Nigeria’s growing use of dollar-pegged stablecoins is reshaping how households and businesses move money across borders, reducing payment costs and delays while creating new challenges for the Central Bank of Nigeria (CBN) and other policymakers concerned about monetary control and financial oversight, according to an International Monetary Fund (IMF) analysis.

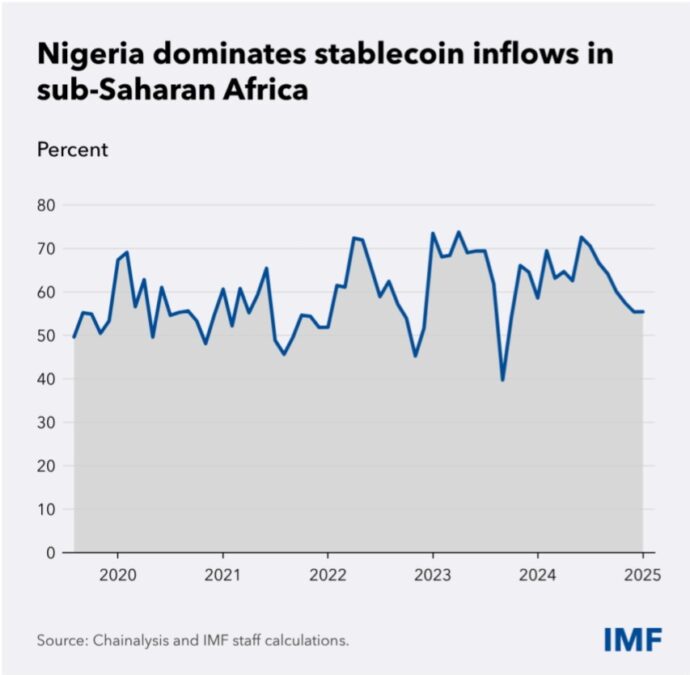

The IMF said Nigeria received about $59 billion in crypto-asset inflows between July 2023 and June 2024, highlighting the scale of adoption in Africa’s largest economy. The country ranked second globally on Chainalysis’s 2024 Global Crypto Adoption Index and sixth in 2025, while accounting for roughly 60% of stablecoin inflows into sub-Saharan Africa since 2019.

In a blog post published on Tuesday by the IMF, Axel Schimmelpfennig, the Fund’s mission chief for Nigeria, and Bo Zhao, an economist in the IMF’s Strategy, Policy and Review Department, said stablecoins have evolved from a niche technology into a significant channel for cross-border payments.

“Nigerian households and small firms are moving money across borders in a new way: via smartphones, digital wallets, and U.S. dollar-pegged crypto assets known as stablecoins,” the authors wrote. “What began as a niche technology has become a meaningful cross-border payments channel.”

Read also: Africa still dominates global growth rankings despite IMF downgrades

The findings build on the IMF’s 2026 Article IV consultation with Nigeria, which examined the country’s economic outlook and policy challenges following sweeping reforms to the foreign-exchange market and fuel subsidies.

As part of that assessment, IMF staff analysed the growing role of stablecoins in Nigeria’s financial system, warning that while the digital assets can improve access to cross-border payments and support financial inclusion, their increasing use could complicate monetary policy implementation and regulatory oversight.

According to the IMF, stablecoins allow users with internet access to receive remittances and make international payments within minutes, often at lower cost than traditional channels. The authors noted that the average cost of sending $200 to sub-Saharan Africa remains about 9% of the transaction value, compared with a global average of 6%, citing World Bank data.

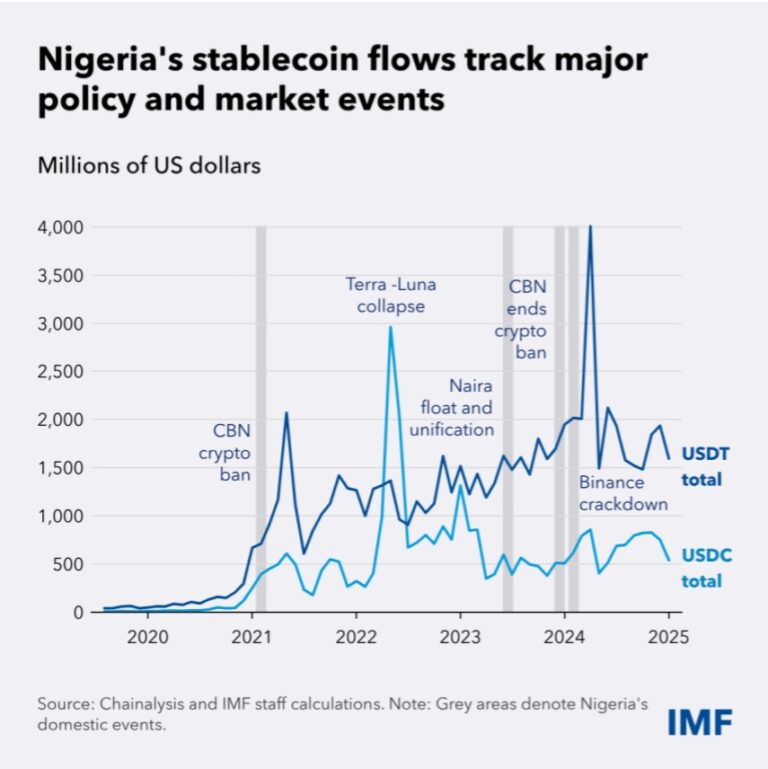

The Fund said domestic economic conditions have accelerated adoption. Sharp depreciation of the naira, elevated inflation and limited access to foreign exchange in 2023 and 2024 increased demand for assets linked to the U.S. dollar. Stablecoins provided both a hedge against currency weakness and a means of paying overseas suppliers.

The trend also gained momentum after the CBN restricted banks from servicing crypto exchanges in February 2021, pushing activity toward peer-to-peer networks and other less-regulated channels, the authors said.

Read also: Africa’s biggest bank eyes acquisitions as it seeks Kenya’s banking crown by 2030

While acknowledging the benefits of faster and cheaper payments, the IMF warned that widespread stablecoin use could complicate economic management.

“One is monetary sovereignty,” Schimmelpfennig and Zhao wrote. “As stablecoins are typically denominated in U.S. dollars, widespread use can resemble a digital form of dollarisation.”

The authors said a growing preference for dollar-linked digital assets could reduce demand for the naira and weaken the effectiveness of domestic monetary policy transmission.

The IMF also highlighted concerns about financial integrity as transactions increasingly move away from traditional banking channels. Activity that previously passed through banks is now flowing through digital wallets and crypto exchanges, making it harder for authorities to monitor transactions using systems designed for conventional financial intermediaries.

“The speed and anonymity of some platforms can also increase risks of illicit finance, including money laundering,” the authors wrote, adding that the risks are not unique to Nigeria but are amplified by the country’s high level of adoption.

Rather than attempting to suppress stablecoin use, the IMF argued for a regulatory approach that accommodates innovation while mitigating risks.

The authors identified four priorities, including preserving monetary stability through a credible domestic currency and sustained macroeconomic reforms. They said recent reforms and tighter monetary policy have helped restore confidence in the naira and that maintaining that progress will be essential.

Read also: IMF warns Nigeria on rising bad loans despite stronger banks

Secondly, the IMF called for stronger regulatory oversight, including clearer rules governing stablecoin issuers and alignment with emerging international frameworks in jurisdictions such as the European Union, Singapore, Hong Kong, Japan and the United States.

Thirdly, the Fund said policymakers need better data on how stablecoins interact with the domestic financial system, and that combining blockchain analytics with reporting on naira-to-stablecoin conversions would improve visibility and help regulators respond more quickly to emerging risks.

Finally, the authors said Nigeria should continue upgrading its payment infrastructure. Although the country has expanded instant domestic payments and joined regional initiatives such as the Pan-African Payment and Settlement System, further improvements to cross-border payment networks could reduce reliance on unregulated alternatives, according to them.

“Stablecoins are neither a passing trend nor a complete substitute for traditional finance,” Schimmelpfennig and Zhao noted. They argued that the digital assets should instead be viewed as a response to persistent inefficiencies in cross-border payments, adding that the policy challenge is to support innovation while ensuring that risks remain contained through sound macroeconomic management and effective regulation.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp