Nigeria’s higher growth rate in the second quarter of 2021 as well as slowing inflation are not likely to pave the way for Africa’s biggest economy to reduce interest rates as the Monetary Policy Committee (MPC) enters its two-day meeting today.

Nigeria’s economy grew at 5.01 percent in the second quarter of 2021 from 0.51 percent in the first quarter of the same year, data from the National Bureau of Statistics (NBS) show.

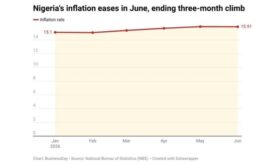

On a positive note also, the inflation rate slowed for the fifth straight month to 17.01 percent in August 2021, from 17.38 percent recorded in July, the same year, NBS report indicated.

The majority of analysts polled by BusinessDay expect the Central Bank of Nigeria (CBN) to retain the Monetary Policy Rate (MPR) after the MPC meeting on Friday, despite rising growth rates and slowing inflation.

They are of the view that the inflation rate is still high and well above the CBN’s 6-9 percent target and that the rising growth is not supported by strong economic fundamentals.

There is also the small matter of the continued pressure on the exchange rate.

“I expect the MPC to hold rates given the Gross Domestic Product (GDP) growth in the last quarter was mainly due to the base effect rather than growth supported by strong economic fundamentals,” says Taiwo Oyedele, head of tax and corporate advisory services at PwC.

Also, he says while it is good that inflation is moderating, 17 percent is still quite high and well above the targeted single digit. It is important to ensure that monetary policies support and not upset the slow and fragile economic recovery.

Nigeria’s central bank has kept its monetary policy stance at 11.5 percent since September 2020 following fragile growth and inflation.

Uche Uwaleke, chairman, Chartered Institute of Bankers of Nigeria (CIBN), Abuja branch, says, “I expect the MPC to maintain the status quo and hold all policy parameters.”

Read Also: Considering inflation, CBN holds benchmark interest rate at 11.5%

He says it would have been desirable to reduce the MPR by a few basis points in order to spur economic recovery. But this path may not be toed given the current pressure in the forex market and the widening gap between the official, Investors and Exporters (I&E) exchange rates and the unofficial market rates.

Uwaleke also notes that although the inflation rate has started decelerating, it is still elevated and way beyond the CBN’s upper band of 9 percent.

“Also, a reduction in MPR may not be in the interest of foreign investors usually incentivised by higher interest rates,” Uwaleke states.

On the other hand, raising the MPR at this time will hurt recovery via increase in cost of capital, especially for SMEs. It will equally slow down the stock market which is still experiencing weak investors’ sentiments. “On the basis of these considerations, the MPC will most likely maintain a hold stance,” Uwaleke says.

Analysts at Meristem Research say the decelerating inflation rate will be a major consideration for the Committee. “In our opinion, this should buy more time for the Committee to allow the existing policy to permeate the economy,” the analysts say.

The analysts note that since the MPC last met in July 2021, some developments have occurred. The Petroleum Industry Act (PIA) was officially signed into law by the President on August 16, 2021. While this move has been applauded considering its benefits to the oil and gas sector, it has also been critiqued on timeliness and provision for host communities.

“While we acknowledge that the improvement in economic growth would be a key consideration for the committee, our expectation is that the committee would maintain the status quo, favouring its pro-growth stance,” the Meristem analysts say.

In its note generated on July 20, 2021, the Economist Intelligence Unit (EIU) said the CBN will fail to keep inflation below a target ceiling of 9 percent, and its policy decisions are likely to remain erratic. Since a 100-basis-point cut to 11.5 percent in 2020 the policy rate has been kept steady. Inflation is high year-on-year, at 17.9 percent in May, but the rate has edged down from a decadal high in March.

The current strategy is to boost the supply side of the economy and thereby control inflation. “We believe that this is misguided; high inflation will frustrate an economic recovery, and issues such as inadequate public infrastructure, hard-currency shortages and rampant instability need to be addressed before the supply side can substantially contribute to moderating the price level.”

Enduring high inflation is expected to compel the CBN to raise interest rates in 2022, as the economy becomes more resilient. Monetary easing will resume only in 2024, when inflation has fallen appreciably, says the London-based EIU.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp