Africa’s biggest economy has been sluggish for several years now, and the human cost of this slowdown is becoming increasingly apparent, BusinessDay’s analysis and expert opinions have shown.

As Nigeria’s independence clocked 63rd, many are checking to see if there is indeed any reason for celebration as the country looks unrecognisable from the country that was forecast in 2015 to be the first African country to hit a GDP of $1 trillion.

For instance, time was when the naira, the country’s currency, was stronger than the United States’ dollar or at least was at par in the 1970s and 1980s, according to a statement from the CBN.

Read also: Nigeria @ 63: Entrepreneur urges govt to arrest inflation, provide infrastructure

Those were the days when Nigerians didn’t need a visa to travel to countries like the UK. Then Nigerian universities were highly regarded globally and the University College Hospital in Ibadan was among the best hospitals in all the Commonwealth nations.

The Nigerian immunisation coverage was also above 80 percent – an indication of an effective healthcare system.

Today, the story is not that inspiring.

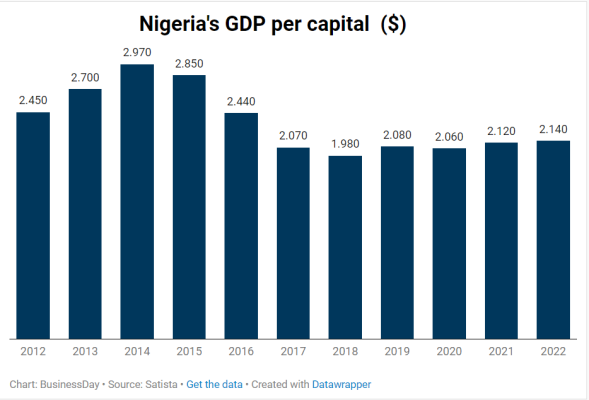

Although the economy has grown from $4.1 billion in 1960 to $477 billion in 2022, the country’s output per person, otherwise known as GDP per capita, has slumped by 28 percent to $2,140 between 2014 and 2022, according to BusinessDay’s calculations.

Take the case of Clement Ighodaro (not real name) for example. His highest qualification is a Bachelor’s degree in Microbiology from Lagos State University.

Ighodaro lost his job at Shoprite in 2021, after the South African retail firm discontinued its 16-year-old operations in Nigeria after struggling with supply chain disruptions and repatriation of funds caused by an acute dollar shortage.

Read also: Nigeria @63: Full speech of President Bola Tinubu on October 1

It has been three years and Ighodaro is yet to land another job. His lack of a job has forced some changes. He has had to move away from his two-bedroom apartment somewhere in Ikorodu to living with a friend in a one-bed apartment almost the size of a telephone booth within the same area.

“It is difficult to earn a living; I’m lucky to start my little business with borrowed funds; I have friends who have been forced to resort to begging or petty trade in order to survive,” Ighodaro said.

Another person who has been directly affected by the economic downturn is Aisha Aliyu, a single mother of three who lives in Lagos.

Aisha used to work as a cleaner, but lost her job a few months ago. She has been unable to find a new job since then, and she is struggling to support her family.

“I don’t know what to do,” she said. “I’m running out of money, and I don’t know how I’m going to feed my children.”

Ighodaro and Aisha’s stories are just two examples of the human cost of Nigeria’s ailing economy.

Yet the pain of an economy growing slower than the population growth also shows it is no respecter of persons. The rich are also feeling the pinch.

Aliko Dangote, the country’s richest man, who doubles as the continent’s wealthiest person, is no longer worth half as much as he was in 2014.

Despite remaining the richest African for almost a decade, his fortune is down by 57 percent to $10.7 billion from $25 billion in 2014, according to Forbes data.

“Despite the objectives of the policies introduced, the Nigerian economy is still faced with suboptimal growth of 3.3 percent and GDP per capita of $2,187, which is 84 percent below the world average of $13,479 as of 2022,” Deloitte, a professional services firm, said in a note.

Read also: 63 years of wandering, wondering, wallowing in excuses

According to Deloitte, challenges such as poor policy implementation, heavy reliance on the oil sector as a major source of revenue, infrastructure deficit, internal security issues and significant debt burden have impeded economic growth and subsequently limited the effectiveness of policies over the years.

With GDP per capita currently at $2,187, the firm said Nigeria is significantly below the prescribed threshold.

“For Nigeria to reach the current world average, its GDP per capita will need to grow at an exponential rate of 25.6 percent per annum within the span of eight years,” Deloitte said.

Experts said a high per capita GDP indicates a high standard of living, while a low one indicates that a country is struggling to supply its inhabitants with everything they need.

“Although the target to double Nigeria’s GDP per capita is ambitious, there are examples of countries that have achieved similar targets within a comparable timeframe,” Deloitte said.

Luxembourg, a small European country surrounded by Belgium, France, and Germany, has the highest GDP per capita globally with $142,214 as of 2023, according to the Worldometer.

Singapore ($127,565) and Ireland ($126, 905) round out the top three countries with the highest countries GDP per capita.

“To bring Nigeria closer to the world average while preventing an overheated economy, the current administration can aim to double the current GDP per capita over the next 8 years,” Deloitte said.

Deloitte advised President Bola Tinubu’s administration to remove the bottlenecks that constrain production and export activities by trade openness through incentives for local production, and reduction of tariffs in certain industries with the potential to generate foreign exchange should be encouraged.

It further advised continued management of the foreign exchange market towards a liberalised regime solely dependent on market forces.

“This will aid cost structuring, promote long-term planning across key sectors, and reduce uncertainties among investors,” Deloitte said.

Concerning Nigeria’s infrastructure deficit, the firm said collaborating with private enterprises through public-private partnerships can bring significant benefits while mobilising private capital and expertise.

“These partnerships can address infrastructure gaps, promote economic growth, and create jobs. This is a strategic approach to bridge the infrastructure gap and drive sustainable development,” Deloitte said.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp