The conduct of monetary policy has largely been to maintain internal and external balance of payments. However, the techniques, or perhaps strategies, to achieve this objective have evolved over the years.

The first technique employed was circa mid 1980s with emphasis placed on direct monetary controls while the second largely relies on market conditions. Notwithstanding the two periods, the Nigerian economy has perhaps witnessed a dramatic shift in the apex bank’s mandate on price stability to an active market operator through its numerous intervention funding schemes. Section 31 of the Central Bank act gives the apex bank its powers to use its developmental function to stimulate sectors within the economy.

Global events such as the economic crises of 2009 and more recently in 2020, the Covid-19 hysteria which culminated in demand and supply shock cum health crisis has given the apex bank greater impetus to churn out more intervention schemes to aid economic growth.

Read Also: Surging inflation driving 7 million Nigerians into poverty

A cursory look around the globe shows that central banks often steer clear of direct intervention for fear of crowding out, mis-signalling the markets and over-heating the economy.

There is an existing partnership between the Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank, the Sveriges Riksbank and the Swiss National Bank, and the Bank for International Settlements (BIS), to explore the future of central bank digital currency (CBDC) in their various jurisdictions.

Specifically, the banks are to focus on the economic, functional, and technical design choices, including cross-border interoperability, and the dissemination of knowledge on emerging technologies. The Bank of Canada is expected to work with the relevant institutions and forums – in particular, the Financial Stability Board and the Committee on Payments and Market Infrastructures (CPMI).

Some other projects which are considered out of the mandate of central banks can be witnessed in the European Union with the ECB’s announcement in a circular dated 27th November 2020 that guides banks on ways to prudently manage and transparently disclose climate-related and environmental risks. As such, banks are expected to conduct a self-assessment this year and undergo a full supervisory review of their practices by next year.

Other central banks such as Bank of Canada and Monetary Authority of Singapore have all focused on Distributed Ledger Technologies for clearing and settlement. In short, central banks globally have not spent a lot of their focus on direct sectoral intervention programs.

Problems with Inflation

Economists usually oppose high inflation, but they oppose it in a milder way than many non-economists. Nobel prize winner in economics Robert Shilller carried out several surveys during the 1990s about attitudes toward inflation. One of the questions he asked respondents was, “Do you agree that preventing high inflation is an important national priority, as important as preventing drug abuse or preventing deterioration in the quality of our schools?” Answers were on a scale of 1–5, where 1 meant “Fully agree” and 5 meant “Completely disagree.”

For the U.S. population, 52% answered “Fully agree” that preventing high inflation was a highly important national priority and just 4% said “Completely disagree.” However, among professional economists, only 18% answered “Fully agree,” while the same percentage of 18% answered “Completely disagree.”

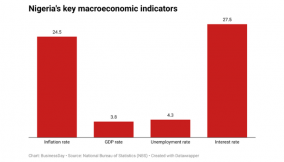

Coincidentally, Nigerian inflation is around 18% and if you are to ask the regular man or woman on the streets of Lagos, Abuja, or perhaps any city in the country you will probably find that they too agree that inflation is top of mind since wages do not rise as fast as inflation. Consider a mother who used to buy four fish in the market for N10,000 can now only buy two. Not only has purchasing power decreased, but it also means that household budgets now need to be revisited. Since the current realities have shown that economic variables do not move exactly in sync with inflation, or perhaps they adjust after a time lag, then inflation can cause three types of problem:

1. Blurred price signals

2. Unintended redistribution of purchasing power

3. Difficulties in long-term planning

Despite this observed phenomenon, the number of funds channelled into the economy through intervention funds and Federal Account Allocation Committee (FAAC) disbursements are equally on the rise. There are numerous intervention schemes proposed and implemented by the Central Bank some of which include:

1. Agri-Business/Small and Medium Enterprise Investment Scheme (AGSMEIS): Targeted towards agricultural businesses and small/medium enterprises (SMEs) in the country, the AGSMEIS Loan, as an initiative to support the Federal Government’s efforts in the development of the agricultural sector. The loan is disbursed through NIRSAL and other Banks and can be accessed at 5%. A total of N111.7 billion has been disbursed to 29,026 beneficiaries under this scheme.

2. The Anchor Borrowers Programme (ABP) caters to smallholder farmers engaged in the production of identified commodities across the country. The Farmers are encouraged to apply in groups/cooperative(s) of between 5 and 20 for ease of administration. Businesses can also apply to become Anchors or Inputs, Suppliers. The loan can be accessed at a maximum interest rate of 9%. 3,107,949 smallholder farmers cultivating 3.8 million land hectares have benefited from was N 631.4 billion.

3. The Accelerated Agricultural Development Scheme (AADS) according to CBN, is to engage a minimum of 370,000 youths in agricultural production across the country over the next three years to reduce unemployment among the youths in the country and increase agricultural production towards food security, job creation, and economic diversification. The beneficiary must be a Nigerian youth with the ages of 18 to 35 years and must sign an undertaking to abide by the terms of agreement of the Scheme.

Others include Micro, Small and Medium Enterprises Development Fund (MSMEDF). Creative Industry Financing Initiative (CIFI), and Healthcare Sector Research and Development Intervention Scheme (HSRDIS) grant.

Following the last Monetary Policy Committee meeting held on the 24th and 25th of May, the committee observed that there had been marginal growth in the manufacturing purchasing managers index (PMI) to 49.0 index points in April which to be clear, remains below the 50-index points expansion level. Furthermore, the committee noted that nearly a trillion naira had been disbursed under the CBN’s interventions scheme and resolved that the CBN should continue to aggressively increase its intervention funding to selected subsectors, including agricultural processing and manufacturing. In addition to the CBN intervention funds, N1.3 trillion has been disbursed on several federal government funds namely the National Youth Investment Fund, Real Sector Intervention, Healthcare Support Intervention fund, CBN Health Care Grant for Research on Covid-19 and Lassa Fever, the National Mass Metering program, and the Nigerian Electricity Stabilization Facility.

Although all the schemes have recorded successes, what about the costs to the economy as a whole?

Intervention Funds Total (Billions of Naira )

Anchor Borrowers Programme 631.40

AGSMEIS 111.70

Targeted Credit Facility 253.40

National Youth Investment Fund 2.04

Creative Industry Financing Initiative 3.19

Real Sector Intervention 856.30

Healthcare Support Intervention Fund 97.40

Health Care Grant for Research 232.50

National Mass Metering Program 35.90

Nigerian Electricity Stabilization Facility 93.80

Total 2,317.63

There is also the issue of Federal disbursements. Every month, the Federal Account Allocation Committee (FAAC) meet and disburse huge sums of monies to the three tiers of government. The sum of N 2.93trn was disbursed to the Federal Government in 2019. The highest Net Allocations were N 275.03bn and N 266.49bn, disbursed in the months of July and September, respectively while the least amounts disbursed were N219.51bn in May and N 223.28bn in March. Fast forward to 2021, there has been a consistent disbursement of around N 619 – N 681bn which, in my view, only aids in overheating the economy.

The road less travelled

The economy can be simply characterized as being in a state of stagflation. In other words, slow economic growth, relatively high unemployment accompanied by rising prices. And in a world where everyone agrees that inflation is a national issue and must be tamed, what types of policies do monetary and fiscal authorities employ to achieve this objective? I would like to propose a few options for consideration.

First, we must acknowledge that a more coordinated monetary and fiscal policy must be imbibed. To achieve this, one must revisit the level of money supply in the formal and in the less talked about shadow economy. Money supply will need to be reduced by both fiscal and monetary authorities. Achieving this will take discipline and courage. For starters, the fiscal authorities will need to reduce FAAC allocation and consider a matching system pegged to individual states internally generated revenue (IGR) that way FAAC now becomes performance-based, while the monetary authority will have to simultaneously wind down its intervention schemes. Furthermore, setting interest rates below market-determined rates may in the near term appear helpful to the respective companies and sectors being targeted; however, in the long run, there is a crowding out effect that occurs which does not help the intended parties the policy sought to aid.

We must collectively be able to tell ourselves the truth. The economy is ailing, and it has been this way for quite some time, and we have not turned the corner to recovery. To be clear, I do not believe it makes good economic sense to continue this path because in the end, we continue to borrow from the future to pay for the present and there is not enough output growth in any sector of the economy to remain sustainable. While we have recorded growth in the agriculture sector, where there are floods coupled with insecurity, the translation is lower yields and higher prices to the consumers. Perhaps more focus should be around the infrastructure to mitigate against the flooding, irrigation to ensure year-round farming and lastly, local responses and techniques to the insecurity bedevilling the sector and country at large.

Prof. Joseph Nnanna, is Chief Economist at Development Bank of Nigeria

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp