A team of analysts at RMB Nigeria Stockbroking (RMBNS), a member of Rand Merchant Bank, have estimated that the earnings per share (EPS) of Dangote Cement Plc will decline by an average of 4 per cent over the estimated period of 2018 to 2020 citing weaker-than-expected third quarter (Q3) 2018 results and a revised outlook for Nigeria’s cement consumption. As elections draw closer, it is expected that construction projects might not get much attention from policy makers in the first quarter of 2019.

“We expect the impact of recent flooding to impact volumes in fourth quarter (Q4) 2018. We estimate Q4, 2018 volumes at 2.8 million tonnes (MT). Broadly, we now expect Nigeria’s 2018e and 2019e volumes at 13.6MT and 14.8MT (+9 per cent year-on-year) respectively. Our 2019e volumes are also c5 percent lower as we expect the electioneering process to cause a lull in construction across Nigeria through first half (H1)2019,” RMBNS said in a note to investors.

READ ALSO; Analysts maintain Buy Ratings on Dangote Cement

| Year | Current EPS | Previous EPS |

| 2015A | 10.86 | 10.86 |

| 2016A | 10.95 | 10.95 |

| 2017A | 11.99 | 11.99 |

| 2018e | 12.40 | 13.54 |

| 2019e | 15.81 | 15.99 |

| 2020e | 18.33 | 18.56 |

Source: RMBNS

A= actual; e = estimated

Dangote Cement’s third quarter result reveals that over 17 MT of cement were sold in Q3’18 representing 7.6 per cent growth when compared with 16.5 MT sold in the corresponding period of 2017.

The cement manufacturer’s revenue for the period surged by 13.5 per cent from N603.6 billion in third quarter (Q3) 2017 to N685.3 billion buoyed, as usual, by increased volumes in Nigeria and a price surge in its Pan-Africa operation.

The Nigeria operation’s contribution to the top line in Q3 2018, from 10.8MT of cement sold (9.6MT sold in Q3, 2017),was 68.8 per cent (N471.3 billion) even though revenue from the operational region rose by 13.3 per cent from N416.1 billion in Q3 2017.

Sales at the Pan Africa region of the business remained relatively flattish, rising marginally by a meagre 0.1 per cent to 7 million tonnes. Increased prices boosted revenue in the region by 11.7 per cent to N214 billion in Q3 2018 relative to N191.9 billion in the corresponding quarter of the preceding year as a result of foreign exchange gains when converting the sales from foreign currencies into naira.

“The average per-tonne price for Pan-African operations increased from N27,322 to N30,502 mainly as a result of changes in the exchange rate,” Dangote Cement Plc said in its nine months report released to the Nigerian Stock Exchange (NSE) recently.

But RMBNS believes the results were unimpressive relative to expectation. The not too impressive performance of the group was due to the Nigerian operation which delivered the weakest country earnings before interest, tax, depreciation and amortization (EBITDA) margin of 62.4 per cent post fourth quarter (Q4) 2016 and lowest volumes of 3 million tonnes post Q4, 2015.

“Relative to our estimates, 3Q18 (9M) was lower by 24% (-8%). Also, Nigeria’s 3Q18 realised cement price declined by 3 per cent quarter-on-quarter (q/q), to N43.2k/t (US$119/t) against our N44k/t, reflecting the increased need to offer rebates in a seasonally weak, rainy quarter,” RMBNS said in the note to investors.

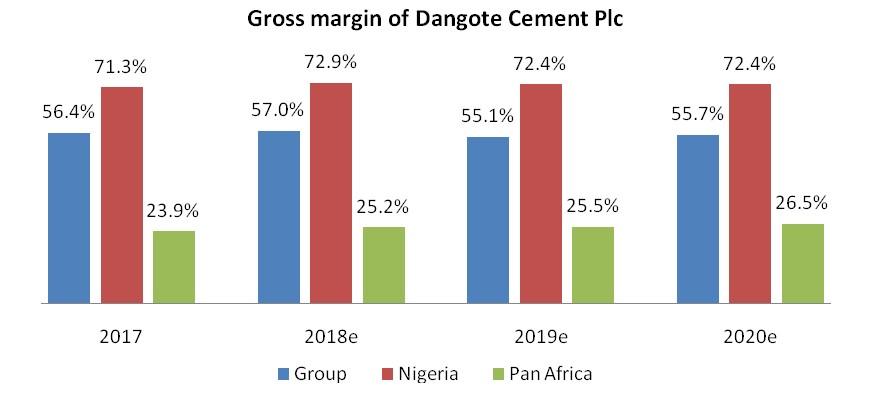

Meanwhile, RMBNS expressed satisfaction with the energy strategy of Dangote Cement especially the complete elimination of the use of LPFO and the use of locally-sourced coal in its plants at Obajana and Ibese in Kogi and Ogun states respectively which drove gross margin of its Nigeria operation to 73.2 per cent in Q3, 2018.

Source: RMBNS

The growth in Pan-Africa COGS/t of N22.4k/t wiped off Nigeria’s stellar COGS/t of N11.6k/t and drove the group production costs up by 3 per cent quarter on quarter to N16.7k/t sparking call for the energy gains by Nigeria to be replicated in the group’s Pan-Africa operations.

“While we like the energy gains from the Nigerian operation, we would like to see the Pan African operation deliver similar gains to support earnings. Reducing the Pan-Africa’s COGS/t by 14%, from current levels, could drive an EPS upgrade of 25 per cent on our estimates,” the report stated.

However, Gbenga Sholotan, equity analyst at RMBNS stated in the report that “a material deterioration in Nigeria’s energy efficiency is a risk to computed estimates even though Nigeria’s cost of goods sold (COGS) per tonnes (COGS/t) is 6 per cent higher than reported in Q3.”

Despite the slash in EPS, the stockbroker retained an overweight rating for Dangote Cement stock at a target price of N263 per share with an expected total return of 32 per cent, including a dividend yield of 4.2 per cent.

“Our target price (TP) is lower – N263 (from N268) – and we reiterate our overweight rating (OW) for the stock as we see potential expected total return (ETR) of 32 per cent, inclusive of a 4.2 per cent dividend yield, from current levels,” RMBNS said.

An overweight rating for a stock means that total return is expected to exceed the average total return of the analyst’s industry coverage universe, on a risk-adjusted basis, over the next 12 months.

Dangote Cement is the most capitalised stock on the Nigerian Stock Exchange (NSE). As the close of business on October 30, 2018, its share price closed at N216 per share which amounted to N3.68 trillion in market capitalisation, and thus accounted for 30 percent of the market capitalisation of stocks listed on the NSE. At the end of the 2017 financial year, the cement giant paid N10.5 dividend per share.

KELVIN UMWENI

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp