On June 23, 2015, the Central Bank of Nigeria issued Circular TED/FEM/FPC/GN/01/010, declaring 41 imported product categories ineligible for foreign exchange in the official market. Subsequent addenda raised the count to 43, including milk and dairy products in 2019, imports the CBN said were consuming between $1.2 billion and $1.5 billion in foreign exchange every year. The list ran from rice, cement, tomato paste, textiles and steel products to toothpicks. Importers were never banned from bringing those goods into Nigeria. They were only barred from buying official dollars to pay for them.

The policy was born of genuine distress. Brent crude, which averaged about $100 a barrel in June 2014, had fallen to roughly $59 by June 2015, and Nigeria still depended on crude receipts for the bulk of its dollar inflows. Godwin Emefiele, the CBN governor who authored the restriction, would later disclose that monthly oil receipts into the external reserves fell from above $3 billion in 2014 to zero by late 2022, a measure of how completely the country’s dollar engine stalled.

Eight years after the Central Bank barred dozens of imports from accessing official foreign exchange, the data delivers a verdict.

The CBN’s logic was simple. Reduce dollar demand and reserves would be protected. Squeeze importers’ access to cheap official dollars and local producers would expand, imports would fall and the naira would stabilise.

The objectives were repeatedly articulated by the CBN under then-Governor Godwin Emefiele. The Bank argued that the restrictions would conserve scarce foreign exchange, reduce pressure on external reserves, encourage domestic production and lessen Nigeria’s dependence on imports. In essence, the policy sought to use foreign-exchange management as a tool for both macroeconomic stability and industrial development.

Eight years later, on October 12, 2023, the CBN reversed the policy in a statement signed by its director of corporate communications, Isa AbdulMumin, conceding that it had pushed demand into the parallel market, weakened the parallel rate and fed price pressures. The question is not whether the policy had good intentions. It is whether the numbers say it worked.

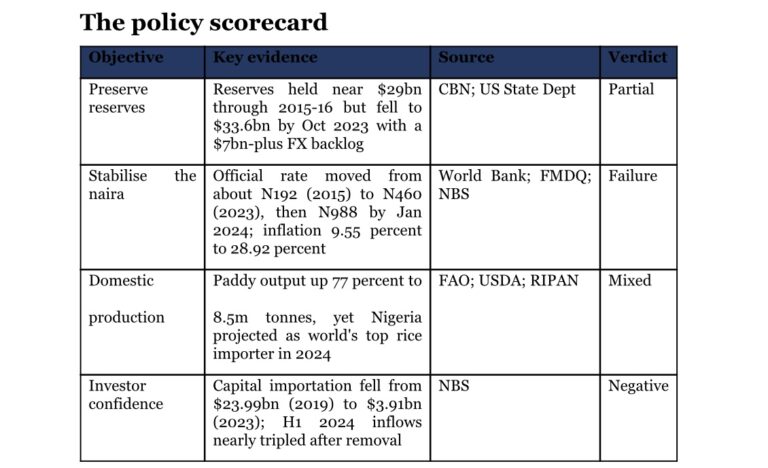

Objective one: preserve foreign reserves

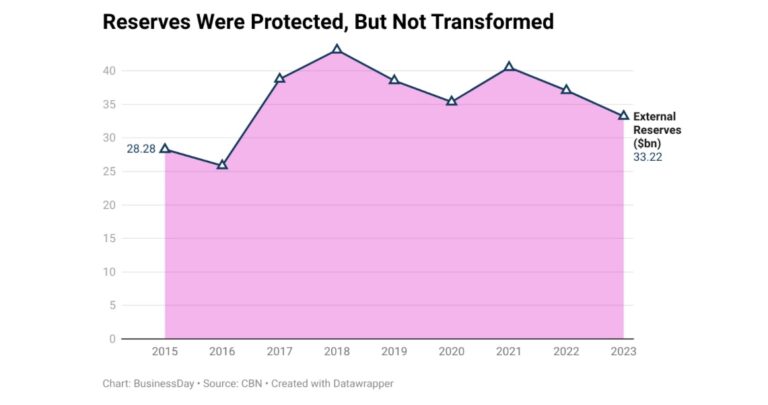

The concern here was legitimate. CBN data cited in the US State Department’s 2017 Investment Climate Statement show gross reserves ended 2015 at roughly $29 billion, fell as low as $23 billion during 2016, and clawed back to about $29 billion by year end. The restriction, alongside outright rationing at the official window, helped slow the bleed through the worst of the oil shock. Given that Brent crude prices had fallen by roughly 50 percent between mid-2014 and mid-2015, supporters argue that reserves would likely have fallen more sharply without administrative demand controls. In that sense, the policy bought policymakers time during a period of acute external stress.

But the protection was never durable, because the policy restricted access to foreign exchange without reducing the need for it. CBN movement-of-reserves data show gross reserves slid from $40.52 billion at end-2021 to $37.09 billion at end-2022 and $34.22 billion by June 2023. When the restriction was lifted in October 2023, reserves stood at $33.6 billion, according to the CBN, while unmet obligations had piled into a backlog exceeding $7 billion by early 2023. Demand had not disappeared. It had been deferred, displaced into the parallel market or stacked up as arrears.

Verdict: Partial success. The policy conserved official reserves at the margin but left the structural dollar shortage, and a multibillion-dollar backlog, intact.

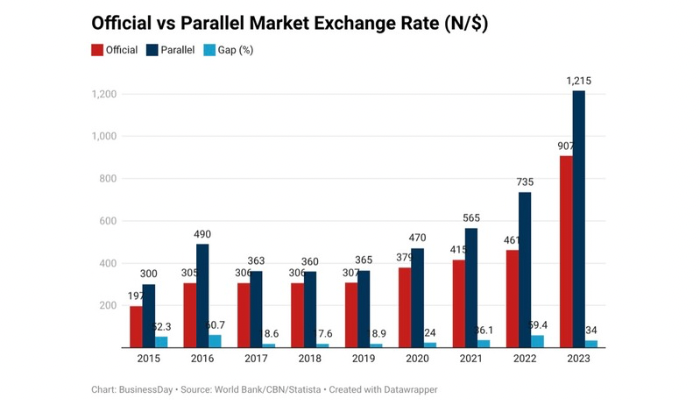

Objective two: stabilise the naira

This was the policy’s most important objective and its clearest failure. The US State Department records that the CBN held the official rate at N196 to N199 per dollar through mid-2016 while the parallel market traded between N350 and N400, a premium that institutionalised round-tripping. World Bank data show the official rate moved from about N192 per dollar in 2015 to around N460 by 2023, even before the June 2023 unification let the market clear.

Once it did, the suppressed demand became visible. FMDQ data show the dollar quoted at N988.46 at the official window on January 3, 2024, more than five times the rate at which the restriction era began. Prices told the same story: headline inflation, 9.55 percent in December 2015 by NBS data, reached 28.92 percent by December 2023. The CBN’s own October 2023 explanation was unambiguous, and the World Bank’s December 2023 Nigeria Development Update agreed, arguing that removal would reduce prices, improve competition and eliminate access distortions.

Verdict: Failure. The policy delayed adjustment for eight years and the naira depreciated severely anyway, with the distortion paid for in inflation.

Objective three: promote domestic production

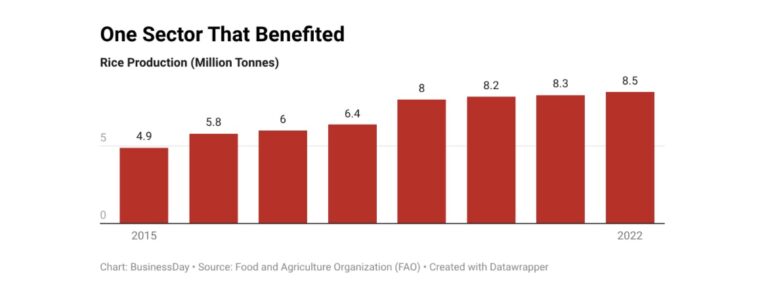

This is where the evidence is most contested, because there were real gains. Rice is the showcase. FAO production data show Nigeria’s paddy output rose from 4.9 million tonnes in 2015 to 8.5 million tonnes in 2022, an increase of roughly 77 percent, supported by the restriction, the CBN’s Anchor Borrowers’ Programme and border controls. The Rice Processors Association of Nigeria reports that integrated mills grew from about 10 in 2015 to more than 100 by 2023.

Yet the gains never amounted to self-sufficiency.

The USDA’s Rice Outlook projected Nigeria would import 2.1 million tonnes of milled rice in 2024, making it the world’s largest rice buyer nine years after the grain joined the list. The broader industrial picture was thinner still. Evidence from the Manufacturers Association of Nigeria (MAN) suggests that the benefits of protection were offset by rising production costs.

Many manufacturers remained dependent on imported machinery, spare parts and intermediate inputs that became more expensive or harder to source under the restriction regime.

MAN’s Manufacturers CEOs Confidence Index repeatedly identified foreign-exchange access as a major constraint.

Although manufacturing’s contribution to nominal GDP rose to 16.04 percent in the fourth quarter of 2023 from 13.49 percent a year earlier, the sector remained constrained by unreliable power supply, high logistics costs, insecurity and scarce foreign exchange. The World Bank argued that the restrictions raised prices, weakened competition and failed to deliver the broad-based production gains policymakers expected. Protection created space. It could not create competitiveness.

Verdict: Mixed. Selected value chains, rice above all, expanded measurably, but no broad-based industrial transformation followed.

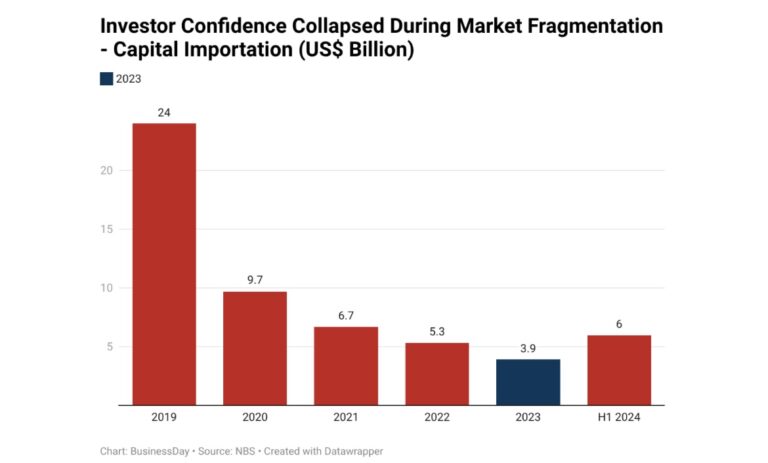

Objective four: rebuild investor confidence

Investor confidence was rarely stated as a formal objective, but it became the policy’s most expensive casualty. Investors price liquidity, transparency and the ability to repatriate capital, and a market running multiple exchange rates with rationed official access offered none of the three. NBS capital importation data trace the damage: inflows fell from $23.99 billion in 2019 to about $3.91 billion in 2023, a decline of roughly 84 percent.

The restriction was not the only cause. COVID-19, global interest rates, oil underproduction, insecurity and election uncertainty all weighed on flows. But causation showed up clearly once the policy died. NBS data show capital importation rose to $5.98 billion in the first half of 2024, nearly triple the $2.16 billion of the first half of 2023, a rebound BusinessDay attributed partly to the easing of currency controls. The CBN reports gross reserves rose from $33.6 billion in October 2023 to $37.9 billion by July 2024 as reforms took hold. Confidence, once the rules became legible, returned faster than it had left.

Verdict: Negative. The policy made access to foreign exchange unpredictable, and measurable inflows collapsed until it was removed.

The flaw in the policy

The policy’s biggest weakness was not its intention but its instrument. The 43-item restriction attempted to solve a foreign-exchange supply problem with a demand-management tool.

Nigeria’s dollar challenge has never been primarily about excessive demand. It has been about insufficient supply. The country earns too few dollars outside crude oil exports, leaving the economy vulnerable to swings in oil prices and production.

Winners and losers

Like many economic interventions, the 43-item restriction created clear winners and losers. The main beneficiaries were domestic rice farmers, integrated rice mills and selected agro-processors that faced less competition from imports. According to the Rice Processors Association of Nigeria, integrated rice mills increased from about 10 in 2015 to more than 100 by 2023.

The costs fell elsewhere. Manufacturers reliant on imported inputs faced higher production costs, small businesses struggled with dollar shortages, and foreign investors grappled with a fragmented exchange-rate system and repatriation concerns. The policy protected some sectors, but it increased costs for others.

What the critics got right

Critics were often portrayed as opponents of local production. Their argument was simpler: import substitution cannot succeed without competitiveness. Muda Yusuf of the Centre for the Promotion of Private Enterprise (CPPE) has long argued that administrative restrictions cannot replace productivity, infrastructure and export competitiveness. Bismarck Rewane of Financial Derivatives Company made a similar point: restrictions can delay pressure, but they cannot remove the causes of scarcity.

Events ultimately proved them right. When the restrictions were lifted, the CBN itself acknowledged that they had fragmented the foreign-exchange market and pushed demand into the parallel market.

What should have been done differently?

The lesson is not that foreign-exchange restrictions should never be used. During a crisis, they can buy time, and in 2015 they arguably did.

The mistake was allowing a temporary measure to become an eight-year framework. A better strategy would have used the restrictions as a bridge while government expanded oil production, strengthened non-oil exports, improved infrastructure, attracted investment and maintained a more transparent exchange-rate system. Instead, the bridge became the destination.

Final verdict

The 43-item restriction was neither a complete failure nor a clear success. It preserved reserves during a period of stress and supported some domestic industries. But it failed to deliver lasting exchange-rate stability, eliminate dollar scarcity or drive broad industrial transformation.

In the end, the policy managed scarcity rather than eliminating it. Nigeria’s foreign-exchange challenge proved larger than a restriction list. It required an economy capable of earning more dollars, not merely limiting access to them.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp