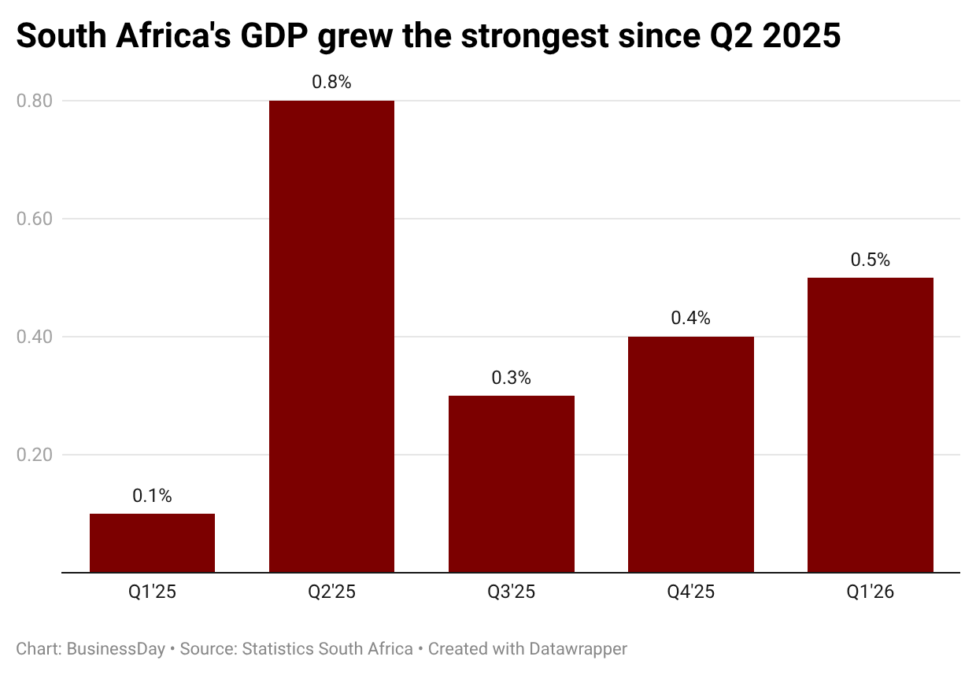

South Africa’s economy expanded at its fastest pace in nine months in the first quarter of the year, showing resilience despite the early impact of the Iran conflict and continued weakness in the manufacturing sector.

Gross Domestic Product in the continent’s biggest economy grew 0.5 percent in the three months to March, up from 0.4 percent in the previous quarter, according to data released on Tuesday by Statistics South Africa. The expansion, which exceeded economists’ expectations of 0.3 percent, marked the sixth consecutive quarter of growth and the strongest performance since Q2 2025.

The growth came despite the outbreak of the Iran conflict toward the end of February, which began to ripple through global energy markets during the latter part of the quarter.

“Finance, agriculture, trade and transport did the heavy lifting on the production (supply) side of the economy. The expenditure (demand) side was supported by a decline in imports and a rise in household consumption, government consumption and exports,” Statistics South Africa said in its GDP report.

While the full impact of the conflict is yet to be reflected in economic output, the statistical agency noted that the sharp rise in fuel prices recorded in April is likely to weigh on second-quarter growth.

Recent business activity data already point to emerging pressures. South Africa’s Purchasing Managers’ Index (PMI), a key leading indicator of economic activity, fell to 49.6 in May from 51.4 in April and 50.8 in March, signalling a deterioration in business conditions.

Finance, agriculture lead growth

Nine of South Africa’s 10 major industries recorded growth during the quarter.

The finance industry was the largest contributor, expanding by 0.9 percent and adding 0.2 percentage points to overall GDP growth.

Agriculture grew for a sixth consecutive quarter, rising by 3.9 percent, supported by strong performance in field crops and horticultural products, particularly fruit.

Trade also extended its growth streak to six quarters, driven by stronger activity in wholesale trade, motor trade, food and beverages, and accommodation services. Retail trade, however, recorded no growth during the period.

The transport and communication sector expanded by 0.7 percent, supported by gains in land transport, air transport and transport support services, although communications activity declined.

Mining activity strengthened on the back of increased production of platinum group metals, gold, chromium ore and diamonds.

Manufacturing remained the main drag on growth, contracting by 0.8 percent for a second consecutive quarter. The decline was driven primarily by weaker output in petroleum and chemicals, iron and steel, and wood, paper and publishing.

Growth in motor vehicles and transport equipment, electrical machinery, textiles and clothing, as well as glass and non-metallic mineral products, was insufficient to offset broader weakness across the sector.

Household spending remains subdued

On the expenditure side, economic activity was supported by lower imports and modest increases in household consumption, government spending and exports.

Household consumption rose by just 0.1 percent, the slowest pace in eight quarters, reflecting continued pressure on consumers.

Utilities and transport were the biggest contributors to household spending, while expenditure on food and non-alcoholic beverages, alcoholic drinks, tobacco products, restaurants and hotels declined.

Spending on miscellaneous goods and services also fell, largely due to lower insurance-related expenditure.

Gross fixed capital formation declined by 1.1 percent after two consecutive quarters of growth, reflecting weaker investment in machinery, equipment and residential buildings.

Exports rose by 0.5 percent, supported by higher shipments of mineral products, agricultural goods and processed food products. Imports, meanwhile, declined, largely due to weaker purchases of precious metals, machinery, mineral products, textiles and edible oils.

Companies also drew down inventories to meet demand, resulting in an annualised inventory reduction of R22.4 billion ($1.22 billion). Manufacturing accounted for the largest drawdown, with stocks declining by R14.5 billion ($790 million).

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp