Africa’s private sector regained momentum last month as easing energy prices and improving business confidence lifted activity across more economies at the end of the first half of the year.

But that fragile recovery now faces a fresh threat after Iran announced on Sunday that it would close the Strait of Hormuz, raising the risk of another oil price shock that could reignite inflation, weaken consumer spending, and slow business activity across the continent.

The closure of the world’s most strategic oil shipping route comes a few days after Purchasing Managers’ Index (PMI) surveys showed business conditions improving across much of the continent, buoyed by lower fuel costs following the temporary easing of tensions in the Middle East.

A prolonged disruption to crude shipments could quickly reverse those gains, particularly in Africa’s net oil-importing economies, where higher energy costs feed directly into inflation and operating expenses.

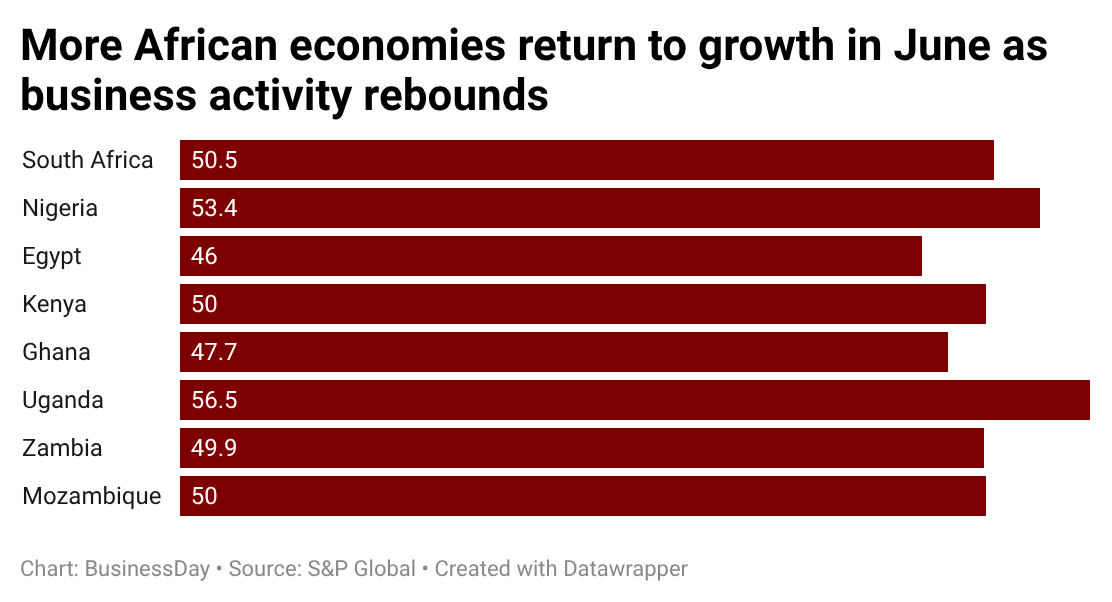

BusinessDay’s analysis of PMI data across eight African economies shows that five recorded an expansion in private-sector activity in June, while three remained in contraction. The improvement marked a rebound from May, when five economies contracted, although it remained below March’s performance, when only two economies reported weaker business conditions. Three economies contracted in April.

A PMI reading above 50 indicates an expansion in business activity from the previous month, while a reading below 50 signals contraction. As one of the earliest indicators of economic performance, the survey provides a timely gauge of changes in output, demand and broader economic growth.

Further analysis also shows that, on average, five of the eight economies surveyed expanded during the second quarter (April-June), while three contracted. In Q1, only two contracted while the rest expanded. Across the first six months, the regional PMI averaged 50.5, slightly below the 50.9 recorded a year earlier, indicating that business activity remained in expansionary territory despite geopolitical tensions and persistent global economic uncertainty.

Last month’s improvement coincided with a modest rebound in global business activity as lower oil prices and easing geopolitical tensions supported confidence after almost four months of disruption linked to the conflict involving the United States, Israel and Iran.

According to S&P Global, worldwide business activity expanded at its fastest pace since the outbreak of the Middle East conflict, although growth remained below levels seen earlier in the year.

“However, the structure of growth showed signs of changing amid the improved newsflow out of the Middle East: the recent strong manufacturing expansion slowed amid reduced precautionary stock building, while services growth revived – notably for consumer-facing industries – amid the recent drop in energy prices,” said Chris Williamson, business economist and executive director at S&P Global Market Intelligence.

Williamson noted that businesses benefited from lower oil prices following the ceasefire and the memorandum of understanding signed between the US and Iran, which temporarily eased concerns over disruptions to global shipping through the Strait of Hormuz.

The improvement, however, proved short-lived.

Renewed hostilities between the United States and Iran over the weekend, including fresh attacks around the Strait of Hormuz, have once again injected uncertainty into global markets. Although Brent crude has retreated to below $80 a barrel from wartime highs above $120, investors remain cautious as the risk of further disruptions to one of the world’s busiest oil shipping routes persists.

Last week, the International Monetary Fund (IMF) projected that sub-Saharan Africa’s economy is expected to grow by 4.3 per cent this year, but warned that the headline figure masks widening differences across countries.

“While growth in SSA is expected to remain broadly stable, this masks substantial divergence across countries,” the IMF said, pointing to differences in policy reforms, fiscal space and exposure to external shocks.

The Fund noted that oil-importing economies remain particularly vulnerable to higher energy and food prices, while countries that implemented earlier macroeconomic reforms are proving more resilient despite weaker global demand and declining development assistance.

South Africa, Kenya and Mozambique return to growth

South Africa, Kenya and Mozambique all returned to expansion in June, helping lift Africa’s private-sector recovery after a difficult May.

Uganda remained Africa’s standout performer, posting the continent’s highest PMI reading of 56.5, up from 54.1 in May, overtaking Nigeria, which had led the rankings the previous month.

The Stanbic Bank Uganda PMI signalled its seventeenth consecutive month of expansion, underpinned by strong customer demand, rising new orders and sustained hiring.

“Uganda’s June Stanbic PMI data confirm that private sector conditions remain robust. Firms reported broad-based new order and output growth due to increased sales and sustained customer demand,” said Christopher Legilisho, economist at Stanbic Bank.

“Positively, firms had to increase headcounts to support higher capacity requirements. To this end, firms increased the quantities purchased, and inventories too were expanded due to resilient client demand.”

South Africa’s private sector also returned to growth after the PMI rose to 50.5 from 49.6 in May, supported by easing inflationary pressures and resilient hiring.

“The PMI’s recovery in June was mainly helped by resilient hiring at South African companies, although output and order books fell at slower rates than in May,” said David Owen, principal economist at S&P Global Market Intelligence. “The outlook among private sector businesses suggests that economic challenges are expected to stay, with optimism hitting its weakest level for nearly five years.”

Kenya and Mozambique also moved back into expansion territory, reflecting improving business activity as cost pressures eased following the decline in global oil prices.

The recovery, however, remained uneven. Egypt, Zambia, and Ghana stayed in contraction, with Egypt recording the weakest performance among the major economies tracked. The PMI fell to 46.0 in June from 47.1 in May, the lowest reading since January 2023.

“The Middle East conflict has exacted a toll on the domestic non-oil sector, with the latest data signalling the steepest decline in new work in over three-and-a-half years,” Owen said.

The PMI surveys now offer a snapshot of Africa’s economy before the latest escalation in the Middle East. If the closure of the Strait of Hormuz persists and oil prices climb sharply again, the improvements recorded in South Africa, Kenya and Mozambique could prove short-lived, while inflationary pressures would intensify across many of Africa’s fuel-importing economies.

The second half of the year may therefore begin with businesses confronting another external shock just as the continent’s recovery was starting to broaden.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp