…Olayemi Cardoso took over after previous chief printed money to fund deficits

Nigeria’s central bank governor indicated interest rates would stay high for as long as necessary to tame inflation, saying the institution had moved decisively to an “orthodox policy” after being plagued by scandal under his predecessor.

Olayemi Cardoso, a former Citigroup executive who became central bank chief in September, told the Financial Times that there was “every indication” that the monetary policy committee he chairs would “do whatever is necessary” to keep soaring inflation in check.

“They will continue to do what has to be done to ensure that inflation comes down,” Cardoso said, ahead of the central bank’s meeting on May 20-21, where some analysts expect a further chunky rate hike.

Cardoso’s stance is in sharp contrast with his predecessor Godwin Emefiele, who oversaw an inflation crisis in Nigeria as the central bank regularly printed money to fund government deficits beyond the 5 per cent limit permitted by law.

Emefiele is currently on trial for corruption charges that he denies, having been ousted as governor last year after nine years in the job.

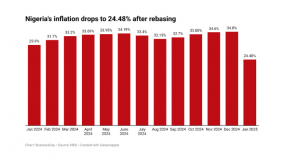

Inflation in Nigeria remains stubbornly high at 33.2 per cent, the highest in three decades. Food inflation is higher still at 40 per cent, a sharp blow to the living standards of poorer citizens who devote a larger share of their income to staples, such as rice. Assaults on grain warehouses have been reported across the country.

“Let’s face it: for a long period of time, the CBN did not embrace orthodox monetary policies,” Cardoso said. “We want to go back to using an orthodox method, and it will take us to where we want to go.”

Cardoso stressed that the apex bank, as the central bank is known in Nigeria, had been “reoriented” to focus on “price and monetary stability”. It hiked rates by 400 and 200 basis points in February and March respectively, lifting the key lending rate to 24.75 per cent.

The moves were praised by investors for halting the slide in the naira against the US dollar. The Nigerian currency hit a record low of N1,625 on March 11 before recovering to N1,284 last month, according to LSEG data.

While the naira has since lost some of those gains, Cardoso said the situation had now stabilised. Investors had previously had a “tendency to head for the window” in response to currency fluctuations, he said. But now, he said, there had been a “fundamental shift”. “They’re getting more comfortable with the market.”

Markets have generally welcomed the CBN’s stance under Cardoso.

“The return to orthodoxy has been very much endorsed by investors,” said Razia Khan, chief economist at Standard Chartered Bank. “While Nigeria is not seeking an IMF programme it is implementing the kind of policies that would be endorsed by the IMF.”

The IMF said in its latest Nigeria report last week that the central bank had “unequivocally committed to price stability as its core mandate” and urged the bank to keep monetary policy tight to fight inflation and build the country’s external reserves.

Yet Cardoso’s policies do not receive universal domestic support, with businesses complaining about the high cost of credit even as foreign portfolio investors have gradually returned to the country.

Cardoso said he hoped that high rates would not “linger” for too long and act as a disincentive to investment and production.

But he said that raising rates had been essential. “Hiking interest rates obviously has had a dampening effect on the foreign exchange market, so that has begun to moderate. It’s not a zero-sum game. You lose on one side, you get on the other.”

Revamping the central bank is a key plank of President Bola Tinubu’s attempts to re-engineer Nigeria’s faltering economy, which lost its place in 2022 as the biggest on the continent thanks to sluggish growth and the weaker naira. Nigeria’s economy is now smaller than that of Egypt and South Africa. The IMF expects it to fall to fourth place behind Algeria this year.

Last year, Tinubu partially removed popular but costly fuel subsidies while the central bank ended the currency peg that allowed the naira to be overvalued against the dollar. Although the government says the reforms will bear fruit in the medium term, Nigerians have been grappling with the worst cost of living crisis in a generation as a result.

Cardoso conceded that inflation was higher than he had hoped, blaming “distortions” mainly because of high food prices. “That obviously is something that is not directly within our control,” he said.

The central bank has not updated its inflation target of 6-9 per cent for more than a decade, but analysts expect this will be revised upwards.

Dumebi Oluwole, a senior economist at Lagos-based data firm Stears, said they expected inflation to fall to between 23.9-25.8 per cent by the end of the year.

“The central bank is on the mark with what needs to be done,” Oluwole said. “But we have to remember that Nigeria’s inflation is a lot more structural. Issues like insecurity are affecting our ability to produce food and that is inducing food inflation.”

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp