The rating agency Standard & Poors today delivered a resounding endorsement of the government of President Muhammad Buhari and its economic policies by affirming Nigeria’s rating at B+ with a stable outlook.

It had been feared that given the foreign exchange controls introduced by the Central bank and backed by the president that the rating agency will place Nigeria on a credit rating watch at best but in its report just published, S&P said its reaffirmation of Nigeria’s credit rating is because the country’s non-oil sectors will continue to support GDP expansion in Africa’s largest economy.

The agency said Nigeria’s rating is further supported by “relatively general government and external debt burdens, ample oil reserves and fairly robust growth in recent years.

The agency acknowledged that Buhari has ordered all government revenues be transferred to a single account held at the Central Bank in a bid to curtail corruption and enhance government revenues.

OVERVIEW

The recently-elected All Progressive Alliance government led by (retired) General Buhari has been slow to establish a cabinet, but has announced new appointees at various entities, including the Nigerian National Petroleum Corporation and the Federal Inland Revenue Service, and has announced a series of anti-graft initiatives.

The low oil price environment continues to impact Nigeria’s external and fiscal balances. The poor financial position of many states prompted the federal government and Central Bank of Nigeria to offer them financial support packages.

The Boko Haram militant group has lost significant territorial control in the northeast, but its guerrilla campaign continues to disrupt the region.

We are affirming our long-term sovereign credit ratings on Nigeria at ‘B+’.

The stable outlook reflects our view that Nigeria’s non-oil economy will continue to support GDP growth and that external and fiscal balances will not increase significantly above our current expectations.

On Sept. 18, 2015, Standard & Poor’s Ratings Services affirmed its ‘B+/B’ long- and short-term foreign and local currency sovereign credit ratings on the Federal Republic of Nigeria. The outlook is stable.

At the same time, we affirmed our long-term national scale rating on Nigeria at ‘ngA’ and our short-term national scale rating at ‘ngA-1’.

RATIONALE

The ratings on Nigeria are constrained by our view of its low GDP per capita; low level of development outside the oil sector; significant infrastructure shortcomings; internal political tensions; and weak, albeit strengthening, institutions. The ratings are supported by relatively low general government and external debt burdens, ample oil reserves, and fairly robust growth in recent years.

Nigeria relies on oil and gas for about two-thirds of its fiscal revenues and over 90% of its exports, and sharply lower oil prices during the past year have had a negative impact on its macroeconomic indicators, in particular its fiscal and current account position.

In elections held in March and April 2015, the All Progressive Congress (APC) led by the retired General Mohammaddu Buhari defeated the incumbent People’s Democratic Party (PDP), led by President Goodluck Jonathan. It was Nigeria’s first-ever democratic handover of power between rival political parties, and has been largely peaceful. General Buhari campaigned on an anti-corruption platform and promised to defeat the terrorist group Boko Haram that has plagued Nigeria’s northeast.

Since his inauguration on May 29, General Buhari has engaged with regional leaders in Chad, Niger, and Cameroon, to enhance joint initiatives to tackle Boko Haram, replaced the Nigerian army, navy, and air-force chiefs, and moved military headquarters to Maiduguri in the northeast, close to the center of the insurgency. While Boko Haram has lost significant control of territory, it has managed to continue its guerrilla warfare and bombing campaign; a recent bomb attack targeted, but missed, the new army chief of staff.

General Buhari has not yet appointed a cabinet, ostensibly because he wants to take his time to ensure that he chooses the best people. We consider that the delay may also be owing to the difficult negotiations between various parties that comprise the APC alliance. The APC is a coalition formed from a host of parties. Their main aim was to oust the PDP, but, having succeeded, it is unclear which common goals will enable General Buhari to unite the coalition.

On the economic front, General Buhari’s focus has been on tackling perceived corruption and he has replaced several high-profile functionaries, including the board and the head of the state-owned Nigerian National Petroleum Corporation (NNPC), and the head of the Federal Inland Revenue Service (FIRS). The new head of NNPC has come from ExxonMobil, while the new head of FIRS was the former head of the revenue service in Lagos State–a state with a track record of sharply increasing tax revenues.

In an effort to reduce leakages, General Buhari has ordered that all government revenues be transferred to a single central treasury account for better monitoring and control, and has promised to strengthen Nigeria’s two main anticorruption agencies, as well as amend the constitution to stop providing immunity to elected officials. Although the new government’s transition committee, which is overseeing the transition from the previous government to the new one, has advised the federal government to scrap the fuel subsidy program and consider privatizing government-owned refineries, General Buhari has yet to act on these recommendations. In addition, NNPC may consider renegotiating contracts with international oil companies.

During the past year, largely because of the fall in oil prices, depreciation pressures on the Nigerian naira (NGN) have been high. This prompted the Central Bank of Nigeria (CBN) to raise interest rates, permit two devaluations of the naira, and impose administrative restrictions on foreign exchange transfers. Although some depreciation pressures continue, the CBN has stated that it views the naira as broadly fairly priced. So far, the CBN is resisting further devaluations and in July opted to impose further administrative exchange controls on 41 categories of imported goods instead.

Citing onerous exchange controls and the lack of a two-way foreign exchange market for investors, JP Morgan, the investment bank, announced on Sept. 8 that Nigerian bonds would be removed from its benchmark Emerging Market Bond Indices (JPM GBI-EM) in a phased manner between September and October. This has led to portfolio outflows; however, the delisting has been debated for many months and many investors have already exited the market over the past year. We anticipate that the naira will face further devaluations in 2015 and 2016, largely owing to low oil prices. Despite the CBN’s attempts to protect foreign currency reserves, we expect these to fall to about three months’ worth of current account payments in 2018, compared with five months in 2015.

We expect an average current account deficit of 1.2% of GDP in 2015-2018, down from an average surplus of 3.2% in 2010-2014. We estimate that narrow net external debt (external debt minus liquid external assets) will average 38% of current account receipts (CARs) in 2015-2018. We expect gross external financing needs to average 123% of CARs in 2015-2018, compared with 82% in 2011-2014.

Lower oil prices prompted the previous federal government to respond by sharply revising its proposed 2015 federal budget (excluding state and local governments); the revised budget was passed by parliament in April. Compared with the 2014 federal budget, the revised 2015 budget cut capital expenditure sharply and made less-sharp cuts in recurrent spending. The government based its budget revenue calculations on a US$52 per barrel (/bbl) oil price and 2.27 million barrels of production per day (b/d; down from a budgeted 2.38 million b/d in the 2014 budget), and an exchange rate of 190NGN to US$1.

The lower-than-budgeted exchange rate will support fiscal revenue (the naira is currently trading at around NGN200-NGN220 to US$1) and the fall in the oil price will enable the government to make some savings on the fuel subsidy bill. However, in the first eight months of the year, oil exports have averaged 2.11 million b/d (below the budgeted 2.27 million b/d) and realized sales prices for Nigerian Bonny Light crude have often been below those for average Brent. (Nigerian crude’s new Asian buyers’ refineries do not value Nigerian light-sweet-crude as much as its former U.S. buyers did).

The new government has considered raising value-added tax rates and cutting the fuel subsidy. However, the recent slowdown in economic growth has led it to postpone these decisions and focus on plugging leakages instead.

Although the federal budget has been sharply revised, many state governments did not make significant adjustments to their budgets. As a result, many states are running arrears on supplier contracts and wages. This prompted the new federal government and the CBN to provide support packages amounting to about NGN900 billion, combined, to states and their creditor banks; the ministry of finance will provide about NGN600 billion toward the restructuring of the state’s commercial bank loans, while the CBN will provide support that will be channeled toward paying states’ wage arrears. The support given to each state will be deducted over time from that state’s share of its constitutionally mandated allocated revenues.

Overall, we forecast that Nigeria’s general government debt stock (consolidating debt at all levels of government, including the federal, state, and local government) will grow by 2.7 percentage points of GDP per year on average in 2015-2018. Although nominal gross general government debt has increased in recent years, we expect it to compare favorably with peer countries’ ratios at an average of 22% of GDP for 2015-2018. We also anticipate that general government debt, net of liquid assets, will average 17% of GDP in 2015-2018.

We include debts of the Asset Management Company of Nigeria (AMCON) in our calculation of gross and net debt, in line with our treatment of such entities elsewhere. Over 80% of government debt is in the domestic currency, which mitigates the impact on the government’s debt burden of the recent naira depreciation.

Owing to low crude oil prices, refined petroleum shortages, and slow growth in the second quarter, we expect real annual GDP growth to fall to 3.8% in 2015 and to average 4.6% over 2015-2018. A series of reforms, including in agriculture, and the rapid growth of sectors such as telecoms and financial services, have contributed to non-oil growth momentum in recent years. However, oil production has stagnated, as new investment has been delayed pending the reform of NNPC and the passage by parliament of the long-awaited Petroleum Investment Bill (PIB); oil production has also becomes less attractive due to the fall in the oil price and ongoing oil theft in the sector.

The Nigerian banking sector, while broadly well capitalized, may face asset quality, profitability, and liquidity pressures in the next year. Weakness is likely to stem from loans to oil companies, utilities, and manufacturing companies, and U.S. dollar exposures. There are also concerns that the government’s move to a single treasury account may cause liquidity-related issues in the banking system. In our view, mid-tier banks are likely to be the most at risk. Nevertheless, capitalization, regulation, and governance over the past few years has improved, and this may help limit potential downside risks.

Our local currency rating on Nigeria is equalized with the foreign currency rating because, in our view, the monetary policy options that underpin a sovereign’s greater flexibility in its own currency are constrained by Nigeria’s broadly managed exchange rate regime and still relatively small domestic financial markets.

OUTLOOK

The stable outlook reflects our view that Nigeria’s non-oil economy will continue to support GDP growth and that external and fiscal balances will not increase significantly above our current expectations.

We could lower the ratings if Nigeria’s external and fiscal positions deteriorate beyond our current expectations, or if Nigeria’s policymaking and institutional stability weaken.

We could consider an upgrade if external factors improve considerably (for example, due to a sharp or prolonged rebound in the oil price), or if Nigeria’s external and fiscal balances perform well above our expectations.

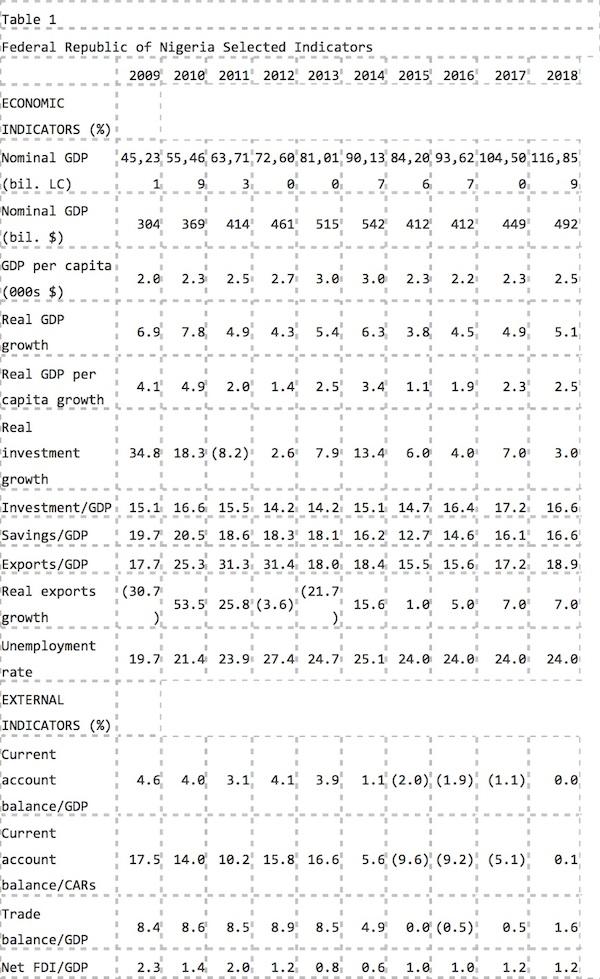

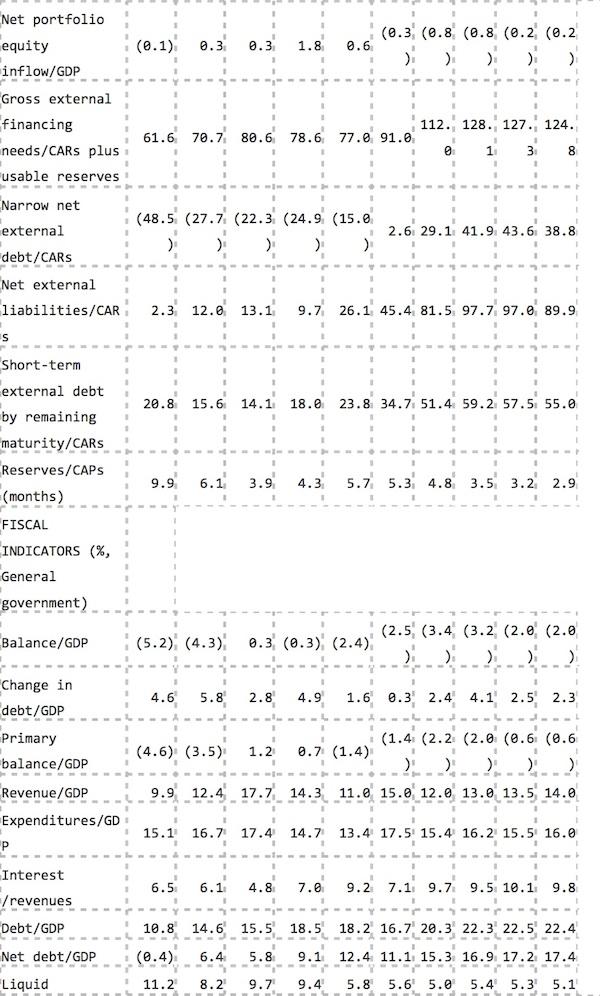

KEY STATISTICS

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp