House of Lannister, according to G.R.R Martins bestseller novel book “The Game of Thrones” is about a very wealthy and influential family that does not want to be indebted to anyone.

This is because there is certainly power, respect and independence with being in no one’s debt.

That stellar track record helped the Lannisters including patriarch Tywin, Queen Cersei and Sir Jamie become one of the wealthiest families in the Seven Kingdoms.

Even when they owe, they look their creditors in the face and say “A Lannister always pays his debts.”

While the Lanisters have their castle built on goldmines which gives them the leeway to meet their obligations, Nigeria’s largest cement makers (who are able to deploy their fixed assets in generating higher sales), are recording mixed reactions towards debt obligations.

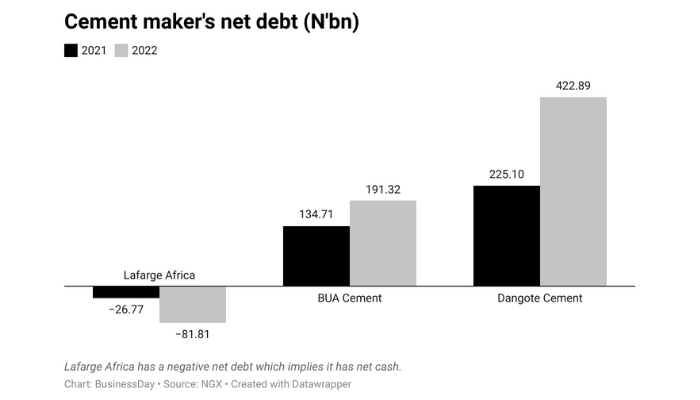

Findings by BusinessDay analysis showed BUA Cement and Dangote Cement’s net debts grew by 70 percent to N614.21 billion in 2022.

Net debt is a liquidity metric used to determine how well a company can pay all of its debts if they were due immediately. It shows how much cash would remain if all debts were paid off and if a company has enough liquidity to meet its debt obligations.

Lafarge Africa recorded a negative net debt of N81.8 billion, which implies that the company possesses more cash and cash equivalents than its financial obligations and is hence more financially stable.

Further findings showed the three-cement maker’s total borrowings stood at N868.76 billion in 2022, up 29.3 percent from N671.73 billion in the full year of 2021.

The firms recorded total short-term borrowings of N489 billion while long-term borrowings amounted to N379.77 billion in December 2022.

According to market analysts, cement makers are raising debts such as commercial papers or bonds for working capital purposes or quick investment needs.

“Cement maker’s ability to pay back their loans are never in doubt, but rising input costs arising from higher energy costs prevented the top line growth from translating into double-digit bottom-line growth,” Tunde Adelakun, an analyst at Sofidam Capital Limited, said.

He added, “if it is judged that income is not large enough to pay monthly instalments, they may be encouraged to take a longer tenor.”

Findings by BusinessDay showed Dangote Cement is a familiar face in Nigeria’s capital market for new debt through bonds after its board agreed to the move, aimed at financing its operations and some expansion projects.

Last February, Dangote Cement issued N50 billion commercial paper sales; the firm issued the debt instruments in two maturities, with the Series 4 at a 183-day tenor and the Series 5 at a 267-day tenor.

Last year, the company said it completed the issuance of N116 billion series 2 fixed rate senior unsecured bonds under its N300 billion multi-instrument issuance programme.

In June 2021, the cement producer had successfully issued N50 billion series 1 fixed rate senior unsecured bonds.

“Cement makers will remain unwavering despite a projected increase in the proportion of debt in their capital structure,” Charles Ogbeide, an industry analyst with a Lagos-based investment bank said.

He added, “Cement makers are investing in various projects across the continent while setting up plants in Nigeria in pursuant of the government’s backward integration programme”.

Read also: Trading revenue swings Stanbic’s gross earning to decade high

Firm analysis

Lafarge

Lafarge recorded negative net debt which implies it has net cash of N81.81 billion in 2022, 205.6 percent increase from N26.77 billion in 2021.

The firm’s short-term borrowings grew 68.5 percent to N35.06 billion in 2022 from N20.81 billion 2021 while long term borrowings dropped 38.3 percent to N1.53 billion from N2.48 billion in the period reviewed.

This led to total borrowings amounting to N36.59 billion in 2022, 57 percent from N23.29 billion in 2021. Lafarge’s interest on borrowings dipped 79.6 percent to N766.86 million in December 2022 from N3.76 billion in December 2021.

Lafarge’s repayment of loans and borrowings stood at N18.7 billion in 2022, 48 percent decrease from N36.05 billion in 2021.

With profit after tax which amounted to N53.6 billion, up 5 percent from N51 billion in the period reviewed. Lafarge Africa reported a 27.3 percent year on year increase in revenue to N373.25 billion from N293.09 billion in full year 2021.

“We note that the company, like its peers, was able to take advantage of elevated prices. Going into 2023, we believe the company is positioned for growth as it ramps up output on the back of the debottlenecking exercise strategy,” analysts at Coronation Research said.

The company’s cash and cash equivalents at the end of the year stood at N116.76 billion, 140 percent increase from N48.63 billion on the back of net cash flows generated from operating activities which amounted to N100.7 billion during the period.

BUA Cement

BUA Cement net debt surged 42 percent to N191.32 billion in 2022 from N134.71 billion in 2021.

The firm’s short-term borrowings rose to N80.70 billion in 2022, 102.7 percent from N39.81 billion in 2021 while long term borrowings at N44.74 billion, up 2.4 percent from N43.69 billion in the reviewed period.

Total bank borrowings grew 50.2 percent to N125.44 billion in 2022 from N83.5 billion in 2021. Interest expense on borrowings stood at N6.74 billion, 3.3 percent decline from N6.97 billion in the comparable period.

Principal repayment of borrowings amounted to N136.98 billion in 2022, 33 percent increase from N102.94 billion in 2021.

BUA Cement’s profit after tax grew to N101 billion in 2022, 12 percent increase from N90 billion in 2021. The firm recorded 40 percent year-on-year increase in revenue to N360.9 billion in 2022, from N257.3 billion in the previous year.

According to Coronation Research, BUA Cement’s revenue performance in full-year 2022 was in line with its expectations (+0.75% variance).

“Amongst its peers in the industry, we are pleased with its improved capacity utilisation (57.3%) reflecting in decent volume growth while also taking advantage of the elevated pricing environment,” Coronation Research said.

Cash and cash equivalents dropped 23 percent to N48.05 billion in 2022 from N62.34 billion on the back of negative cash flow used in investing and financing activities.

Dangote Cement

Dangote Cement net debt grew to N422.89 billion in 2022, 87.9 percent increase from N225.10 billion in 2021.

The firm’s short-term borrowings dropped 4 percent to N373.24 billion in 2022 from N388.38 billion in 2021. Long-term borrowings, however, increased by 89 percent to N333.50 billion from N176.56 billion in the comparable period.

Dangote Cement’s total borrowings climbed 21 percent to N706.73 billion in 2022 from N564.94 billion in 2021 while interest on borrowings grew 31.6 percent to N75.24 billion from N57.17 billion in the period reviewed.

Loans repaid stood at N267.18 billion in 2022, 17.7 percent increase from N324.83 billion in 2021.

Profit after tax stood at N382.3 billion in 2022, 5 percent increase from N364.4 billion in 2021. The firm’s revenue grew 17 percent to N1.62 trillion in 2022 from N1.38 trillion in 2021.

According to CSL Research, the management is yet to provide details of the drivers of the company’s strong performance in FY 2022, but we believe this growth in revenue could be attributed to increasing prices, amidst a decline in production volumes as the company seeks to protect its profit margin. As of 9M 2022, prices were up by (+28.1% y/y), while production volumes declined by (-4.7% y/y).

Cash and cash equivalents dropped 43 percent to N150.84 billion in 2022 from N263.4 billion in 2021, on the back of 35 percent dip in net cash flow from operating activities and negative cash flow used in investing and financing activities.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp