Nigerian insurance underwriters are major to be blamed for the low and unsustainable risk premium rates, which is also stifling the much-anticipated growth of the industry, Ganiyu Musa, Group Managing Director, Cornerstone Insurance Plc has said.

Speaking at the Cornerstone Insurance Plc 2023 Brokers engagement meeting held in Abuja, Group Managing Director of Cornerstone Insurance Plc, Ganiyu Musa raised concerns that insurance premiums in Nigeria are largely underpriced, as underwriters deviate from the basics of the profession and have collectively driven rates to an unsustainable level.

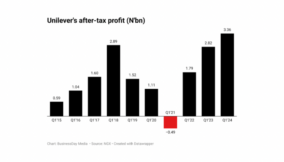

Cornerstone, which is a Tier 1 Insurance Company in Nigeria reported some N4 billion Gross Premium growth in 2022 to N24.6 billion as against N22.3 billion that it posted in the 2021 financial year.

Musa, said premium underpricing, has cut down profitability across the insurance industry to a level far below other sectors of the financial services sector.

He reiterated that insurance being a specialized subject area is guided by a number of technical and professional considerations, as pricing is done on certain underwriting principles, technical rating, on risk management amongst others.

“However, as an industry, we have deviated from the basics of our profession, in the sense that we have all collectively driven insurance rates to levels that are not sustainable. And that is why we are suffering. Our profitability across the industry is below par. It is not comparable to what you have in the other arms of the financial services industry,” Musa lamented.

Drawing an analogy, he explained that the banking industry which is faced with similar regulatory constraints does better with pricing and in a unified manner than what obtains in insurance.

He notes for instance that “If the CBN says you cannot lend for more than 21 per cent, or that you cannot pay less than two per cent interest on the current account, for the banks, that maximum lending rate is what applies to the majority of their customers. If anything, in addition to the specified lending rate they also charge documentation fees, legal fees, such that at the end the customer is borrowing above the specified rate.”

“ But for us as insurers, faced with a similar regulation that says, for instance, the motor premium should not be more than 10 per cent, while the banks will take that rate as the minimum that they charge, insurers take that as the maximum and then drives it down.”

He said until December when NAICOM came to their rescue with a new guide on rating, motor premiums had gone down to as low as one per cent in certain cases.

“That is why contrary to the position of the industry two, three decades ago when insurance companies actually owned banks, we have now turned full circle to a situation where the banks just pick up insurance companies with peanuts. That is why we are suffering.”

Musa insisted it is the collective responsibility of all underwriters to develop the discipline needed to change the trend.

“We cannot blame the brokers even though we believe that they could play a greater role in collaboration. Their obligation is to the insured. And their mandate is to get the best terms for the insured.

“It is the underwriters that are squarely to blame because we are not forced to accept those rates, we determine the pricing, and we put our balance sheet at risk. If all the underwriters come together and agree on the rate of premium to accept and the brokers go from underwriter A to Z and get a similar response, they will pay a price that is fair or carry their risk,” he said.

“So it is squarely on our own shoulders as underwriters, we cannot blame anybody else, we cannot blame the regulator. If anything, the regulator has been trying to fight our battle, we should do what is right rather than tread away our rights, our profitability and our balance sheet.”

He, however, acknowledged that more than ever, there is now a lot more understanding, awareness and collaboration amongst the stakeholders.

Read also: Buhari’s metering rollout yet to make ‘crazy bill’ history

Musa who sits on the Governing Council of the Nigerian Insurers Association (NIA) said a number of initiatives are being put in place to try to address these issues, beginning with motor insurance where technology is now deployed. This is in addition to collaborations with aggregators, and state governments to regulate and check all those unethical practices of people hawking third-party insurance at ridiculous prices.

He said there is also the NIA marine portal, which has been integrated with the CBN trade portals, and customs, in a bid to checkmate the unethical practices in the area of marine insurance.

He observed that there is now a much better rating for fire insurance which has been one of the biggest challenges for the industry in terms of profitability.

He assured that the industry is taking its deeply rooted challenges head on and will therefore take time to cascade into quite visible results.

He also assured that payment of claims which has been a thorny issue is now being taken seriously considering that it is a key element of trust.

Cornerstone Insurance which prides itself on having a very liquid and strong balance sheet sees claims as a top priority, and has never defaulted in any of its obligations, except where the insured has breached the terms, the GMD noted.

On the low insurance penetration, he noted a number of steps being taken to address it, including awareness which was lacking.

“If you do not sort out the issue of trust, it is very difficult for you to recover. And one of what is being done in this regard is to get the operators to imbibe discipline as a priority which entails members leaving up to their responsibility or facing suspension or even expulsion.

“I can assure you that now, it’s almost impossible for you to have a valid claim by a member of the NIA that is not paid. Where a claim is not paid by an NIA member, just be sure that there is possibly a critical part of the contract that the insured has not complied with.

“It’s to clean up our acts, improve discipline, improve collaboration, use technology,” he assured, stressing the need to correct legacy impression.

Earlier, while addressing the brokers, he assured them of the company’s commitment and collaboration, and that Cornerstone Insurance has a strong balance sheet which enables the company to deliver on promises.