Background

Dangote Sugar Refinery (DSR) is a part of the Dangote Group, one of the most diversified business conglomerates in Africa. Dangote commenced operations in March 2000, as the sugar division of Dangote Industries Limited.

The company’s factory was designed and built by Tate and Lyle, UK, with an initial production capacity of 600,000 MT/annum of raw sugar. This was increased to1.44 million MT/annum in 2004, making it the largest sugar refinery in sub Sahara Africa and the second largest in the world.

The company has 12 billion shares outstanding with shareholder funds of N49.13 billion as of March 31, 2014.

Financial results for Q1 2014

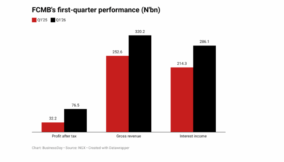

Dangote Sugar Refinery, Nigeria’s number one producer of the sweeter, has released its first quarter 2014 results, which showed bottom-line growth amid decline at the top line level. For the first three months of the year 2014, the company’s revenues reduced by 7.0 percent to N25.88 billion from N27.83 billion in the same period a year ago.

Profit before tax increased by 6.06 percent to N5.77 billion in the period under review compared with N5.44 billion as of Q1’2013. Profit after tax followed the same growth trajectory as it rose by 8.80 percent to N3.757 billion compared with N3.45 billion in same period of the prior year (Q1’13).

In order to increase its share of the market, the company introduced a wide range of products such as the Vitamin A fortified sugar packages in one kilogram, 500 grams and 250 gram packs.

The fortified white sugar was launched into the market to achieve the set target of higher sales volume, earnings and ultimately profitability.

Gross profit reduced slightly by 1 percent to N7.18 billion in Q1’14, from N7.23 billion as at Q1’13. This highlights the need for the company to intensify the management of direct costs attributable to projects.

Gross profit margin shows the relationship between turnover and cost of sales and is a proof of the company’s ability to control cost of inventories and to pass along any price increase through sales to client. Gross profit margin increased to 27.7 percent in Q1 2014 compared with 26.17 percent as of Q1 2013. This signifies that the ability of the company to translate turnover into profits improved.

The fixed assets turn over highlights the effectiveness of DSR in generating turnover from investment in assets. Total assets turnover was 30.28 times signifying the company’s ability to translate assets into turnover and profits.

The fulcrum of the improved performance at the bottom line level of DSR was the fall in operating expenses by 30 percent to N1.622 billion in Q1’14 compared with N2.33 billion in 2013, thus operating margin ratio declined to 6.26 percent in 2014 from 8.44 percent in 2013.

Inputs costs were also reduced marginally as cost of sales margin declined to 72.23 percent in Q1’2014, as against 73.18 percent as of Q1’2013.

Total assets for the first three months through March 2014 decreased by 3.92 percent to N85.46 billion in Q1’14, from N88.95 billion in 2013.

Dangote Sugar, which has a 70 percent share of the Nigerian market, plans to increase sugar production to 250,000 tons a year by 2017 and achieve 1 million tons output by 2020.

Share performance and outlook

The company’s share price has increased by18.35 percent in the past year to close at N9.17 on May 16, 2014, on the floor of the Nigerian Stock Exchange, and market capitalisation was N110.04 billion on the same day.

BALA AUGIE

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp