When the name “UAC of Nigeria Plc ( UACN)” is mentioned, what easily comes to mind is the company’s portfolio of well-known brands such as Gala Sausage Roll, a pastry snack which gained wide acceptance of road travellers in Nigeria; Mr Bigg’s, one of Nigeria’s leading Quick Service Restaurants (QSR) brands; Supreme Ice Cream; among others.

From food and beverage to paint, logistics and real estate sectors of the economy, Nigeria’s oldest and one of the largest diversified conglomerates UACN, which was formerly a part of Unilever Plc., has played an active role in Nigeria’s economic landscape since 1879 and maintained a track record of consistency over the years.

UACN is a listed conglomerate on the Nigerian Stock Exchange (NSE) and parent of a number of companies including UAC Property Development Company PLC (UPDC), the first company in the real estate sector to be listed on the NSE; and UAC Foods Limited, manufacturers of Gala Sausage Roll, Supreme Ice Cream and Swan Natural Spring Water.

The company’s other business portfolio includes MDS Logistics Limited, a foremost integrated logistics company with investments in pharmaceutical distribution hubs in key locations across the country; UAC Restaurants Limited with its chain of Mr. Bigg’s and Debonairs Pizza outlets.

In addition to these are Grand Cereals Limited, manufacturers of Vital Poultry and Fish Feeds, Binggo Dog Food, Grand Maize Flour, Grand Cornflakes and Grand Soya Oil; Chemical and Allied Products Plc, leading its industry segment with Dulux Paint; and UNICO CPFA Limited, a Closed Pension Fund Administrator.

While UPDC engaged in a broad range of activities including property development for sale and lease, facilities management, and hospitality for corporations and high net worth individuals, its recent expansion coincided with Nigeria’s economic recession in 2016. The real estate sector was particularly affected with significant declines in asset values and rental rates.

Although Nigeria emerged from the recession in the second quarter of 2017, the real estate sector continued to shrink, further contracting by 3.84 percent in the second quarter of 2019.

The resultant effect of this is declining investment values, reduced demand for assets, and high vacancy rates. Little wonder revenue from real estate continued to underperform in 2018, contributing just 2.7 percent to the group’s revenue compared with 3.8 percent recorded in 2017. Real estate revenue also nosedived by 43 percent to N2.2 billion in 2018, from N3.9 billion in 2017.

“On the back of lower housing inventory sales and collections amid challenging market conditions, we estimate that average occupancy rate has fallen to 45-47 percent, from 55-60 percent pre2014 oil price slump,” analysts at CSL Stockbrokers Ltd stated in a note to clients.

In addition to that, UPDC recorded an impairment loss of N8.91 billion, making UACN record a negative EBITDA margin, an assessment of a firm’s operating profitability as a percentage of its total revenue, of 3.9 percent in full-year 2018 and an after-tax loss of N9.58 billion from a profit of N962 million a year earlier.

With UACN’S loss of N15 billion in 2018, worse than a loss of N2.9 billion recorded in the previous year, it became apparent that the UPDC business segment was no longer profitable for the parent company.

Analysts had expressed concerns over the effect of UACN’S conglomerate model and the need to get out of its non-profitable lines. In March, the company appointed a seasoned professional with 17 years’ experience gained from diverse functional roles, covering finance, strategy, risk management, and corporate finance, Ibikunle Oriola, as its new group finance director, while Folasope Aiyesimoju resumed as managing director/ceo later in the month.

Restructuring and Recapitalization of UPDC

Present state forestall the unimpressive performance, the board and management of UACN last week announced plans to restructure and recapitalize UPDC, a move the company said is subject to the approval of the shareholders of both firms, the NSE, and the Securities and Exchange Commission (SEC).

For UPDC, the challenges are endless ranging from revenue shortfalls to a continuous increase in the debt burden. Besides these, it drowned in a pool of losses since 2016. The underperformance weighed on the company’s equity value and caused its shareholders’ funds to come under within the last five years, falling steadily to N16.7 billion as at the first half of 2019. This also restricted the company’s ability to pay dividends.

Worried by all these ill-fated events and in a bid to reposition UPDC, the management of UACN said it aims to reduce finance costs and achieve a sustainable capital structure for UPDC, through the introduction of equity capital to refinance outstanding debt obligations and reduce the uncertainties associated with frequent debt roll-overs.

The recapitalization of UPDC would involve an equity capital raise of N15.96 billion by way of a rights issue to repay the company’s short-term debt obligations which stood at N22.84 billion at the end of June 2019 and strengthen its balance sheet.

A rights issue is a form of raising capital where cash-strapped companies grant existing shareholders right to buy new shares often at a discount – lower price – to the current market price. The right does not translate to obligation, implying shareholders are not bound to buy the new shares.

Post the rights issue, UPDC’S only interest-bearing debt will be its long-term bond with a total outstanding balance of N4.3 billion. The reduction of UPDC’S outstanding debt through the injection of N15.96 billion from the rights offering is expected to help the firm attain sustainability and ensure its debt is serviceable from recurring cash flows.

After the recapitalization of UPDC, the company will also unbundle its majority interest of 61.5 percent in the UPDC Real Estate Investment Trust (UPDC REIT) to UPDC shareholders through the allocation of REIT units directly to UPDC shareholders in proportion to their post rights issue holdings in UPDC. This will be in addition to their shares in UPDC.

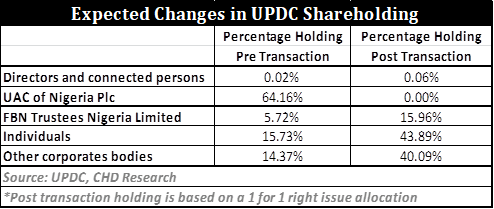

Unlike UPDC which was enmeshed in losses since 2016, UPDC REIT is profitable and has a track record of consistent dividend payments. Subsequently, UACN will unbundle its 64.16 percent shareholding interest in UPDC on successful capital raise and transfer on a pro-rata basis – a Latin term used for describing allocation based on each person’s share of the whole – to all its shareholders, who will hold such UPDC shares in addition to their existing shares in UACN.

Hence, the unbundling of these companies will break the connecting chains and create three separate entities post transaction such that UACN will no longer hold any equity stake in UPDC, implying UPDC will cease to be a subsidiary of UACN and be consolidated in UACN’S financial statements.

Also, UPDC will no longer own any units in the UPDC REIT, indicating the firm will cease to be an associate company of UPDC. As a result, UPDC will now operate as a standalone legal entity, free to source appropriately structured capital.

After the recapitalization and restructuring, each UACN shareholder will hold shares in three separate entities – UACN, UPDC and the UPDC REIT benefitting from the prospects of each.

“Efforts are underway to strengthen UPDC’S board of directors and management team to ensure that the recapitalized and restructured UPDC retains its leadership position in the Nigerian Real Estate Sector,” both firms said in a statement. “Operations, contracts and legal obligations of both UAC and UPDC will continue as normal and in line with the existing Memorandum of Articles and Association of the respective companies.”

Going forward, the management of UACN will now focus more on the rest of the company’s subsidiaries which include UAC Foods Limited, Grand Cereals and Oil Mills, Livestock Feeds Plc, MDS Logistics, Chemical and Allied Products Plc, Portland Paints Plc, amongst others.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp