Nigeria closed the second quarter of 2026 as the busiest destination for private capital on the continent, as African dealmakers logged more transactions than they had in the opening months of the year, even as the biggest cheques of the last quarter failed to reappear.

Fresh data from Stears’ Q2 2026 Private Capital in Africa Activity Report shows the continent recorded 221 private market transactions in Q2 2026, a 19 percent jump from 185 deals reported in Q1, though still 8 percent below the corresponding quarter last year.

The rebound came without the scale that defined the first quarter, when MTN’s $6.2 billion buyout of IHS Holding’s Nigerian assets and a $4 billion Dangote Refinery debt package pushed disclosed values to $16.7 billion.

Stripped of those outliers, disclosed value fell to $10.8 billion in Q2, from $16 billion reported in the first three months, the report disclosed.

Stears said that “value disclosure rose to 69 percent of transactions in Q2 2026, up from 58 percent in Q1, giving the quarter a broader disclosed base, even though aggregate value was lower than Q1.”

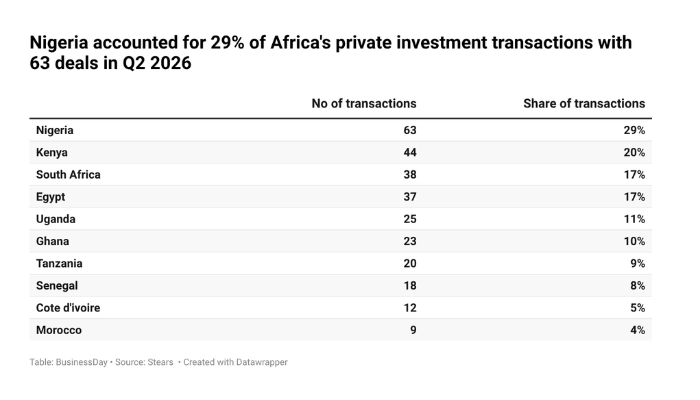

Nigeria stands out

Nigeria was the standout performer, accounting for 63 of the quarter’s transactions and carrying $8 billion of West Africa’s $8.9 billion in disclosed value. A $600 million loan facility from Africa Finance Corporation to Dangote Group’s Greenview Fertiliser Corp and a $268 million loan from the ECOWAS Bank for Investment and Development to Taraba State featured among the quarter’s notable single-country deals.

Egypt, by contrast, showed the tightest domestic concentration among the continent’s major markets, with Stears observing that the pattern suggests that Egypt’s activity was more domestically concentrated.

Followed by Kenya at 20 percent, South Africa at 17 percent, and Egypt at 17 percent. Egypt, however, stood out for single-country activity, with 25 Egypt-only transactions, accounting for 68 percent of its total country-linked deal count. Nigeria recorded the highest number of single-country deals at 32, representing 51 percent of its total activity, compared with South Africa at 39 percent and Kenya at 16 percent.

The middle market gets squeezed

Beneath the headline recovery, the shape of dealmaking shifted. Deals below $2.5 million widened to become the single largest ticket-size band, while mega deals above $75 million held their ground at 24 transactions.

The middle of the market, tickets between $2.5 million and $75 million, lost the most ground, falling to 37 percent of disclosed deals from 54 percent in Q1. Stears frames this as a market being squeezed from both ends, adding that “The middle bands were comparatively squeezed even as activity improved elsewhere.”

Financial Services loosens its grip

According to Stears, financial services remained the most active sector in Q2 2026, recording 52 transactions, although its lead narrowed from the previous quarter. Industrials, Energy & Utilities,

It added that consumer discretionary and information technology completed the dominant five, which together accounted for 181 transactions, or 82 percent of total deal activity. This was lower than the 85 percent recorded in Q1 2026, suggesting that activity remained concentrated in familiar sectors, but with a slightly wider spread than at the start of the year.

“Just like Q1, financial services sub-sectors led the way again on a sub-sector basis, with payments infrastructure accounting for $3.0 billion, equivalent to 28 percent of total disclosed transaction value in the quarter, while cross-border payments, B2B payments, B2C payments, and digital wallet platforms each recorded $2.8 billion, or 26 percent of total disclosed value.”

It said beyond financial services, telecom infrastructure and utility-scale solar were among the more active sub-sector themes in Q2 2026. Liquid Intelligent Technologies (Mauritius) and Project BRIDGE (Nigeria) secured investments in telecom infrastructure, while Axian Energy (Senegal) and a solar PV project (South Africa) attracted capital in utility-scale solar

M&A cools, exits stall

Mergers and acquisitions cooled from Q1’s elevated base, falling to 14 percent of recorded deals, with the $2.7 billion acquisition of cross-border payments platform Payoneer standing as the quarter’s largest, alongside a run of smaller AI-focused acquisitions by firms including CNTXT AI and Yoco.

Exit activity told the weakest story of the quarter. Only seven exits were recorded, the lowest count since late 2022, a sharp drop from the 32 logged as recently as the final quarter of 2025.

The pullback pushed Stears’ proprietary liquidity gauge, the SVL Index, to 82.46, its lowest reading in years. The report attributes this to the sharp fall in recorded exit volume, rather than a broad deterioration across all liquidity indicators, and cautions that reporting lags may lead to additional exits being added over time.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp