John Mohammed took loans from his bank, family and friends to keep the lights on in his car dealership after the business fell on hard times in 2015.

The loans made sure it was business as usual for John as they bought time for his car dealership to rebound.

Eight years later, Mohammed, 64, has borrowed to the hilt and his car dealership is still showing no signs of recovery. When Mohammed racked up the debt, he failed to invest it in any income-generating venture.

With little to show for years of tapping debt and no more room to borrow without triggering a debt crisis, Mohammed must now spend the little loan he can secure more efficiently and seek out viable ways of getting equity cash – the option he had avoided in the early days of his struggling business. Weaning himself off the pile of debt that has carried him for so long promises to be no small task.

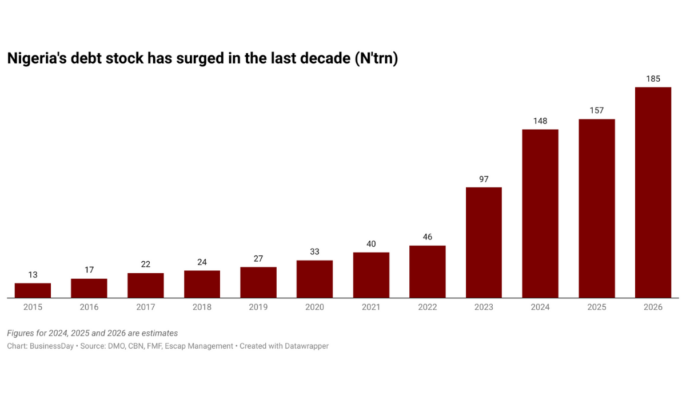

Mohammed’s age is not the only similarity he shares with Nigeria. Like him, Nigeria also borrowed to the hilt in the last nine years to buy time for dwindling oil revenues. Nigeria’s debt stock, which includes cash borrowed by the Federal Government and the states, jumped more than seven-fold to N117.5 trillion as at March 2024 from only N13 trillion in 2015.

Debt, when unlawful borrowings from the Central Bank is factored in, rose to become an unlikely main source of budget revenue in the period, after years in which oil income contributed the bulk of revenues.

There are scant gains to show for most of the borrowings, a fact the previous government countered by pointing to significant investment in rail infrastructure. Critics however said even the investment in infrastructure was not well targeted.

Take the $823 million Abuja Light Rail which the government took Chinese loans to build and cost $50 million a year to service.

The government reopened the line two months ago after shutting it down for four years. Today, the line operates free rides for commuters and is in no state to earn the revenues required to repay the loans taken to build it. It has also not added any significant economic value.

Economists are scratching their heads over how a cash-strapped country with a considerable infrastructure deficit can afford to take a little under a billion dollars in loans to roll out such an expensive rail service which rots away for four years after its completion before resuming this year with free rides for scarce commuters till the end of the year.

Read also: UPDATED: Top 10 African countries facing the biggest IMF debts

The problem with the rail line is that at one end lies the airport, a place where most people who can afford to fly typically arrive by car, and at the other end is an isolated area of the so-called Central Business District in the capital city of Abuja, where the road in front of the station is more often filled with herders driving cattle to grazing land than anyone headed to or from work. Out back is scrubland where people fleeing violence in the north of the country have built shacks. An additional 18 kilometres of track was built toward the suburbs but never saw any service.

“It is one thing to be a poor country dealing with a severe scarcity of resources but it is soul-crushingly painful to see wastage of the little resources a can muster,” Feyi Fawehinmi, an accountant, said.

It’s this type of wastage that Nigeria can no longer afford.

The government has spent loans recklessly and must now face a future where it can’t borrow as much anymore. It must therefore be more efficient in utilising its scarce resources, whether loans or hard-earned revenues.

Nigeria’s debt stock has grown to the point where the country’s debt to GDP has more than doubled to 49.73 percent from around 20 percent.

While 49.73 percent is still lower than the Sub-Saharan Africa average of 58.5 percent and emerging market average of 69.4 percent, the country’s high debt-to-revenue ratio means Nigeria is in a worse position than most other countries to service its debt.

“By 2026, we project the debt stock will reach N185 trillion,” said Esili Eigbe, director at consulting firm, Escap Management Ltd.

“Despite this, authorities seem unfazed, citing a lower debt-to-GDP ratio compared to global peers.

“However, the focus should be on the debt-to-government revenue ratio in our opinion, which places Nigeria among the countries least capable of repaying their debt,” Eigbe said.

Debt crisis

Nigeria ranks fourth among countries with the highest debt-to-revenue ratio, signalling a high risk of a debt crisis. Only Sudan, Venezuela and Yemen have higher debt-to-revenue ratios than Nigeria

Petrodollars are still not flowing as they used to and part of future production has been used to secure cash today in oil-backed loans taken by the government.

Fuel subsidies, additional borrowings, FX devaluations, and higher borrowing costs mean Nigeria’s total debt could hit N148 trillion by year-end.

“Rising debt levels put Nigeria at serious risk of a debt crisis,” Eigbe noted.

“With the potential return of Donald Trump in the United States and a likely oil price collapse, the government must act swiftly,” Eigbe said.

A debt crisis has severe implications for Nigeria. It would trigger a naira devaluation, credit downgrade, economic fragility, higher borrowing costs, persistent inflation, loss of investor confidence and social unrest.

The negative impact on local businesses would be severe and must be avoided at all costs.

Way out

Analysts at Escap Management Ltd are of the view that the government must eliminate fuel subsidies, adopt austerity measures, restructure its debt and even seek emergency funding from the International Monetary Fund (IMF) and World Bank in the short term to avoid a debt crisis.

There’s also the need to boost oil production, adjust monetary policy and introduce a legal debt ceiling.

In the medium term, the government has been urged to implement revenue-enhancement reforms and restructure the civil service.

Development of social safety nets, public-private partnerships to boost infrastructure development, effective public communication and engagement as well as addressing security challenges are also seen as crucial steps to take in the medium term to avert a debt crisis. Long-term measures include economic diversification, strengthening public institutions, human capital development and introduction of favourable trade and investment policies.

Time to get serious with equity funding

President Bola Tinubu has no choice but to seek other creative ways of generating revenue for the cash-strapped government with the debt option largely out of it.

For instance, all eyes are on Tinubu to finally raise meaningful cash from the privatisation of idle government assets which seemed almost impossible under the watch of the previous administration.

Tinubu is aiming to raise as much as N298.4 billion from the privatisation of national assets in 2024 to fund the cash-strapped government’s budget, according to data obtained from the Budget Office.

Africa’s biggest economy generated zero cash in the first nine months of 2023 from its budget of N154.6 billion as privatisation proceeds. In 2022 and 2021, the country also generated nothing from asset sales from its budget of N90.7 billion and N205.2 billion respectively.

Failure to raise any cash from privatisation will leave the Federal Government with an even larger budget deficit and that could lead to more borrowing or lower than planned capital expenditure.

The President’s Policy Advisory Council recommended last year that the government sell down its stake in the most joint-venture oil and gas assets, a proposal that is estimated to bring in up to $17 billion.

BusinessDay had earlier reported that Nigeria plans to unlock the N180 trillion trapped in dead or idle government assets as a renewed hunt for cash heats up.

Over 70 entities have been captured in a national asset register that aims to identify the country’s vast and mostly idle assets, according to the Ministry of Finance Incorporated, whose work it is to build the critical database that will help unlock badly needed cash for the government.

“The previous administration resorted to borrowings to make up for the sizable public revenue shortfall but I’m not sure the current administration can do that with the debt stock now reaching unsustainable levels,” said Muda Yusuf, an economist and CEO of the Centre for Promotion of Private Enterprise (CPPE).

“Indeed, the hard work starts now,” Yusuf said.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp