Nigeria drug makers are upgrading facilities in hopes of meeting the World Health Organisation’s (WHO) pre-qualification standards that will make their products marketable at the international level and help boost revenues and margins.

Meeting the pre-qualification standards has become a major environment challenge as some of these manufactures are incurring huge operating and finance to upgrade and construct new facilities.

Our discussion is centred on the overall performance of the five drug makers that have so far released their full year 2013, financial results.

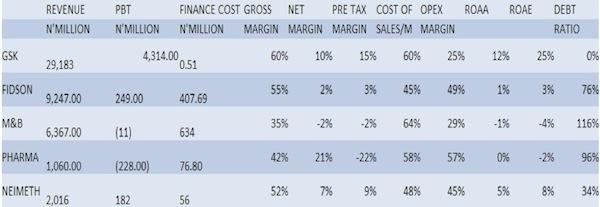

GlaxoSmithKline (GSK), the largest pharmaceutical company in Nigeria by market value, was able to grow its revenues at year end 2013, due to product rebrand, introduction of innovative products and aggressive market penetration.

This explains its higher gross, net margins and pre-tax margins of 60 percent, 10 percent and 15 percent, respectively. It also returned an impressive return on shareholders assets, and equity of 12 percent and 25 percent, respectively, in 2013, the highest in the industry.

Fig 1: Nigeria drug firms 2013 earning, margins and returns

Source: Company Financials, BusinessDay research

However, it incurred huge costs, which are due to the developments of health care products across West Africa. It is also aggressively penetrating and unleashing its products into Ghana with a view to extending its share of the market.

GSK was able to achieve an impressive result without incurring so much debt in its capital structure.

This explains the cost of sales margin of 60 percent and an operating expense ratio of 12 percent.

Fidson Pharmaceutical plc faces the same environment challenges that beset the industry in 2013. This includes huge debt and high operating and input cost due to expansion and development of new products.

Gross margin was 55 percent while net and pre-tax margins were 2 percent and 3 percent, respectively.

It recorded cost-of-sales margin of 45 percent and an operating expense margin of 49 percent.

May & Baker Pharmaceutical plc’s bottom-line slowed as a result huge debt incurred to fund the construction of a new N4 billion facility to meet the WHO pre-qualification.

Total borrowings were as high as N3.52 billion while the finance cost of N630.77 million ate up operating profits of N633.80 million, cumulating in a loss before tax of N11 million.

The company is highly geared as it has a debt-to-equity ratio of 116.1 percent. It means lenders have provided the large chunk to finance the company’s operations.

Neimeth Pharmaceutical plc recorded impressive top-line performance as full year revenues surged.

However, its margins were low as gross margins and net margins were 52 percent and 7 percent, respectively.

Furthermore, as peculiar to the sector, huge costs were incurred as cost of sales margin and operating expense margin were 48 percent and 45 percent, respectively.

Pharmadeko Pharmaceutical plc’s expansion drive and the upgrading of facilities to meet set standard has hit its bottom-line performance resulting in a loss of N228 million.

Debt-to-equity ratio was 96 percent, while cost of sales margin and operating expense margin were 58 percent and 57 percent, respectively.

PATRICK ATUANYA & BALA AUGIE

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp