Investors chasing a rally in Nigerian and global equities in the second half of 2026 may also need to consider the commodity market.

Gold, copper, and aluminium are emerging as some of the strongest investment opportunities for the second half of the year as escalating geopolitical tensions, supply disruptions, and structural demand from the global energy transition reshape commodity markets.

CardinalStone Research, in its 2026 Mid-Year Asset Allocation Guide, recommends increasing exposure to commodities and real assets as traditional equity markets grapple with stretched valuations, election risks, and slowing global growth.

While CardinalStone still expects Nigerian equities to deliver a 24.9 percent return in the second half, it argues that industrial and precious metals offer superior portfolio diversification and could generate stronger risk-adjusted returns because their fundamental drivers remain intact despite recent price corrections.

“Given the elevated global uncertainty, we remain positive on alternative assets,” the investment firm said, highlighting aluminium, copper, silver, and gold as preferred exposures for investors.

Commodities quietly become 2026’s best-performing asset class

The first half of the year demonstrated how quickly geopolitical shocks can transform investment markets.

Following the escalation of the US-Israel-Iran conflict, the temporary closure of the Strait of Hormuz triggered one of the largest energy supply disruptions in recent years, sending oil prices above $100 per barrel while disrupting global supplies of liquefied natural gas, fertilisers, and industrial metals.

Rather than fading after the ceasefire, analysts believe those disruptions have fundamentally altered commodity market dynamics.

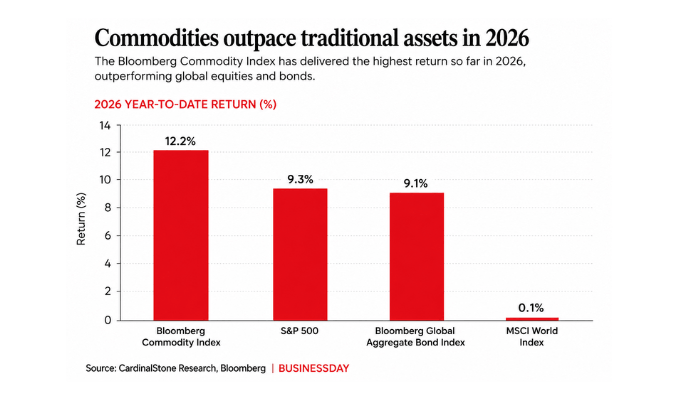

The report noted that the Bloomberg Commodity Index has returned 12.2 percent so far this year, outperforming both the S&P 500 (9.3 percent) and the Bloomberg Global Aggregate Bond Index (9.1 percent), while the MSCI World Index has delivered only 0.1 percent.

The outperformance has been strong enough for the World Bank to revise its 2026 commodity outlook from an expected 7.3 percent decline to a projected 16 percent increase.

Why gold still has room to climb

Gold has experienced one of its most volatile years in recent history.

After surging to a record $5,589 per ounce in January, prices corrected by nearly 19 percent as higher US interest rates, a stronger dollar, and widespread profit-taking outweighed traditional safe-haven demand during the Middle East conflict.

However, analysts believe the correction may mask a much stronger structural story.

The report noted that central banks have maintained gold purchases of roughly 1,000 tonnes annually for three consecutive years, creating a durable demand floor that is unlikely to disappear.

The World Bank has consequently lifted its 2026 average gold price forecast by 31.5 percent to $4,700 per ounce, reflecting expectations that official-sector buying, together with retail accumulation through bars and coins, will continue supporting prices.

For investors, that means the recent pullback may represent an entry opportunity rather than the end of the rally.

Copper stands to benefit from global electrification

Copper’s outlook is increasingly being driven less by geopolitics and more by structural supply shortages.

Although Middle East tensions initially pushed prices lower amid fears of weaker industrial demand, production setbacks elsewhere have tightened the global market.

Chile, the world’s largest producer, recorded its weakest quarterly copper output in nine years after ore quality deteriorated, while proposed US tariffs on refined copper imports from 2027 are expected to encourage heavy stockpiling during the second half of 2026.

CardinalStone believes manufacturers and commodity traders are likely to accelerate purchases ahead of those tariffs, providing additional support for prices.

Copper also remains central to electric vehicles, renewable power, battery storage and transmission infrastructure, sectors expected to experience sustained investment over the coming decade.

Aluminium’s supply crisis deepens

Among industrial metals, the report identifies aluminium as perhaps the strongest structural commodity.

Unlike copper, where the Middle East accounts for only a small portion of global production, Gulf countries represent between 8 and 9 percent of global aluminium smelting capacity.

Military strikes on major smelters disrupted more than 1.5 million tonnes of annual production, briefly sending London Metal Exchange aluminium prices to $3,850 per tonne before easing as geopolitical fears moderated.

Yet the investment case remains compelling. China, the world’s largest producer, cannot substantially increase output because of government-imposed production caps aimed at controlling energy consumption.

At the same time, demand continues to rise from electric vehicles, solar panels, wind turbines, packaging, and electricity transmission projects.

Research cited by CardinalStone projects a 1.4 million-tonne global aluminium deficit in 2026, with prices potentially climbing to a record $4,000 per tonne during the third quarter.

Why investors should diversify beyond equities

CardinalStone’s recommendation reflects a broader shift in global portfolio construction.

Rather than relying solely on equities, the research firm argues investors should increase allocations to alternative assets that protect against inflation, geopolitical uncertainty, and currency volatility.

Its preferred commodity basket includes gold, silver, copper, and aluminium alongside infrastructure and real estate investments, assets expected to deliver stable long-term returns even if financial markets become more volatile ahead of major elections and shifting global monetary policies.

For Nigerian investors, while domestic equities remain attractive because of improving macroeconomic conditions, stronger corporate earnings, and foreign portfolio inflows, commodities now offer an additional source of returns that is increasingly disconnected from traditional stock market cycles.

As Iran and the US have threatened to reignite their conflict after the most extensive exchange of fire since an interim deal was signed last month, energy transition investments continue, and supply constraints remain unresolved, metals may prove to be the winners of the second half of 2026.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp