As Nigeria marked 64 years of independence yesterday, October 1, 2024, the incumbent President, Bola A. Tinubu, delivered a speech to commemorate the important event in Nigeria’s history. The speech prompted me to write this article.

“For Nigeria to attract FX, most especially in the form of FDI, there is a need to disincentive divestments in the oil and gas sector as well as manufacturing; reduce investor apprehension about the Nigerian business environment; tackle insecurity, regulatory bottlenecks, and infrastructural deficits; and ensure structural barriers to foreign capital inflows are beaten.”

He made mention of attracting $30 billion in foreign direct investments (FDI) in one year.

“Thanks to the reforms, our country attracted foreign direct investments worth more than $30 billion in the last year.”

This does not mean $30 billion has actually flowed into Nigeria. However, agreements have been signed between Nigeria and foreign investors, promising to deliver this amount over the course of 5-8 years. This might seem like counting our chickens before they are hatched. Hence, we must do everything as a nation to ensure these investments do not only materialise but soon too. This is so because FDI has largely dried up in recent times. Take, for example, out of total capital imported between 2023Q2 and 2024Q1 of $6.14 billion, only a relatively meagre $448.95 million is in FDI. This comes to a paltry 7.31 percent of total foreign investments in FDI. The larger chunk of imported capital into Nigeria is hot money like Treasury bills, OMO bills, and foreign loans. While this helps with the availability of foreign exchange (FX) or liquidity, it is not sustainable.

For Nigeria to attract FX, most especially in the form of FDI, there is a need to disincentive divestments in the oil and gas sector as well as manufacturing; reduce investor apprehension about the Nigerian business environment; tackle insecurity, regulatory bottlenecks, and infrastructural deficits; and ensure structural barriers to foreign capital inflows are beaten.

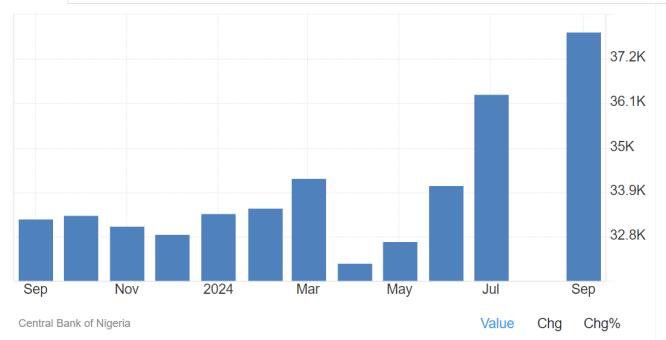

Secondly, for the foreign exchange reserves (FX reserves), it might have been one of the bright spots of the administration. As it made it better than it met it. Nigeria’s FX reserves were $35.14 billion on May 26, 2023, but have since increased to $38.05 billion by September 27, 2024, despite the deployment of the reserves to clear almost the entire FX backlog. This is clearly reflected in the president’s speech, where he mentioned:

“We inherited a reserve of over $33 billion 16 months ago. Since then, we have paid back the inherited forex backlog of $7 billion. …. Despite all these, we have managed to keep our foreign reserve at $37 billion. We continue to meet all our obligations and pay our bills.”

Nonetheless, it must be added that the entirety of the backlog might not have been cleared as only “valid claims” have been settled. This clearly means there are claims the Central Bank of Nigeria (CBN) feels do not merit being attended to. Furthermore, according to IATA, 98 percent of trapped airlines funds have been cleared.

Read also: Nigerian economy resilient but remains fragile – NESG

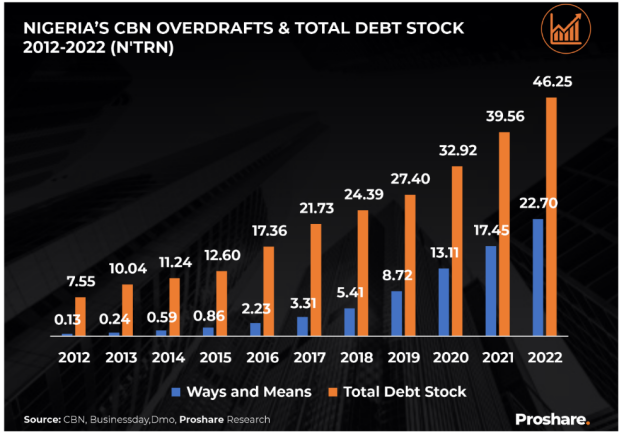

Thirdly, the ways and means advances are not cleared as they have not been repaid, partly or fully. They have only been securitised, meaning converted into a security to be bought and sold. So, the part of the president’s speech where he mentioned that should have been better worded:

“We have cleared the ways and means of debt of over N30 trillion.”

The President’s immediate predecessor ballooned the M&M Advances from less than 1 trillion naira in 2015 to a whopping 22.7 trillion naira, which securitisation was approved by the Nigerian Senate on May 23, 2023. And a further 7.3 trillion naira in W&M Advances securitised through Senate approval on 30th December 2023. The securitisation means the Nigerian state would be paying back the accumulated debts from the CBN over the course of 40 years. And the catch is the rate of interest to be paid, which is now in a single digit instead of what would have been without the securitisation.

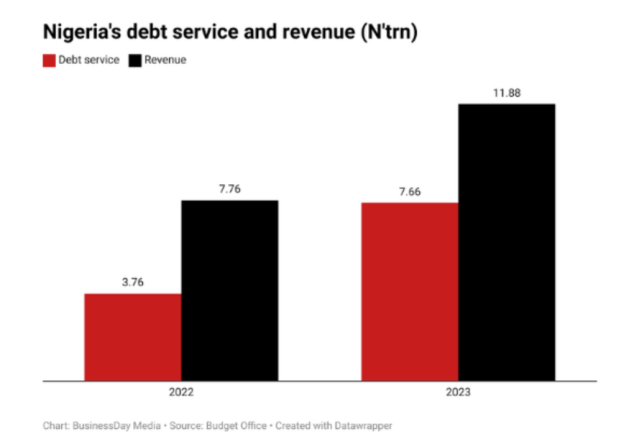

While the World Bank recommends a debt service-to-revenue ratio not exceeding 22.5 percent for developing economies like Nigeria, Nigeria has been struggling to keep up with its debt service. Take, for example, in 2020Q1, 96.7 percent of government retained revenue was used to service debts. This got worse in 2021 Q1 at 123.2 percent; eased a bit in 2022 Q1 to 120.5 percent. It, however, ballooned to 149.5 percent in 2023Q1. With the coming of the Tinubu administration, it crashed to 74.3 percent in 2024Q1. This can be largely attributable to the hike in the pump price of fuel as well as the depreciation of the naira in terms of the dollar. What is more, the securitisation for the over 30 trillion naira in W&M Advances reduced the rate of interest charged. So, the President’s assertion that:

“We have reduced the debt service ratio from 97 percent to 68 percent.”

This does not mean that it is uhuru. Nigeria has been accumulating debts in recent years. And these have to be paid back eventually. So, unless all the necessary measures are taken, Nigeria may go back to using 100 percent of retained income to service its debts. This, however, can be avoided by continuous structural reforms, sensible fiscal management, increased revenue, increased oil production, and seeking loans on concessional, not commercial, terms.

Samson G.SIMON, Chief Economist ARKK Economics & Data Limited.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp