In 2008, Enhancing Financial Inclusion and Access (EFInA) conducted a survey that revealed that 52.5% of the adult population in Nigeria were excluded from financial services. It called attention to the level of financial exclusion in the country. The Global Financial inclusion index was later developed in 2011 to track global efforts towards financial inclusion. Following the wind, the CBN developed a National Financial Inclusion Strategy (NFIS) in 2012 with the ambitious goals of achieving 80% total financial inclusion and 70% formal financial inclusion by 2020.

The NFIS specifically aims to increase by 2020, the number of adults with access to payment services to 70% (from 21.6% in 2010), access to savings accounts to increase from 24.0% to 60%, and credit from 2 to 40%, Insurance from 1 to 40% and pensions from 5 to 40%, all within the same period. The targets were benchmarked around peer countries as well as other growth factors in the domestic environment. Nigeria is not on track to meet the 2020 targets; which is less than 2 years away.

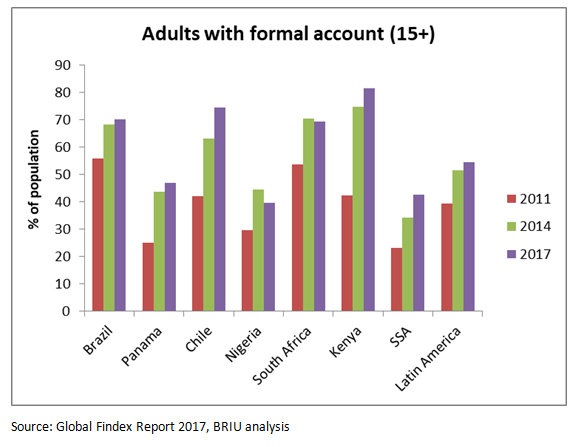

The Global Findex report 2017 show that with an estimate of 100 million unbanked adults, Nigeria joins six other countries including Bangladesh, China, and India as the top contributors to the global financially excluded of 1.7 billion. The number of adults with a formal bank account fell from 44% to 39.7% between 2014 and 2017. The number of adults with financial institution account fell to 39.4% from 44%, with a gender disparity of 51% and 27% for male and female respectively. The percentage of adults who saved money in a financial institution and those who borrowed with a credit card were 20.6% and 5.3% respectively. The number of those with mobile money account is still incredibly low at 5.6%, below the Sub-Saharan African average of 20.9%. According to EFInA, the total financially excluded is as high as 41.6% in 2016. It is therefore pertinent to draw lessons from successful countries with similar conditions in Latin America

Source: Global Findex Report 2017, BRIU analysis

Latin American Countries such as Brazil, Panama, and Peru have made significant and consistent improvements in financial inclusion through the years from 2011 to 2017. In the period, Peru recorded an astronomic rise in the number of adults with accounts, from 20.5% (2011) to 42.6% (2017); whereas Panama recorded 24.9% and 46.5% in the same period. In the lead on adults with accounts in financial institutions, Chile (73.8%) and Brazil (70%) surpassed the Latin American average (54.4%) in 2017. For both countries, the gender and educational disparity in accounts-ownership show impressive records. The percentage of adults saving at a financial institution in Brazil and Chile was 14.5% and 21.1% above the regional average of 12.2%; and on access to credit via credit card in the last year, both countries recorded 26.3% and 30.9% – against a regional average of 20.8%.

In Brazil, the progress has been attributed to the expansion of the national correspondent banking networks, growth in microfinance and cooperatives as well as targeted conditional transfers to increase the income levels of the low-income workers under the Bolsa Família program. The correspondent banking model permits accessible retailers such as food vendors, gas stations and drug stores to act as intermediaries for basic financial transactions, thereby bridging the gap between formal and informal financial structures. The Brazilian government also promoted financial literacy and adapted regulation of financial services to the needs of the underserved low-income groups. In Chile, it was a sincere commitment to the Maya Declaration in 2011 – to which Nigeria is a signatory. The Chilean government introduced an electronic payment system for transfers of state benefits, launched an extensive financial education program for beneficiaries of state transfers and developed a complementary financial inclusion survey. A state bank, Banco Estado, was established with a defined financial inclusion strategy to drive efforts on achieving financial inclusion.

All that notwithstanding, some progress have been made by both policymakers and stakeholders to improve access to financial services in Nigeria. The Brazilian correspondent banking is similar to the Agent banking in its early stages in urban centres across the country; while the Bolsa Família is to the National Social Investment program (NSIP). More so, The CBN and the Nigerian Communications Commission (NCC) signed a memorandum of understanding in other to facilitate mobile money operations on the premise that more adults in Nigeria owned phones than bank accounts. This initiative has given birth to a synergy between commercial banks and telecoms operators as well as enabling the development of financial technology (FinTech) operators such as Paga, Quickteller, Paydirect, Alert and eTransact. The collaborative effort between the CBN and the NIBSS to create a regulatory sandbox which allows FinTech start-ups to test solutions under controlled environment has enabled a start-hub conducive for creating sustainable businesses and expansion of the FinTech space to reach the last mile. The agent banking model that incorporates trading businesses as transactional outlets of banks and the most recent Payment Service Banks which is a model of the Non-Bank led financial inclusion strategy is also the efforts to serve the unbanked.

The direction of policy strategies seems to be towards leveraging ownership of mobile phones and access to the internet which happens to be the strongest improvement area for African countries according to the Global Findex report, 2017. Therefore, a combination of policies that encourage participation within the mobile money space and an expansion of the agent banking model into other states of the federation would go a long away, noting that most of these models are still being piloted in urban centres where the incidence of financial exclusion is less critical. The electronic payment method should be deployed in the conditional cash transfer schemes of the NSIP which is still done in cash at some local levels. Effective financial education for the most vulnerable cannot be overemphasized. Since the drive on financial inclusion in 2008, only about 10% declined has been achieved, amounting to 1% per annum on average. There is still a long way to go; all hands must be on deck.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp