Nestlé Nigeria reported substantial moderation in revenue growth in full year 2018 (+9.1 percent year on year to N266.28bn) compared to the 34.2 percent year on year surge posted in full year 2017. This temperance in revenue growth reflects tame price and volume increases in the review period.

Whilst the company successfully raised average price of its product portfolio in full year 2017 in response to cost inflation, sustained weakness in disposable income amidst intensifying market competition limited the pricing power of Nestlé in full year 2018.

In addition, Nestlé’s muted price increase might be a competitive response to Cadbury’s decision to maintain competitive prices in the review period.

In our opinion, Nestlé retained market leadership in its food and beverage businesses, which reported revenue growth of 9.0 percent year on year and 9.1 percent year on year, respectively, in full year 2018.

In full year 2019, our expectation is that revenue will improve by 10.5 percent year on year to N294.3bn, supported by volume growth and a mild price increase to slightly account for inflation. In addition, we expect price-induced increase in turnover in the food business.

Moderation in marketing expenses to drive EBITDA margin higher. In full year 2019, Nestlé’s cost to sales ratio declined by 147bps to 57.2 percent in full year 2018 (from 58.7 percent in full year 2017). This followed an equally slower 6.3 percent year on year expansion in cost of sales to N152.4bn (from N143.3bn in full year 2017) compared to revenue growth of 9.1 percent.

This cost efficiency was driven by lower input prices in full year 2018: Sugar (-9.5 percent year on year), Soybean Oil (-14.9 percent year on year) and Crude Palm Oil (-22.0 percent year on year).

However, the company’s EBITDA margin was somewhat flattish at 25.4 percent (from 25.5 percent in full year 2017) due to the impact of higher marketing and distribution expenses (up 23.7 percent year on year to N43.5bn from N35.2bn) driven by spend on advertising (up 50.4 percent year on year).

Going forward, we expect cost pressures to be slightly elevated on expectations of increases in cocoa, soybean oil and crude palm oil prices in first half of 2019.

Expectations of higher cocoa prices are based on supply setbacks in Ghana and Ivory Coast whilst Lunar Year festivities across Asia has supported a rally in soybean oil and crude palm oil prices.

Hence, we forecast full year 2019 gross margin at 42.5 percent compared to 42.8 percent in full year 2018. Irrespective, tamer spend on operating expense is likely to drive EBITDA margin to 25.7 percent (+30bps year on year) in full year 2019.

Profitability to remain supported by lower finance costs. The company’s profit before tax (PBT) rose by 27.6 percent year on year to N59.8bn in full year 2018 from N46.8bn in the prior year, missing our estimate of N63.8bn. PBT improvement was driven by lower finance cost in full year 2018 as finance cost declined significantly to N2.6bn in full year 2018 from N15.1bn in full year 2017.

The decline in finance cost was driven by a net repayment of N51.5bn between full year 2017 and full year 2018, comprising intercompany and bank loans. In our view, the repayments were supported by improvement in Nestlé’s cash flows.

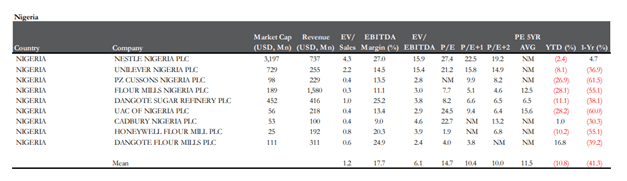

We also note the decline in the company’s net debt to equity ratio to 13.8 percent in full year 2018 from 45.6 percent in full year 2017, which is comparably lower to peers (Cadbury – 32.3 percent, Unilever – 70.1 percent). In full year 2019, PBT is likely to increase to N70.0bn (+17.2 percent year on year) on projected growth in sales and further decline (-71.0 percent year on year) in finance costs.

Free Cash Flow to Equity to remain positive. In line with expectation, Free Cash Flow to Equity (FCFE) came in at N47.5bn in full year 2018 from a negative N28.3bn in full year 2017, buoyed by a N74.6bn net operating cash flow that was mainly driven by efficient management of working capital.

Full year 2018 capex spend amounted to N12.7bn with capex intensity at 4.8 percent (vs. 3.6 percent in full year 2017).

In full year 2019, we forecast capex intensity at 4.1 percent and we expect the company to sustain its debt repayments with total debt (intercompany loans and bank loans) likely to settle at N1.9bn by close of full year 2019. Hence, we expect FCFE to grow by 7.2 percent year on year to N50.9bn in full year 2019.

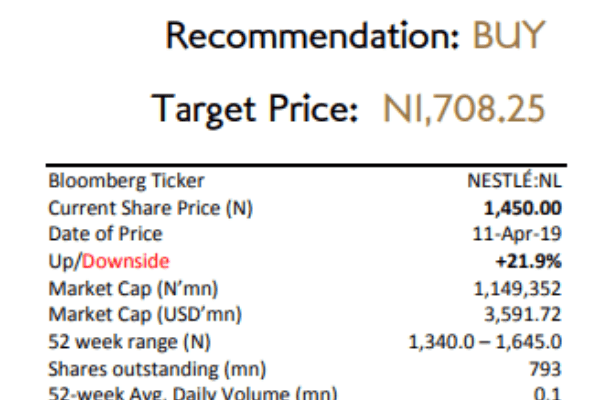

We maintain our BUY rating on Nestlé. We cut our 12-month target price to N1,708.25 from N1,768.62 previously and retain a BUY rating on the stock. In arriving at our TP, we employed a blend of DCF and multiples valuation approaches (P/E and EV/EBITDA).

Our DCF assumptions include adjusted beta of 0.84, risk free rate of 13.93 percent, and terminal growth rate of 5.0 percent. We expect a total return of 21.9 percent (capital appreciation of 17.8 percent and dividend yield of 4.1 percent).

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp