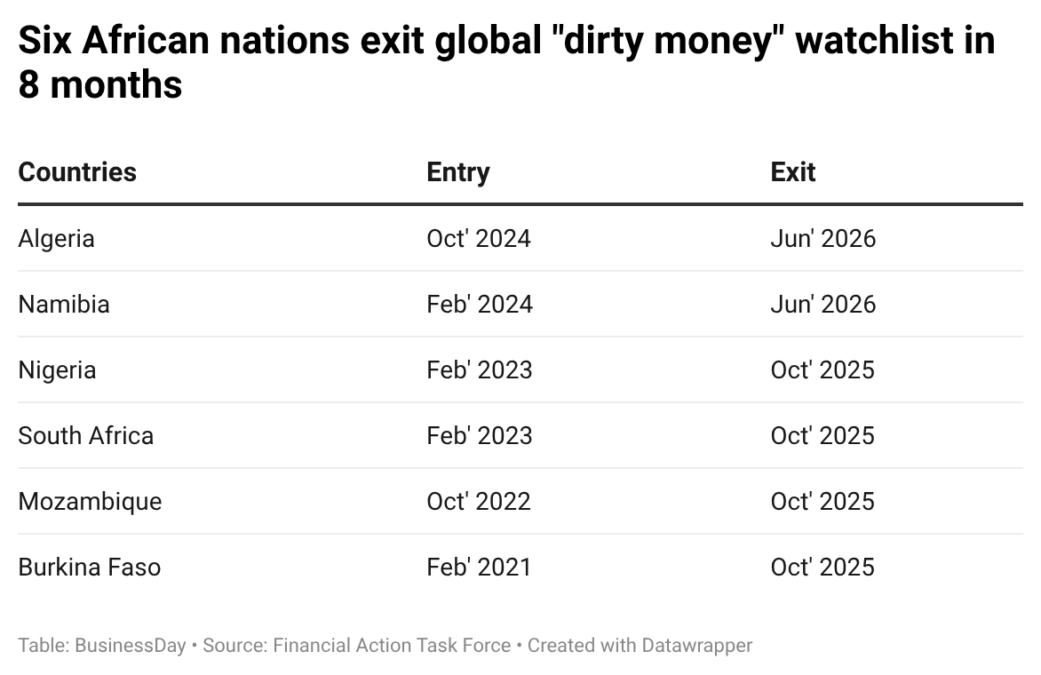

Africa’s efforts to strengthen anti-money laundering controls gained fresh momentum after Algeria and Namibia were removed from the Financial Action Task Force’s (FATF) grey list, bringing to six the number of African countries to exit the global watchlist in the past eight months.

The latest removals extend a wave of progress that has seen Nigeria, South Africa, Mozambique and Burkina Faso strengthen safeguards against money laundering and terrorist financing, improving their standing with international investors, lenders and correspondent banks.

The FATF, the world’s leading watchdog on money laundering and terrorist financing, announced on Friday that Algeria and Namibia had been removed from its list of “Jurisdictions under Increased Monitoring” after completing action plans designed to address strategic deficiencies in their financial crime frameworks.

“Algeria and Namibia were removed after successful on-site visits confirmed they had completed their action plans,” the Paris-based watchdog said in a report. “Algeria will continue working with MENAFATF and Namibia with ESAAMLG to sustain the improvements.”

The development marks another milestone in the continent’s push to improve financial transparency and restore investor confidence after years of heightened scrutiny from international regulators.

Countries on the FATF grey list are subject to increased monitoring because of weaknesses in their anti-money laundering and counter-terrorism financing systems. While grey-listing does not automatically trigger sanctions, it can increase compliance costs, complicate correspondent banking relationships and make it harder to attract foreign capital.

The FATF also added Iraq and Bosnia and Herzegovina to the grey list during its latest plenary meeting. The list now contains 22 jurisdictions under increased monitoring, including six African countries: Angola, Cameroon, Côte d’Ivoire, the Democratic Republic of Congo, Kenya and South Sudan.

Why the removals matter

The latest exits send a positive signal to international investors, financial institutions and credit rating agencies, demonstrating progress in aligning African financial systems with global standards.

Beyond reputational benefits, removal from the grey list can reduce compliance burdens for financial institutions, improve access to international banking networks and support foreign investment inflows.

The progress comes as African countries compete for global capital amid rising geopolitical uncertainty and tighter international scrutiny of illicit financial flows.

Algeria’s return to compliance

Algeria’s removal represents a turnaround after the North African nation was re-added to the FATF grey list in October 2024, having previously exited the list in 2016.

To secure its latest removal, the country implemented a series of reforms aimed at strengthening beneficial ownership transparency, improving oversight of financial and non-financial sectors, increasing transparency in cross-border financial flows and enhancing the detection of suspicious transactions.

According to Abderrahmane Mebtoul, former Director-General of Economic Studies, the reforms were underpinned by legal and institutional changes introduced since 2023, including amendments to the country’s anti-money laundering framework and stronger compliance requirements for banks and financial institutions.

The authorities also accelerated the implementation of a National Register of Beneficial Owners and introduced stricter customer due diligence and transaction monitoring requirements.

The reforms are expected to strengthen Algeria’s financial credibility, improve relationships with international banking partners and enhance the country’s attractiveness to foreign investors.

Namibia exits after addressing 13 deficiencies

Namibia was placed on the FATF grey list in February 2024 after the watchdog identified 13 strategic deficiencies in its anti-money laundering and counter-terrorism financing framework.

The Southern African nation successfully addressed all 13 deficiencies, leading to its removal following a positive on-site assessment by FATF. According to the country’s finance ministry, the reforms strengthened Namibia’s ability to detect, investigate and prevent financial crimes while improving regulatory oversight.

The removal is expected to lower compliance costs, improve access to international finance and strengthen investor confidence in the country, which is Africa’s largest producer of uranium.

Nigeria, South Africa lead Africa’s FATF turnaround

The latest removals also follows the exits of Nigeria and South Africa from the FATF grey list in October 2025.

Africa’s two largest economies implemented sweeping reforms to strengthen anti-money laundering controls, improve financial intelligence sharing, increase beneficial ownership transparency and tighten regulatory oversight.

South Africa addressed 22 action items agreed with FATF through legislative reforms, stronger law enforcement coordination, enhanced tax and border controls and tougher supervisory penalties for non-compliant institutions.

Nigeria, which was added to the grey list in February 2023, strengthened its anti-money laundering framework through new legislation, enhanced supervision of high-risk sectors, improved financial intelligence capabilities and increased enforcement against financial crimes.

Mozambique and Burkina Faso also exited the list in 2025 after implementing extensive reforms to strengthen anti-money laundering controls, improve beneficial ownership transparency, enhance financial sector supervision and boost financial crime investigations. Mozambique had been under increased monitoring since October 2022, while Burkina Faso entered the list in February 2021.

Their exits highlight a broader trend of African countries strengthening financial governance frameworks to meet international standards and improve access to global capital. While six African countries remain on the FATF grey list, the recent wave of removals shows growing momentum in the continent’s efforts to combat illicit financial flows and strengthen financial sector credibility.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp