Nigeria’s economy has been shrinking for the past few years, and the situation is not getting any better.

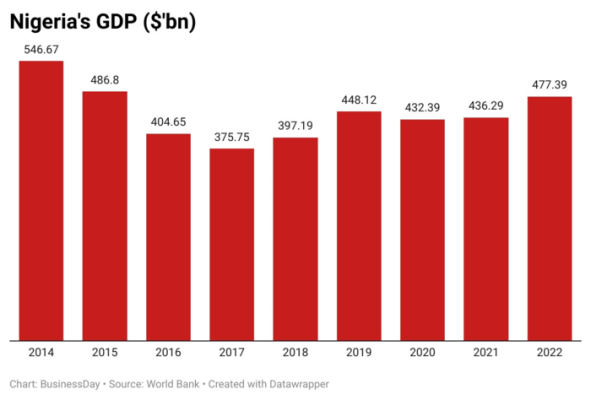

The value of the economy declined to $477 billion in 2022 from $546 billion in 2015, according to BusinessDay’s calculations.

The shrinking size of the economy means there is a smaller pie to share among Nigeria’s 200 million people, a painful squeeze for a country that is home to the world’s largest number of poor people.

That explains why many Nigerians cannot relate to unemployment figures put out by the National Bureau of Statistics (NBS), according to Wale Lawal, a Nigerian youth who has been without a job since 2015.

Analysts said its fractured political class is struggling to find answers to long-term headaches and short-term crises, leading to a growing sense of malaise.

Read also: Adegboyega Oyetola takes up the gauntlet at Marine and Blue Economy Ministry

“We’ve done a lot of talking in the last 10 years but achieved very little in terms of growing the economy,” Kelvin Atafiri, the CEO of Cavazanni Human Capital Limited said.

“The country is currently leaving on past glory,” he added.

A research report by the World Bank revealed that from 2004 to 2014, Nigeria witnessed a surge in the number of middle-income earners as a result of its fast economic growth, which can be largely attributed to a form of structural change in economic activities from the traditional-agricultural sector to the service sector.

However, things are no longer the same for the once vibrant ‘Giant of Africa’ as major households continue to get vulnerable to its unstable economy.

This is evidenced by the World Poverty Clock report where Nigeria got tagged as the world poverty capital for three consecutive years until recently when the baton was handed over to India.

“Since 2015, Nigeria’s economy has been grappling to survive as its overvalued currency continues to translate into a persistently high inflation rate alongside a high rate of unemployment and poverty that has defied all economic interventions,” Luqman Agboola, head of research at Sofidam Capital said.

Other analysts said its over-dependence on oil has made it particularly vulnerable to recent global turbulence: supply chain disruption, Covid19 pandemic, surging energy prices, rise in inflation and interest rate that has led to a global slowdown.

Read also: Stable economy, policy continuity will attract foreign investments; Borodo, CIoD President

“Nigeria is losing its middle-class category to foreign countries. The service sector especially seems to be at the receiving end of this dilemma as many of the professionals who are contributing to Nigeria’s human capital development seem to have had enough of a poor and unrewarding economy,” Agboola said.

According to a 2022 survey by the Africa Polling Institute, a staggering 69 percent of Nigerians would relocate out of the country with their families if given the chance.

Almost 80 percent will leave this 2023, while only 39 percent were willing to emigrate in 2019, according to the same poll.

“The middle class has disappeared due to lack of jobs or shrinking wages,” Ola Alokolaro, partner at Advocaat Law Practice said.

Presently, Nigeria’s current minimum wage of N30,000 seems to be a far cry from what it should be given the current economic circumstance. As of 2019, when the figure was approved, the inflation rate was 11.40 percent.

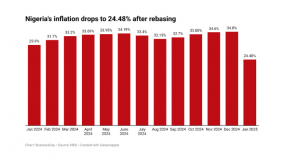

Presently, the rate of inflation in Nigeria has hit 22.79 percent, which has generated a public outcry as the World Bank revealed that Nigeria needs to urgently introduce a robust economic reform that will address mounting fiscal pressures, boost private investment to create jobs and also come up with policies that will address the poor living standards of its people

“An all-out effort is needed to diversify Nigeria’s fiscal base away from oil. In the context of an economic downturn, raising revenue will be difficult. But fiscal reforms, especially creating a more stable revenue base, will be necessary for long-term sustainability,” a senior chief economist said in response to questions.

“Priority expenditure will need to be protected. While capital expenditure boosts growth, it is necessary to reduce the amount of recurrent expenditure,” he added.

Agora Policy, an Abuja-based think tank set up to find practical solutions to urgent national challenges, recommended ways the new government in Nigeria can fix the nation’s economy.

The most critical policy issue for the Federal Government, the paper states, is inadequate revenue.

It argues that the Fiscal Responsibility Act mandates revenue-generating agencies to remit 80 percent of their operating surpluses to the Consolidated Revenue Fund and retain 20 percent in their reserve fund.

Agora Policy said, “There are many revenue-generating agencies that either fail to remit any revenue, or remit a very small fraction to the government”.

The think tank recommended that “the Fiscal Responsibility Act should be amended to stop funding revenue-generating agencies from the Federal budget; and set penalties for agencies that fail to remit their stipulated operating surpluses”.

The report showed that Nigeria has recorded persistent trade deficits in recent years, clocking a deficit of N1.9 trillion in 2021.

To tackle this, Agora Policy recommends that “the distortionary non-tariff measures need to be urgently reviewed and/or phased out”.

“These include the foreign exchange restrictions on 42 products by the CBN; review of the import prohibition and absolute import prohibition lists and perhaps replacing these trade policy tools with tariff duties or import quotas; change in government policy on border closure from partial reopening to the full reopening of closed land borders”.

The organisation argued that there is “a need to urgently increase investment in digital technology in rural areas to create more jobs and economic opportunities”.

The report says to create more jobs, the government needs to tackle insecurity in rural areas, access to finance, and deal decisively with corruption, bureaucracy and red tape in administrative processes by government officials.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp