Nigeria’s main stock market index has returned -5.93 percent year to date (January 1st – April 12, 2019) and -23.9 percent in the past year (between April 2018 and April 2019), one of the worst performances globally for frontier/emerging market equities.

The Johannesburg Stock Exchange (JSE) by comparison is up +10.25 percent ytd, and +7.05 percent in one year, while the Nairobi exchange has returned +12.45 percent this year (ytd).

In Nigeria stocks are not a perfect proxy for the wider economy as total market capitalisation of N11 trillion represents only 8.5 percent of nominal GDP of N129 trillion (IMF estimates), at the end of 2018.

However, the performance of large listed companies in Nigeria such as Nestle (consumer goods), Dangote Cement (industrial materials), Seplat (oil and gas), Nigerian Breweries (Food and Beverage), and First Bank (Financials), which are components of the NSE-30 index (30 largest firms on the exchange), usually provides a clue as to what is happening in the broader sectors in which they operate.

The NSE – 30 firms make up some 96 percent of the entire market capitalisation of listed equities.

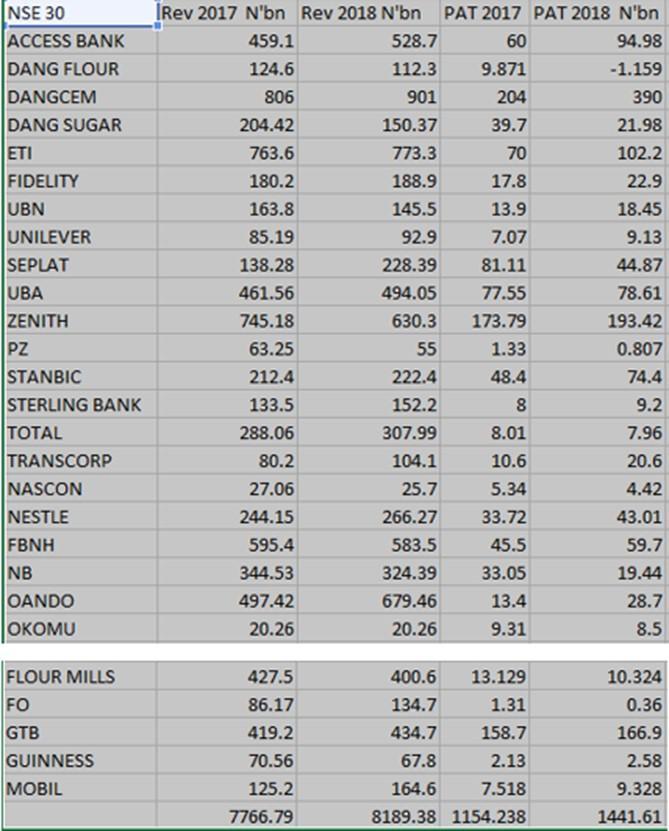

Total revenues for 27 of the 30 firms that have released Full Year, 2018 results as of Friday rose by 5.4 percent to N8.18 trillion from N7.76 trillion in 2017.

Combined profits for the same group jumped 25 percent in the period to N1.441 trillion from N1.15 trillion in 2017. (See chart).

Source: Company Financials

If firms are barely growing sales but recording a jump in profits it signals that other things such as cost cutting, FX trading/Treasury investments (for banks) or non-core operations are responsible for juicing profits.

Take First Bank for instance which released FY, 2018 results on Friday.

Revenues declined by 2 percent in the period to N583.5 billion from N595.4 billion, however profits rose by 31 percent to N59.7 billion.

Loans advances to customers also declined to N1.7 trillion from N2.0 trillion.

First Bank in a statement noted that “it is reflective of the weak macroeconomic environment that does not support aggressive risk asset creation.”

The direction of stock prices (whether rising or falling) is important because stocks are largely priced based on the expectations that prospective investors have for the future earnings of the company.

Falling stocks prices therefore means investors are not confident of higher overall growth in the economy which will boost revenues and eventually profits of firms.

Lower stock prices also often affects the ability of firms to raise equity capital through initial public offerings IPOs or rights issues.

Often, long periods of sell-off in stocks could result in lower valuations and discourage prospective capital raising.

Another negative implication from the stock market’s poor showing is the potential for Nigeria to lose a generation or two of young investors.

Domestic investor interest in the equity markets peaked some 10 years ago in 2007/2008, and majority have yet to return.

Lower equity prices also leads to negative wealth effect and sentiment which impacts consumer spending.

Some N6 trillion in market value has already been wiped out since the end of 2015, when total market capitalisation was N17 trillion, compared to N11 trillion today.

That the Nigerian economy is barely growing is probably not lost on investors.

Growth is forecast by the International Monetary Fund (IMF) to rise marginally to 2.1 percent from 1.9 percent in 2018.

It is highly unlikely that firms can grow revenues byupper single digits or double digits from such weak levels of expansion.

Looking at the numbers a lot of consumer goods firms have been particularly hit hard as disposable incomes remain largely stagnant.

Dangote Flour, Dangote Sugar, PZ, NASCON, Nigerian Breweries, and Flour Mills all saw a drop in revenues in 2018, compared to 2017.

If blue chip Nigerian companies who probably have easier access to credit and can command more favourable terms on interest rates and fees are struggling, then it signals more dire conditions for smaller firms and enterprises.

Getting the economy to grow fast again with firms building new plants and factories and hiring new workers, should help reduce unemployment which recently hit 23 percent as well as poverty.

In Indonesia, there is an old saying, that goes ‘good times leads to bad policies, bad times, leads to good policies.’

It is hoped that in the depths of the current bad times, the government will enact good policies to help turn things around and return positive sentiment and animal spirits to the capital markets.

PATRICK ATUANYA

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp