Introduction

Top line growth for some businesses has been negatively impacted. A knee jerk reaction from employers may be to lay off employees or renegotiate vendor contracts to reduce costs. The most plausible move will depend on several factors such as the long-term growth plans and business continuity during and beyond the pandemic. Employers who can navigate these times through proactive and innovative thinking will be ahead of the curve and may very well come out at the end of the tunnel with the greatest asset; an agile workforce.

Nigeria recorded its index case of the pandemic on 27 February 2020 and deployed various strategies to contain the spread-these included issuing lockdown orders and closing the borders. Some businesses have struggled with

the seemingly new model of remote working.

Top line growth has been negatively impacted, with some sectors (such as the hospitality and airline industries) badly hit. A knee jerk reaction from employers may be to lay-off employees or renegotiate vendor contracts to reduce costs.

The most plausible move will depend on several factors such as the long-term growth plans and business continuity during and beyond the pandemic. Employers who can navigate these times through proactive and innovative thinking will be ahead of the curve and may very well come out at the end of the tunnel with the greatest asset; an agile workforce.

This article focuses on considerations for managing employee costs. It also considers the legal and tax implications of changing your workforce and key considerations for the ‘new workplace’ as the lockdown eases.

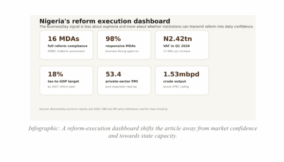

Read also: Africas free trade pact can boost regional income by $450bn, says World Bank

Re-assess your long-term strategy

With lower productivity levels, it is a good time to reassess the growth strategy of the company. There may be need to revisit the ‘core/live wire’ of the business, diversify to new income streams, improve efficiencies on existing business lines or even carve out distressed or non-core assets. What happens to the workforce associated with such assets? How do you keep staff motivated in the absence of physical interface? Does your reward and compensation structure align with a work from home (WFH) policy?

Does your performance strategy adequately appraise staff working from home?

Are your flexi policies sufficient to attract and retain the right talent? The answers to these questions will not come easy especially for family businesses where loyalty is a key factor for retaining employees. Broadly,employers would need to:

a)assess current and future business needs

b)identify skill gaps and mismatches

c)build a future proof skill strategy. This will include re-evaluating the reward and performance strategies

d) develop and implement reskilling/upskilling of workforce

e) evaluate return on investment.

Review existing relationships

One key consideration in the assessment will be reviewing contractual obligations on existing relationships. Some relationships have the semblance of an employer/employee relationship but are not. Employers must review relationships to determine whether a ‘staff’ is an employee, or an independent contractor before embarking on varying arrangements.

The costs of engaging a contractor differ from the employee so this will be critical in determining whether to continue, end or convert.

For example, an independent contractor is only entitled to the agreed contract fee/payment; as opposed to the employer/employee relationship where an employee may be entitled to other payments (statutory contributions) in addition to his/her wages/salaries.

For the purpose of reviewing an employment relationship, the primary legislation and documents to review would include the Labour Act, the employee’s contract (usually this would incorporate the Employment Handbook which contains additional terms of the employment contract) and any Collective Agreement (relevant in a unionised workplace).

To Continue or to End?

For as long as an employment contract subsists, the employer will be under an obligation to fulfill its statutory and contractual obligations. Employers seeking to stay afloat, would need to be innovative to reduce employment related disputes. The parties can agree to vary the terms of the contract (variation could include pay cuts, furlough leave and flexible working); suspend the employment contract or outrightly terminate the contract.

Outsourcing

Remote working comes with a huge element of trust that the employee is working as agreed contractually. The employer must believe things are working as expected but can put processes in place to measure deliverables and results. A 2019 survey from job search site FlexJobs found that 80 percent of respondents said they would be more loyal to their employers if they had flexible work options (up from 75 percent in 2018).65 percent of respondents also think they would be more productive working from home (WFH) than working in a traditional office environment due, in large part, to fewer distractions. Where an employer still feels otherwise about WFH, one option may be to convert employee relationships to contractor relationships or outsource services to an independent third party provider. An employer taking this route should consider issues such as confidentiality, ownership of intellectual property, quality control and how to enforce these. The tax implications also differ.

Rather than withholding Pay As You Earn (PAYE) taxes at an average of about 20%, withholding tax at 5% to 10% will apply on the fees charged by the independent contractor. VAT will be an added cost especially with the changes under the Finance Act 2019 to self charge. The corollary is that social security costs may no longer apply where a conversion is done but an initial charge on termination benefits may apply to deserving employees who now become consultants to the companies.

Paid and unpaid Leave

Where employees need to work from a physical office, the employer can manage the size of the workforce by requesting employees whose services are not required in the short term to utilise their statutory holidays or go on unpaid leave where leave is exhausted.

An employer is not discharged from its obligations to pay salaries and account for PAYE taxes or social security contributions because an employee is on leave. With unpaid leave, some of these obligations do not arise but documentation is key to forestall any challenge from the regulators.

Variation of contracts

Contractual obligations can be varied or waived by mutual agreement between employer and employee. For example working less hours to align with demand and varying allowances as a result. An employee who works remotely may no longer require a travel allowance but may need internet services to be effective.

Employment contracts can be varied orally, but it is prudent to document them. Where an employment relationship is governed by the Labour Act, any variation must be brought to the notice of the employee within one month. With a variation, contractual and social security concerns may change e.g. standard pay components underlying pension contributions.

Suspension of Employment Contract

The Courts have defined suspension as “the act of temporarily delaying, interrupting, or terminating something, such as suspension of business operation. It could also mean the temporary withdrawal from employment, as distinguished from permanent severance”.

Where the employee will resume duties later, the suspended contract should be clearly documented so it does not become acrimonious. If an employer wishes to make routine ‘gracious’ payments as a palliative for the crisis, the payments may be regarded as gifts or benefits in kind. There is a thin line of distinction that would be outweighed in the light of documentation. Benefits are subject to tax under the Personal Income Tax Act (PITA) while gifts are not. It would be useful for employers to seek clarification before embarking on such payments.

Termination

Where termination is the best option, the employer must ensure it does not end up in lawsuits. Termination must be done in accordance with the terms and conditions of the employment or any relevant collective agreement that has been incorporated in the employment contract. In an employment with statutory flavour where the procedure for termination is expressly spelt out in the relevant statute, the employer must comply strictly with the provisions of the statute. Any termination that is inconsistent with the statute is null and void.

An employer is allowed to terminate without giving reasons but it is prudent for the employer to consider the defences that may be available if the termination is contested. It is uncertain whether the defence of force majeure or frustration will be sustained by the Courts to discharge the employer from damages. What is certain is that the Courts must take judicial notice (facts which a court mandatorily takes as proved by the operation of law and not requiring further proof) of the crisis and evaluate its impact on an employment relationship on a case by case basis.

Generally, redundancy payments are made up of elements of terminal pay and/or termination benefits. A termination pay/benefit is a redundancy lump sum paid to employees on the premature termination of employment (usually discretionary) while terminal pay/benefits are retirement /resignation/end of employment payments usually based on predefined terms and satisfactory performance of employment duties.

Termination benefits (usually capital in nature) will qualify for tax exemption under PITA, to the extent that the amount paid to the employee is not ‘pre-agreed’. These payments will however, be liable to Capital Gains Tax (CGT) at 10% subject to qualifying exempt limits. Terminal benefits on the other hand are subject to Personal Income Tax. Consideration must also be given to pension benefits that can be accessed when an employee is disengaged and whether these are taxable.

How high has the bar been set for safety at work?

One of the duties of the employer is to ensure safety at work. Some of the questions that have arisen are: (i) whether the employee’s home can be designated a ‘workplace’ for the purpose of imputing liability for work related hazards. (ii) can an employer make claims under the Employee Compensation Scheme for remote workers or even pandemic related matters? (iii) or should the employer cease contributions where it adopts a WFH policy? As the lockdown eases, employees may need to return to the workplace.

How much safety can an employer put in place to ensure that transmission of the virus is limited to the barest minimum? What would be the test for determining whether the employer has sufficiently discharged the duty to provide a safe workplace? These questions may not have a straightforward answer. What is sure is that employers must adhere to all the directives issued by the government.

It would be prudent to document health and safety measures that have been put in place as a response to the pandemic.

Are the costs associated with running a home office deductible?

Section 20 of PITA spells out the test for determining deductibility of expenses incurred to generate taxable income under the Act. For an expense to be deductible, it must have been incurred wholly, exclusively, necessarily and reasonably for the purpose of earning relevant income (in this case salary/wage).

Can costs incurred while working from home be deducted for tax or are these private expenses which are not allowed? Employees would do well to keep separate and robust documentation of the expenses associated with running their home offices. For evidential proof, an employee who can show the hike in expenses (for example electricity bills, cost of running the generator and providing internet service) is more likely to succeed than one without documents.

Business continuity

How detailed is your business continuity plan? Does it capture working from home procedures, cyber security, alternative working location, document storage etc. If, for example a team member gets infected, the chances are that all the other team members who came in contact may be quarantined. If an office building becomes compromised and inaccessible to the workforce, it may also become impossible for the organisation to conduct its business. These and many more would pose a big challenge to business continuity.To ensure minimal disruption on account of the pandemic, organisations must review and update their business continuity plans to include workforce planning /arrangement, policies for employees working remotely, employee communication, leave management etc.

How detailed is your business continuity plan? Does it capture working from home procedures, cyber security, alternative working location, document storage etc. If, for example a team member gets infected, the chances are that all the other team members who came in contact may be quarantined. If an office building becomes compromised and inaccessible to the workforce, it may also become impossible for the organisation to conduct its business. These and many more would pose a big challenge to business continuity.

To ensure minimal disruption on account of the pandemic, organisations must review and update their business continuity plans to include workforce planning /arrangement, policies for employees working remotely, employee communication, leave management etc.

Conclusion

This crisis has affected individuals and businesses in ways that were not anticipated. While some businesses would not survive the crisis, those who survive must reassess their business models, performance strategy and compensation structure. Businesses would have to review their workforce to eliminate waste-routine tasks that need to be automated. This is not to say, people will not be required but the skillset required to take businesses to the next level in the new world will be different. All these actions have legal and tax implications for the workforce, employer and other stakeholders.

Above all, organisations will do right to strategise for an agile workforce amidst the uncertain business environment.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp