DIR/PUB/CIR/002/009 titled “Review of Minimum Capital Requirements of Commercial, Merchant, and Non-Interest Banks in Nigeria,” to increase the minimum capital requirements for all Nigerian banks by April 2026. This move, aimed at strengthening the financial system and supporting the country’s economic growth ambitions, has banks scrambling to meet the new requirements within the two-year window. It comes amid the government’s goal of achieving a $1 trillion GDP by 2030 and a desire for a more robust financial system.

The ripple effect of the recapitalisation directive is reverberating throughout the banking sector, setting the stage for a profound transformation in the financial landscape. This move is already reshaping banking innovation and strategies, triggering a wave of restructuring as banks strive to meet the updated criteria through various regulatory channels. However, while exploring these options, banks may encounter potential innovation challenges that must be addressed to ensure compliance with the rules.

The CBN’s goals for a recharged banking system

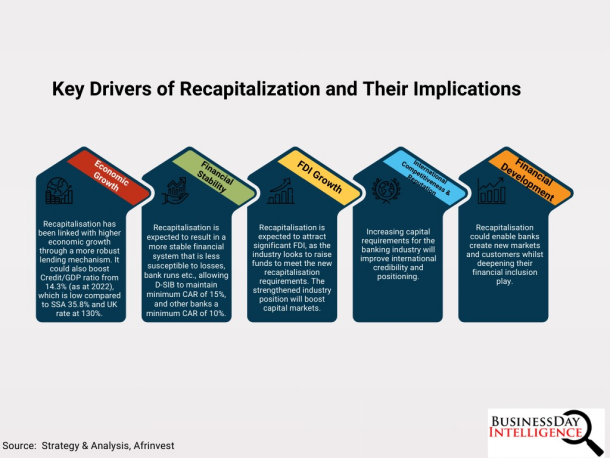

The New Recapitalisation Directive is a significant reform for the Nigerian banking sector. By strengthening individual banks and the overall financial system, it aims to create a more resilient and growth-oriented financial landscape for Nigeria. More specifically, the CBN’s goal of turbo-charging the Nigerian banking architecture can be summed up as follows:

Stability first! Banks with more capital are less likely to fall apart during financial crises, promoting overall economic stability.

Confidence is king! Stronger banks inspire more trust from depositors, businesses, and investors, creating a healthier financial environment.

Let’s get lending! With a more robust capital base, banks can lend more, fueling economic growth by providing credit to businesses and individuals.

The drivers and implications of recapitalisation are generally premised on fostering economic growth, improved financial stability, and enhanced international competitiveness and reputation.

“However, while exploring these options, banks may encounter potential innovation challenges that must be addressed to ensure compliance with the rules.”

Recapitalisation hurdles

The tightrope walks of time: 24 months might seem like a reasonable timeframe, but raising billions of Naira is no easy feat. Smaller banks, with less access to capital markets, may find themselves struggling to meet the deadline. This could lead to a scramble for funds, potentially driving up the cost of capital.

Merger mania or consolidation calamity? The pressure to meet the capital requirements could trigger a wave of mergers and acquisitions (M&A) in the banking sector. While consolidation can create stronger, more stable institutions, it can also lead to job losses, branch closures, and disruptions for customers. The key will be ensuring these M&A activities are strategic and value-driven, not simply a desperate attempt to meet the deadline.

Read also: Nigeria’s foreign investments rising on proposed bank recapitalisation -Cardoso

A domino effect on customers? Banks facing financial strain might resort to passing on the burden to their customers. This could manifest in several ways:

Fee Frenzy: Increased account maintenance fees, higher transaction charges, or even new fees for previously free services could become a reality.

Loan tightening: Banks might become more selective in who they lend to, potentially making it harder for businesses and individuals to access credit, especially for smaller loans.

Interest rate rollercoaster: Banks might adjust interest rates on deposits and loans to improve their profitability. While this can impact both savers and borrowers, it’s crucial to ensure any changes are done transparently and responsibly.

Regulatory Compliance Challenges

One of the flashpoints of the recent directive since Q1 2024 is the compelling of financial institutions to reassess their capital adequacy and compliance strategies. However, while the policy aims at bolstering the stability and resilience of the sector, from raising additional capital and bearing increased compliance costs to enhancing governance and risk management practices, the banks are expected to navigate a complex regulatory landscape and stakeholders’ expectations.

Some of the myriads of regulatory compliance hurdles that banks must navigate to meet the requirement effectively include:

Enhanced Capital Requirement and Financial Strain: One of the primary challenges posed by the CBN’s recent recapitalisation drive is the need for the financial institution to raise substantial additional capital. Recent estimates suggest that all the 34 DFIs in Nigeria are required to raise an additional N4 trillion in capital. The new requirement places financial strain on institutions, particularly smaller banks and those grappling with profitability issues, as was the case of Heritage Bank. We posit that raising capital in a volatile economic environment like Nigeria, where investors’ confidence is low, business confidence is dampened, and the economic prospect is slighted, raising additional capital is likely to exacerbate the difficulty, potentially leading to a consolidation wave as weaker banks merge with stronger ones to meet the capital thresholds.

Operational Adjustments and Compliance Costs.

Another dynamic in the wake of the directive is the significant operational adjustments within banks. Compliance with the enhanced capital requirement involves rigorous financial reporting, stress testing, and risk management protocols. This operational compliance comes with increased compliance costs, including the need for advanced technology systems, specialised personnel, and extensive training programmes. We envisage that smaller banks in particular are likely to struggle to bear this additional cost, leading to a competitive disadvantage.

Technological integration and cybersecurity: The push for compliance underscores the need for technological integration and cybersecurity development. Nigerian banks must invest in cutting-edge technology to streamline compliance processes, enhance data accuracy, and protect against cyber threats. The integration of technology with regulatory compliance efforts is critical, but it also introduces complexities related to data management, system interoperability, and cyber resilience.

Banking innovations: A strategic approach

In response to CBN directives, financial institutions must explore innovative strategies to meet the heightened capital requirements. Clearly, to facilitate the actualisation, CBN outlines three (3) broad response pathways to the recapitalisation drive with multiple options to consider: raise funds; restructure; and/or exit or divest. This is expected to boost banks’ capacity to navigate the prevailing and possible future economic headwinds, enhance resilience, boost liquidity, enhance solvency, and continue to support Nigeria’s economic growth.

Read also: Race to 2026 bank recapitalisation: Meet the CFOs of top merchant and non-interest banks in Nigeria

Some of the innovations include:

-Digital banking expansion: Digital banking represents a significant innovation that banks can leverage to meet additional capital requirements. By expanding digital services, banks can reduce operational costs, increase customer reach, and boost revenue streams. Digital platforms enable banks to offer a range of services such as online banking, mobile banking, and digital wallets, which attract tech-savvy customers and promote financial inclusion. The reduced need for physical branches lowers overhead costs, freeing up capital for other strategic investments.

Fintech Collaborations: Collaborating with fintech companies allows banks to tap into advanced technological solutions and innovative financial products. Fintech partnerships can facilitate the development of new services, such as peer-to-peer lending, robo-advisory, and blockchain-based transactions, enhancing the banks’ service offerings and revenue potential. Additionally, fintech collaborations can improve operational efficiencies and customer experiences, driving profitability and enabling banks to build up their capital reserves.

Capital Market Access: Banks can explore accessing capital markets to raise the required capital. Issuing equity or debt securities, such as bonds or preference shares, provides a viable avenue for banks to garner substantial funds. By diversifying their funding sources, banks can mitigate risks associated with traditional funding methods and enhance their capital base. Successful capital market transactions require strong investor relations and transparent financial reporting to attract potential investors.

Securitisation and Asset Management: Banks can employ securitisation techniques to convert illiquid assets into tradable securities, thereby freeing up capital. By packaging loans or other receivables into asset-backed securities, banks can sell these instruments to investors, generating immediate liquidity. Additionally, banks can enhance their asset management capabilities by offering wealth management and investment advisory services. These services attract high-net-worth individuals and institutional investors, bolstering the banks’ capital through fee-based income and managed assets.

Enhancing Operational Efficiency: Improving operational efficiency through process automation and cost optimisation can help banks conserve capital. Implementing advanced analytics, artificial intelligence (AI), and machine learning can streamline back-office operations, reduce errors, and enhance decision-making processes. By cutting down on operational expenses, banks can allocate more resources towards meeting capital requirements and strategic growth initiatives.

Sustainable Finance and Green Bonds: Banks can explore sustainable finance options, such as issuing green bonds to raise capital for environmentally friendly projects. Green bonds attract a growing segment of socially responsible investors seeking to support sustainability initiatives. By aligning with global sustainability goals, banks not only meet capital requirements but also enhance their reputation and contribute to positive environmental impacts.

For banks to successfully navigate this recapitalization process, some key considerations include:

Strategic capital raising: banks can explore various options like issuing new shares, mergers and acquisitions, or attracting private equity investments.

Risk management: Maintaining strong risk management practices is crucial to ensuring the effective utilisation of the increased capital.

Governance and transparency: Upholding good corporate governance and transparency will be essential to attract investors and maintain public trust.

Balancing Act: Compliance and Innovation

It is a unanimity that the recent CBN’s directive to banks introduced a new set of challenges and opportunities. As the banks gear up to comply with the new heightened capital demand, they must also innovate and develop new products and services to remain competitive, sound, and profitable. Striking this balancing act will be crucial for sustainable growth and stability of the financial industry.

Banks will need to find creative solutions, such as raising capital, restructuring their operations, or even exiting certain markets, all while staying within the regulatory boundaries. The key question remains: How can banks become financially stronger while continuing to innovate for the future? To navigate the labyrinth, BDI’s in-depth observation of the financial ecosystem motivates us to make the following suggestions:

Agility and Adaptability: All banks across different licensing categories must be able to adapt quickly attuned to the regulatory demands and market dynamics. By regularly reviewing and updating the risk management framework, compliance policies, and innovation strategies, they will be able to foster a culture of agility and continuous improvement.

Continuous stakeholder engagement: A core strategy that all the banks must build is to cultivate the ethos of continuous engagement with regulators, customers, and other stakeholders to balance their quest for meeting the demand and the regulatory expectations. Transparent communication and collaboration can help build trust and support the bank’s initiatives.

Strategic planning: They must develop a comprehensive strategic plan that takes cognizance of these two pillars. They can do this by setting clear objectives, prioritising projects, and allocating resources effectively.

In sum, the new CBN recapitalisation directive presents both challenges and opportunities for Nigerian banks, which, by balancing regulatory compliance with innovation—through digital transformation, fintech collaboration, capital market access, and sustainable finance—can enhance resilience, competitiveness, and support for economic growth.

For Enquiries: Nike Alao-Chief Research Officer: +2348034856676

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp