“I’ll allow Nigerians to say it. I hope they’ll be fair to me. I want them to analyse how things were when we came in and how they are when we’re leaving.” President Muhammadu Buhari uttered those words last year when quizzed about his legacy.

The government rode into power in 2015 on the change mantra, promising Nigerians a better deal than former President Goodluck Jonathan’s administration offered.

When Buhari became president in 2015, he promised to reform an economy hooked on petrodollars, reduce poverty, create jobs, and improve livelihoods in Africa’s most populous nation.

“Unemployment, notably youth unemployment, features strongly in our party’s manifesto. We intend to attack the problem frontally through the revival of agriculture, solid minerals, and mining, as well as credit to small and medium-size businesses to kick-start these enterprises,” Buhari said in his 2015 inauguration speech.

After eight years in power, Buhari’s supporters point to his “unprecedented infrastructure development” and a legacy of a social investment programme that is unparalleled in Africa, which has enhanced the quality of life of the beneficiaries.

Yet the numbers show that at no point in Nigeria’s democracy has the economy expanded slower than it did in the last eight years.

Slow economic growth

Data obtained from the National Bureau of Statistics (NBS) showed Nigeria recorded annual Gross Domestic Product growth of 3.1 percent in 2022, down from 3.4 percent in 2021.

Data obtained from the National Bureau of Statistics (NBS) showed Nigeria recorded annual Gross Domestic Product growth of 3.1 percent in 2022, down from 3.4 percent in 2021.

A closer look at NBS data showed Buhari holds the worst record out of the four presidents who have led Nigeria since it returned to democracy in 1999.

While President Olusegun Obasanjo can boast of an average growth rate of 6.9 percent during his eight-year tenure, his immediate successor, President Umaru Yar’Adua, did even better in a few years before he passed on, with an average growth rate of 7.1 percent, while Jonathan delivered 6.07 percent growth in his four-year term as president.

Under Buhari’s watch, however, the economy grew by an average growth of 1.40 percent.

Buhari’s supporters point to the crash in oil prices in 2016, the global pandemic in 2020 and the supply chain disruption caused by the Russia-Ukraine war as the reasons for his poor economic record.

His critics are, however, convinced it is a lot more than that.

Read also: Upstream regulator hosts communities to boost oil, and gas production capacity

Higher inflation

The rising inflation rate has been a major bane of the Nigerian economy and has recently been a topical issue, given the fast rise in the prices of goods and services in the country and across the globe.

Of the four presidents, Nigeria recorded its highest average inflation rate under the current administration, which according to the NBS’s latest figure, quickened to 22.04 percent in March 2023.

Nigeria recorded an average inflation rate of 12.3 percent, with an opening rate of 8.28 percent in June 1999 and a closing rate of 4.64 percent in May 2007.

During the eight years of Obasanjo, Nigeria recorded its highest inflation rate in August 2005, after the consumer price index surged by 28.21 percent, before moderating back to single digits.

During his tenure, Obasanjo introduced N100, N200, N500, and N1,000 denominations into the economy, which is argued to have fuelled inflationary pressure.

During Yar’Adua’s administration between 2007 and 2010, Nigeria recorded an average inflation rate of 11 percent. The late president took over the presidency in May 2007 following a 4.64 percent inflation but saw inflationary pressure gallop to 15.04 percent before he died.

The highest rate during his administration was recorded in February 2010 at 15.65 percent.

His administration was, however, marred by high insecurity in the Niger Delta and insurgency in the northern regions of the country, which almost brought the nation to its knees, with several reported cases of kidnappings of foreign expatriates in the South and mass killings in the North.

Jonathan, who was Yar’Adua’s deputy, inherited a high inflation rate from his predecessor. However, during his six years as the president of the largest African economy, an average inflation rate of 10.22 percent was recorded.

He met inflation at 15.04 percent but saw it decline to 9 percent at the end of his tenure while operating under similar macro and socio-economic conditions as his predecessor.

During the period, Nigeria also endured massive killings in the North by the Boko Haram insurgent group, although with a decline in the activities of the militants in the Niger Delta region, thanks to the Amnesty Programme established by the previous administration.

Under Buhari, Nigeria experienced an average inflation rate of 14.52 percent between June 2015 and December 2022, recording a 17-year high of 21.34 percent in November 2022.

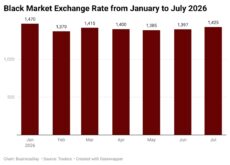

Exchange rate:

Nigeria’s exchange rate has consistently depreciated since 1999, but under the administration of Buhari, it depreciated to record lows.

During the tenure of Obasanjo, the country’s exchange rate was between N98.02 to N116.8 per dollar.

Under the Yar’Adua/Jonathan-led government between 2007 and 201o, the country’s exchange rate also moved from N116.8/$1 to N149.2/$1.

At the beginning of Jonathan’s tenure as a democratically elected president in 2011, the country’s exchange rate moved from N149.2/$1 to N197/$1 in 2015.

Under Buhari, the country’s exchange rate moved from N197/$ in 2015 to N460/$ as of May 5, 2023.

External debt:

Nigeria’s public debt has been on the rise. Despite securing debt relief during the Obasanjo-led administration, successive governments have continued on a borrowing spree.

On external borrowings, Buhari increased debt from $7.3 billion in 2015 to $41.69 billion as of December 2022. This means that the president incurred $34.39 billion in foreign loans.

Analysis of the figures showed that external debt decreased from $28.04 billion in 1999 to $2.11 billion at the end of 2007. However, the domestic component increased from N798 billion to N2.17 trillion within the same period.

The huge decline in foreign debt was a result of the substantial reduction following the pay-off of the outstanding debts owed to the London Clubs of Creditors in the first quarter of 2007.

Fiscal deficit

Prior to 2014, the federal government’s revenue shortfall – that is the variance between actual and budgeted retained revenues – was in the billion-naira range but with the collapse in oil prices, the difference has stayed within the trillion-naira range.

Africa’s biggest economy plans to spend N21.8 trillion against revenue of N10.5 trillion in 2023, according to the budget signed on Jan. 3 by Buhari, who will leave office on May 29.

That leaves a deficit of N11.3 trillion, which will be plugged largely by borrowing.

In the 2023 budget, the fiscal deficit to GDP amounts to 4.78 percent, and according to Section 12 (1) of the Fiscal Responsibility Act (2007), the fiscal deficit should not exceed 3 percent of the estimated GDP, except there is a clear and present threat to the national security and sovereignty of Nigeria.

Rising insecurity

Despite repeated assurances from Buhari and the security chiefs, many Nigerians are at the mercy of bandits, terrorists and other criminals who are ravaging many parts of the country.

A report by SBM Intelligence, Lagos-based security and political risk research firm, showed about N653.7 million was paid as ransom in Nigeria between July 2021 and June 2022 for the release of kidnap victims.

“Based on what we could verify, between July 2021 and June 2022, no fewer than 3,420 people were abducted across Nigeria, with 564 others killed in violence associated with abductions. In the ensuing period, N6.531 billion was demanded in exchange for the release of captives while a fraction of that sum (N653.7 million) was paid as ransom,” the report said.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp