When Stella Odion, who sells foodstuffs at Bola Tinubu Modern Market, Moshalashi, Lagos, faced financial challenges and needed to access a loan to finance her business, she couldn’t get any from banks because of ‘the high interest rate, cumbersome requirements, and process involved.

However, when she heard of digital lenders who could assist, she decided to try it, and her go-to was Credit Direct.

In her words, “I requested N200,000, and the process was seamless.” And since then, her business has been going well. She knew that all she needed was capital, and having to secure that made business go well for her.

“The payment plan was favourable, paying small amounts every week made it easy to return the money,” she added.

For Eniola Olawole, a trader for over four years, said traders in the market like me don’t have any hope for a pension, but when Credit Direct came, they introduced pensions to us. When I want to save money, I do use Ajo, and that is how I get money to restock my shop.

But Credit Direct changed everything, she said. “I knew them when they came to the market to advertise for me. One thing I like about their service is that they don’t make it so open when the collection period arrives; your secret will not leak out.”

Many small traders in Nigeria’s bustling informal economy, market women, artisans, and street vendors have long been excluded from structured financial systems.

Their limited documentation, irregular cash flows, and lack of credit history make them unattractive to traditional banks. Yet, this segment accounts for about 65 percent of Nigeria’s GDP and over 80 percent of employment, according to the National Bureau of Statistics (NBS).

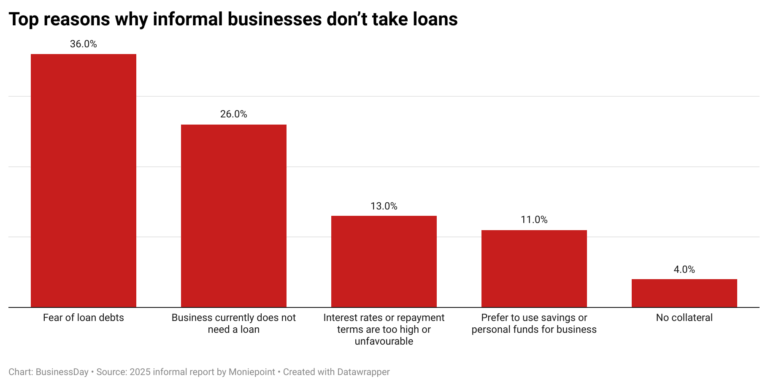

According to the 2025 Informal Economy Report by Moniepoint, 51 percent of small business owners don’t intend to take loans, citing fear of bad loans, high interest rates, or repayment terms that are too high or unfavourable, among other reasons.

However, Credit Direct, a non-bank financial institution under FCMB Group, is taking a different approach. Its mission extends beyond providing loans. It is creating pathways to pensions and insurance for market traders who had never imagined owning such safety nets.

In November 2024, Credit Direct began a pilot financial inclusion market outreach across Lagos markets to gauge informal traders’ appetite for structured financial products. The initiative formally launched in March 2025, targeting women and men who rely on daily cash turnover but often lack access to credit, insurance, or retirement plans.

“So far, over 2,201 new beneficiaries have been reached through this outreach,” said Sheba Umunna, head of financial inclusion and impact, Credit Direct. “Many of them are first-time participants in any formal financial service.”

The model is simple but powerful. Agents visit markets, meet leaders of traders’ associations, and introduce Credit Direct’s suite of microfinance tools—loans, insurance, micro-investment, and pension plans.

“Our approach is human and community-driven,” she said. “We plan to visit twenty markets across Lagos, and this outreach is carried out every quarter.”

Read also: How Zeeh Africa’s direct debit solution is tackling Nigeria’s rising loan defaults

Umunna disclosed that some of the markets they visited include Ayewadun market (Ikola); Ibafo market; Ifelodun market (Alakuko); Igando market; Ikotun market; Irepodun Oja Oba Odejobi market (Council market); Jankara market; Kosofe market; Kudaki market (Egbe); Mandela market; and Mile 12 market, among others.”

Building inclusion beyond lending

Tajudeen Hassain, who has been selling herbs for over 40 years, said, “I used to save money at home and sometimes collect loans from others just to buy goods.” However, everything changed when I started using Credit Direct; their low interest rate with free pension really attracted me, and that’s how I began using their services.

Apart from savings and loans, Hassain said they introduced insurance services to us. He added that with the Credit Direct loan, I used it to pay school fees for my children.

Credit Direct’s loans typically attract a 5 percent monthly interest rate over three months, but that figure includes more than just lending costs.

“Out of the 5 percent, 1 percent funds insurance, another 1 percent funds pension contributions, while 3 percent covers administrative and capital costs,” said Emeka Ucheaga, head of strategy and financial inclusion at Credit Direct. “We are not in this for the profit margin; we’re in it for the impact.”

Under this system, every trader who takes a loan automatically gets a pension account opened with FCMB Pensions, Credit Direct’s partner. The company contributes a portion of each repayment to that pension account, jumpstarting a savings culture most traders never had.

“Our goal is to help them build the discipline of earning from what they have; we call this micro-investment,” Ucheaga noted. “They earn daily, so we designed a weekly repayment model that fits their lifestyle. Over time, they begin to see that financial planning isn’t just for salaried workers.”

Tackling the trust deficit

One of the biggest challenges for financial inclusion in Nigeria’s informal economy is trust. Many traders distrust digital lenders and financial institutions due to past experiences with exploitative microfinance schemes or aggressive loan recovery tactics.

According to the 2023 EFInA Access to Finance Survey, lack of trust and understanding of the product emerge as major barriers to acceptance and usage of financial services.

Lack of trust fell to 6 percent in 2020, from 5 percent in 2023, while understanding of the product rose to 6 percent from 1 percent.

Credit Direct’s teams are embedded in the heart of market communities, building trust where it matters most. “We’re not some faceless lender,” said Ucheaga, Head of Strategy and Financial Inclusion. “We show up, connect, and speak the traders’ language. When people see we’re real, they listen.”

This people-first approach sets Credit Direct apart from others, more focused on pressure than partnership.

“We’re not here to squeeze traders,” Ucheaga added. “We’re here to help them grow.”

Read also: Seed surge, mega-deal drought as Africa’s venture capital market enters new normal

Merging finance with welfare

Beyond loans and pensions, Credit Direct’s outreach introduces micro-investment options, encouraging traders to set aside small amounts regularly and earn interest.

“Even if they save as little as N500 a week, it accumulates over time,” Ucheaga said. “It’s not just savings; it’s teaching the habit of investment.”

Every borrower is also automatically enrolled in a micro-insurance scheme that covers their loan in cases of death or serious illness. This ensures that their families aren’t burdened in times of crisis.

For the insurance services, Credit Direct partnered with emPLE, a financial services company dedicated to providing insurance and investment solutions.

Adeorunke Smith, head of bank assurance at emPLE Life Assurance Limited, said the partnership between our company and Credit Direct is aimed at making insurance more accessible to market men and women across Nigeria, especially those in the informal sector.

“The partnership operates as an embedded insurance model. Credit Direct has already purchased the insurance packages, such as term life insurance that covers debt repayment, fire insurance, hospital cash back, and medical expense cover for market men and women.”

“So, once you are a customer of Credit Direct, whether a new or existing one, you automatically have access to these insurance covers. Credit Direct pays for these packages monthly, ensuring that their customers are protected without any extra cost or separate purchase,” she said.

What to expect in the coming year?

Credit Direct is also exploring digital commerce linkages to further support traders.

“We’re developing a platform to connect our traders to our larger customer network,” Ucheaga said. “If we help them sell their products, they can grow faster and repay more easily. We want to create an ecosystem of shared growth.”

“The market has been kind to us and we want to continue reciprocating the kindness in line with our FCMB Group purpose, because business to us is first impact before profit,” he said.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp