Providus Bank’s acquisition of Unity Bank, a financially troubled yet systematically important bank, is the price the fast-growing regional bank is willing to pay to go national.

Several banking analysts and investors were taken by surprise after the Central Bank of Nigeria (CBN) gave the green light for a merger between Providus bank and Unity bank last week.

On one hand is Nigeria’s fastest growing bank by assets in the last three years and on the other is a financially unstable bank with negative retained earnings.

The coming together of Providus and Unity appears the most unlikely marriage, but multiple sources interviewed by BusinessDay provided inside details into the driving factors of the deal and how it is a “coincidence of desires.”

Read also: World Bank predicts bigger diaspora remittance for Nigeria in 2024

Merger vs Acquisition: Another Access-Diamond in the offing?

The Providus-Unity deal has been described as a merger by all the three parties involved from the CBN to both banks.

While the deal has been structured as a merger, multiple sources familiar with the deal say Providus is acquiring Unity Bank.

Providus is providing a lifeline for a systematically important bank that risks going under while riding the bank to its national bank aspiration.

Providus is the healthier of the two banks and anything short of an acquisition which gives Providus the complete power to transform Unity bank could quickly become a poisoned chalice for Providus.

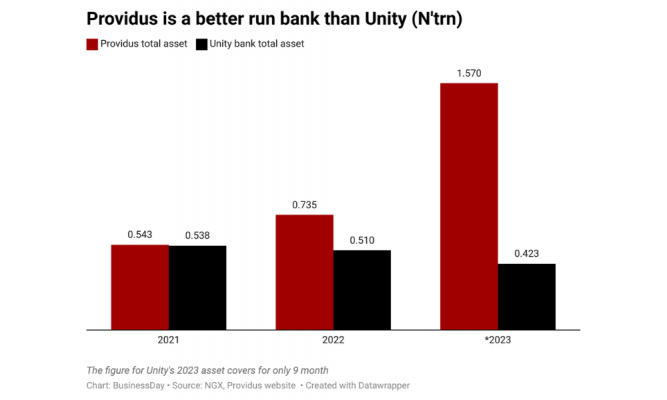

With shareholders’ funds exceeding N96.2 billion and total assets of N1.5 trillion as of December 2023, Providus Bank has demonstrated robust growth and sound financial management. The bank has grown its assets by 189 percent in the space of three years from N543 billion in 2021.

Unity Bank, which had negative shareholder funds of N190 billion and total assets of N423 billion, according to its unaudited accounts for the period ending September 2023, has not exactly demonstrated sound financial management. The bank is yet to publish its full year results.

Both banks have very different corporate governance cultures but with this acquisition, Unity will be run by Providus, paving the way for a much bigger bank that has the imprints of Providus.

Interviews with some staff of Providus also revealed the deal is more of an acquisition than a merger.

The staff of Providus expect a raft of promotions and postings to come with the “merger.” Word has been going around within the bank that the staff at the headquarters will fill out top management positions that will become vacant at Unity bank’s branches.

Read also: CBN-backed Unity Bank takeover safeguarded Northern Nigeria financial lifeline

They seem to believe their bank is acquiring Unity and not merging with it. “Forget what is being said, it’s more of an acquisition than a merger,” a staff of the bank told BusinessDay.

“There will be little or no room in the new institution for Unity bank staff who ran their bank aground in the first place,” the staff who did not want to be named said.

The structure of the deal between Providus and Unity Bank is similar to that of Access and Diamond Bank.

The management of Access and Diamond bank both said the deal was a merger but it turned out to be an acquisition with Access swallowing Diamond bank’s operations, leaving little room for the management staff of Diamond bank.

This deal was beneficial for Access because Diamond Bank had a strong retail base and digital banking infrastructure. These variables were useful for Access, which needed to lower its cost of funds to maximise profits.

Providus gets the northern reach of Unity

For Providus, the acquisition of Unity Bank will transform the regional bank, founded in 2016, into a national bank overnight.

Unity bank has some 220 branches across the country with a northern reach that Providus will be looking to leverage.

Unity Bank has one of the most extensive branch networks in northern Nigeria, inherited from some of its legacy banks, particularly Bank of the North, Tropical Commercial Bank, Intercity Bank and New Africa Bank.

Unity Bank’s origins trace back to the banking consolidation of 2004, which saw the merger of nine struggling banks into a single entity.

Despite its troubled legacy, Unity Bank held a unique position in Nigeria’s financial ecosystem, particularly in the northern regions. The bank was the lifeline for many communities, servicing states and local governments where access to financial services was limited.

Unity Bank’s 220 branches plus Providus Bank’s 23 branches will give the new banking entity a branch network of 243 branches across Nigeria, ranking it among the top 10 largest Nigerian banks in terms of branch network.

A joint statement put out by the managements of both banks also lists Unity bank’s “strategic niche in the agriculture business” as a key benefit Providus is expecting from the deal.

Read also: Lack of BVN stalls 18% Heritage Bank depositors from reimbursement NDIC

“By combining Unity Bank’s extensive branch network and deep-rooted customer relationships with Providus’s digital prowess and innovative spirit, we aim to deliver a seamless blend of traditional and modern banking services,” the statement read.

Unity gets Providus lifeline

For Unity Bank, the “merger” with Providus is a lifeline for a crumbling bank.

Unity Bank has been in financial trouble for years.

The bank recorded negative retained earnings of N428.75 billion in the nine months through September 2023.

Retained earnings are the portion of a company’s cumulative profit that is held or retained and saved for future use. A company with negative retained earnings is an indication that the company has accumulated losses in previous years, resulting in a deficit in its retained earnings account.

Unity bank’s negative retained earnings means the bank’s net income has not been sufficient to cover its losses or fulfill other financial obligations.

The bank reported a loss of N428 billion in the nine months ended September 2023 and negative shareholder funds of N190 billion.

Negative shareholders’ funds suggest that the bank’s liabilities exceed its assets, indicating a weakened financial position.

The bank has been stuck with a negative return on assets and equity, a sign the bank is not making profit and is unable to use its assets effectively.

Investors are well aware of the financial mess Unity finds itself in, hence the reason the bank has a negative price to book ratio of 0.090x, the worst of any bank. A negative price to book ratio indicates that a company has more liabilities than assets.

The bank reported total liabilities of N613.6 billion in the nine months through September 2023 compared to N423 billion in total assets, leaving a shortfall of N190 billion.

The acquisition by Providus preserves the safety of Unity Bank’s depositors’ funds and its banking franchise.

It also allows Unity Bank and its shareholders to be part of a fast growing and well managed institution with bright prospects.

Read also: Afreximbank to double intra-African trade financing to $40bn by 2026

A coincidence of desires delights CBN

The merger was described as a coincidence of desires by one of the sources interviewed by BusinessDay.

On one hand is a bank with the desire to become a national bank and on the other hand is a bank that is in financial doldrums but is considered too “big to fail” by the CBN.

The CBN’s intervention, a N700 billion loan to plug the hole in Unity Bank’s books, was supposed to serve as a sweetener for a deal with Providus bank. Providus may have balked at taking on the liabilities of Unity Bank without the CBN’s support.

The CBN had compelling reasons to speedily bless the union of Providus and Unity Bank and provide the necessary support to make the deal go through.

First is that the apex bank has found a solid bank to take another systemically-important bank out of a hole.

Providus bank’s track record gives confidence in its ability to transform Unity bank.

By putting the management of the combined bank in the hands of Providus, known for its efficiency, the CBN greatly enhances the prospects of repayment of the financial accommodation extended to Unity Bank.

The union of both banks is also important for financial inclusion, which is one of the key goals of the CBN in a country where 37 percent of rural Nigerians are financially excluded.

Farmers and dependents are the populations most likely to be excluded from the financial fold, according to a survey by Efina, which provides the most comprehensive data on financial inclusion in Nigeria.

Here’s where Unity bank comes in.

The bank’s depositors are mostly small and medium scale enterprises in rural areas and farmers in the north, which implies that the bulk of the bank’s depositors are people the CBN is trying to keep within the financial fold and expand their access to more financial services beyond simply account ownership.

Read also: CBN’s unsettled forex forward increases business risks, economic turmoil — MAN

If Unity bank fails, it will derail the CBN’s effort to boost financial inclusion.

By preserving the branch network and customer accounts of Unity Bank, the CBN is able to ensure continued access to banking services for millions of urban and rural customers in several areas in the north, including those areas where Unity Bank is the only bank.

In summary, the CBN’s endorsement of this merger reflects a broader strategy to maintain stability in the banking sector while ensuring that underserved regions, particularly in the north, continue to have access to essential financial services.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp