The Financial Times Africa Editor, David Pilling, wrote an article last month where he asked “What is Nigeria’s government for?”

One of the possible answers to that is the government now exists to pay creditors. Not to invest in education, healthcare or infrastructure, as is expected of a developing economy with promising human capital and a huge infrastructure deficit.

The International Monetary Fund (IMF) is projecting Nigeria will spend 92 percent of its earnings paying creditors this year. Agusto and Co, a local credit ratings firm, says the figure will be around 90 percent.

If these projections do happen, it will be by far the most any country pays as a percentage of revenue servicing debt.

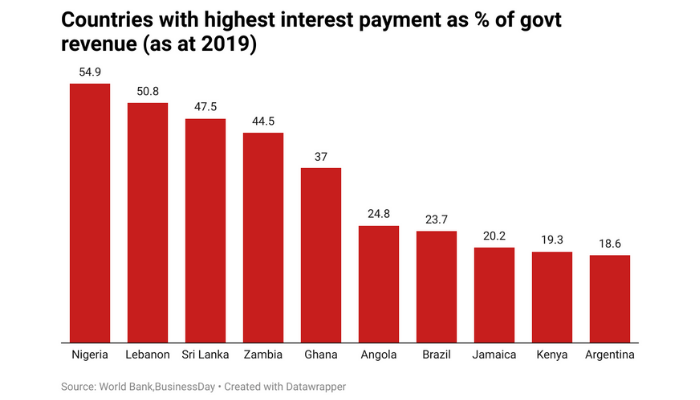

Nigeria was already spending the highest as a percentage of its revenue of any country repaying creditors back in 2019, according to data from the World Bank.

In 2019, Nigeria spent N54 of every N100 it earned, more than half, servicing debt. The country closest to Nigeria, Lebanon, was spending 50.8 percent of its revenues.

Nigeria being ahead of Lebanon is in itself a big indictment. Lebanon is grappling with a deep economic crisis after successive governments piled up debt following the 1975-1990 civil war with little to show for their spending binge.

Read also: African govt, banks, SMEs to benefit as $10bn AfCFTA Adjustment Fund debuts

Lebanese banks, central to the service-oriented economy, are paralysed. Savers have been locked out of dollar accounts or told that funds they can access are now worth a fraction of their original value. The currency has crashed, driving a swathe of the population into poverty.

Nigeria is not much different. There’s little to show for the government’s debt binge and the country is now the world’s poverty capital, overtaking India with five times its population, according to the Brookings Institution.

A Lebanese who owns a business in Nigeria told BusinessDay that he fled his country due to the economic hardship but admits Nigeria is increasingly towing his country of origin.

“Everywhere I go something bad happens,” he jokes. “The Nigerian situation has not yet deteriorated to what is obtainable in Lebanon but there are signs it is only a matter of time before it does as Nigeria is heading the same path; piling debt with nothing to show for it, but then the creditors are at the door,” the Lebanese business owner said.

But the situation risks being even worse.

If Nigeria starts spending 92 percent of its revenues on debt servicing, it means the government is nearing crisis levels where there may even be more recourse to further borrowing to repay existing creditors.

“We will be back to the 80s or perhaps even worse if that happened,” an economist who did not want to be named said. “Then the government used borrowed money to pay for old borrowings and the debt service cost was usually the first line item on the expenditure side of the budget,” the economist said.

The government seems oblivious to the impending crisis. In its 2022 budget, less than 40 percent of revenues is earmarked for debt servicing. But the trend of lower than planned actual revenues means analysts hold the estimate with a pinch of salt.

“The worry is that Nigeria’s rapidly growing foreign debt stock does not reflect shrinking oil revenues and we need to be careful not to fall into the 1980s debt trap where a huge chunk of revenues went to debt service,” said Egie Akpata, a director at Lag0s-based investment bank, UCML Capital.

The government’s resistance to ditching costly petrol subsidies makes it easy to see why the IMF expects Nigeria to eclipse its own record of debt service as a percentage of revenue.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp