…Weaker naira puts banks’ loan books at risk

The debts owed by oil and gas firms to Nigerian commercial banks jumped by over 40 percent largely due to the recent weakening of the naira, now representing over a quarter of the lenders’ total credit to the economy.

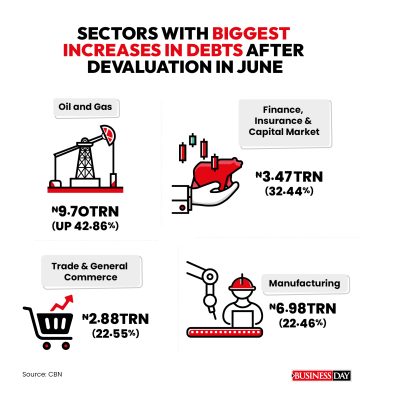

Data from the Central Bank of Nigeria (CBN) indicate that oil and gas firms have the most foreign currency (FC)-denominated debts, and their naira equivalents surged on the back of the large devaluation in June, when the naira closed at 751.98 per dollar on the official market as against 465.46/$ at the start of that month.

Their debts ballooned to N9.7 trillion in June from N6.79 trillion in the previous month, accounting for 25.88 percent of the banks’ total credit, which grew to N37.48 trillion from N30.18 trillion, according to the data.

Firms operating in the downstream, natural gas and crude oil refining subsectors owed N7.03 trillion as of June as against N4.85 trillion in May, while those in the upstream and services subsectors owed N2.67 trillion, up from N1.94 trillion.

Operators in finance, insurance and capital markets saw the second biggest increase as their debts rose by 32.44 percent to N3.47 trillion, while those in trade and general commerce owed N2.88 trillion, up 22.55 percent.

Manufacturers owed N6.98 trillion as of June, up 22.46 percent compared to the previous month.

The spike in debts poses risks to banks’ loan books but analysts believe that the sector looks relatively well placed to weather this devaluation storm. Many of the lenders reaped bumper profits in the first half of the year partly due to foreign exchange revaluation, even as the capital adequacy ratio (CAR) of the sector declined in June.

“While banks’ receive a positive valuation effect from the naira devaluation, their loan books might suffer. Around 30 percent of total banking sector loans have been made in foreign currency,” David Omojomolo, Africa economist at London-based Capital Economics, said.

“For borrowers whose income is in naira, servicing these debts will become more expensive. That said, while data are hard to come by, loans to the oil and gas sector – whose income is in dollars – probably account for a large share of total foreign currency lending,” he said.

He said the risks to the loan book could be made worse by the broader environment of weak growth, high inflation and interest rates.

The country’s economic growth stood at 2.51 percent in the second quarter, inflation surged to a fresh 18-year high of 26.72 percent in September and the money policy rate – the benchmark interest rate – was raised in July to 18.75 percent, the highest in more than two decades.

“These will make servicing naira loans harder too. The experience from 2015-17, when the collapse in global oil prices brought some similar economic challenges, showed that NPLs (non-performing loans) also increased, peaking at close to 15 percent,” Omojomolo added.

Banks’ NPL ratio declined further to 4.1 percent in June from 4.5 percent in prior month, remaining below the maximum prudential requirement of 5.0 percent, according to the CBN.

The continued decline in NPL has been attributed to write-offs, restructuring of facilities, Global Standing Instruction (GSI) and sound credit risk management.

The GSI, a policy introduced by the central bank in 2020, is a mandate authorising the recovery of due loan obligations from any and all deposit accounts maintained by a defaulting borrower with other banks other than the creditor bank.

“It is worrisome indeed that the expected multiplier effect of the increase in total credit on output has not crystallised, suggesting that credit may have ended up in the foreign exchange market, which may erode asset quality, in the medium to long term,” Ahmed Aliyu, a member of the Monetary Policy Committee, said in his personal statement at their last meeting.

A global credit rating agency, Fitch Ratings, said in July that naira devaluation would inflate banks’ FC-denominated risk-weighted assets (RWAs), putting pressure on capital ratios.

“It will also inflate FC-denominated problem loans, thereby increasing the prudential provisions that banks must hold against them. The impact is mitigated by banks’ generally small FC-denominated RWAs and net long FC positions, which deliver FX revaluation gains,” it said.

It said the devaluation, along with the fuel subsidy removal, would also lead to higher near-term inflation and tighter monetary policy, putting pressure on borrowers’ debt-servicing capacity and causing impaired loans to rise quicker than was previously envisaged.

Read also: Explainer: What CBN amendment bills propose

“Nigerian banks appear sufficiently capitalised and able to absorb even greater loan losses. The capital adequacy ratio has declined from around 14 percent at the end of 2022 to around 11 percent at the end of June. This is still above the CBN’s 10 percent minimum requirement for domestic banks,” Omojomolo said.

He said it would take a loan loss rate of over 7 percent to take the CAR down to the minimum of 10 percent. “That seems very high. In the US, the loan loss rate hit 5 percent during the Global Financial Crisis.”

Analysts at CSL Stockbrokers said bank FX loans to customers with naira earnings could deteriorate owing to the devaluation as they have to service their loans at a significantly higher cost and this could lead to growth in impairments.

“If a bank suffers an unexpected rise in cost of risk that exceeds the capacity of one year’s profits to absorb it, then that bank will be looking at writing down capital. However, banks within our coverage are unlikely to require a capital write down,” they said in a recent note.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp