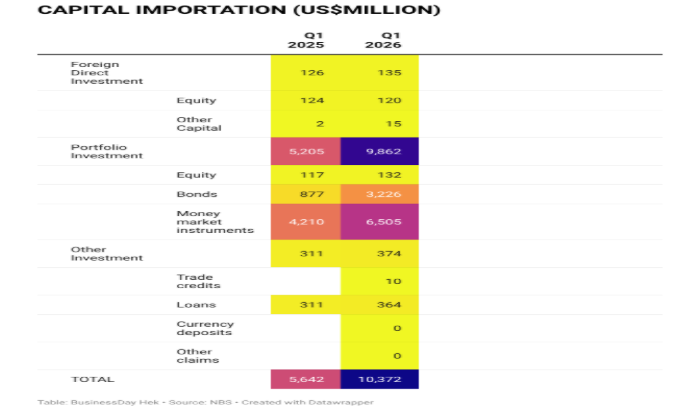

On first inspection, the number looks like a vindication. Nigeria’s capital importation surged 84 per cent year-on-year to U$10.37 billion in the first quarter of 2026 (Q12026), according to the National Bureau of Statistics (NBS). For an administration that staked its reputation on liberalising the foreign exchange window, this appears to be the ultimate market endorsement.

But the configuration tells a different story as foreign portfolio investment (FPI) dominated with US$9.86 billion, more than 95 percent of the total. Meanwhile foreign direct investment (FDI), the kind that builds factories, creates durable employment and transfers technology, nibbled at a meagre US$135 million, or 1.3 per cent.

This imbalance is not new, but its scale underscores a persistent structural weakness. The macroeconomic surgery of 2023, comprising naira unification, fuel subsidy removal, and interest rate hike, succeeded in luring back yield-thirsty foreign portfolio investors.

These were attracted by elevated domestic interest rates and high yields on treasury bills, bonds, and money market instruments. And so did capital came, wearing running shoes.

The NGX sugar rush and pricing conundrum

This torrent of currency has hit the Nigerian Exchange (NGX) like pure adrenaline, with the bourse capturing the mood with theatrical enthusiasm. The All-Share Index is riding a wave of foreign re-entry, has returned over 50 per cent this year, driven by valuation anomalies that would glisten even a quantitative analyst’s eyes.

The NGX stocks are fundamentally cheap because Nigeria’s country risk premium has been astronomically high. So as the naira stabilises, funds from the UK and US are piling in to capture that spread. However, this is not a development story; it is a carry trade story. The banking sector, which facilitates this flow, cornered US$7.55 billion and 72.79 per cent of all capital, while the entire production and manufacturing sector contented with a pitiful US$152 million

Risk, reality, and embedded bubble

The foregoing picture presents a binary calculus for you, the Hek reader. On one hand, you have momentum. Inflation has eased, the fiscal deficit has widened, and pre-election liquidity is abundant. The planned Dangote Refinery IPO could act as a further catalyst, dragging frontier market allocations higher.

On the other hand, you have physics. What goes up on hot money must eventually be maintained by, as yet absent, cold fundamentals. Manufacturing remains uncompetitive due to energy costs, agriculture is starved of mechanisation, and the real sector is being suffocated by the very high interest rates hat make the treasury bills so attractive to London and New York.

While we are not at bubble valuations yet as NGX equities still offer genuine earnings yields, the composition of the flows is a classic bubble forerunner.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp