The International Monetary Fund (IMF) has urged the Central Bank of Nigeria (CBN) to stop financing the Federal Government’s budget deficits in order to tame soaring inflation.

“In the medium term, the monetary policy operational framework should be reformed and Central Bank financing of budget deficit phased out in order to reduce inflation,” the IMF stated in its Article IV consultation with Nigeria released Monday afternoon.

External vulnerabilities due to lower oil prices and weak global demand have increased, with Nigeria’s current account remaining in deficit in the first half of 2021.

“Directors observed that the accommodative monetary stance remains appropriate in the near term, although tightening may be warranted if balance of payments or inflationary pressures were to increase,” the fund noted in the mailed report.

The IMF also estimated that Nigeria’s economy, which is currently facing a difficult recession, may have contracted by 3.2 percent in 2020. It further warned that multiple rates, limited flexibility, and prevailing foreign exchange shortages are posing challenges to the already weak economy.

“Nigeria’s economy has been hit hard by the COVID-19 pandemic. Following a sharp drop in oil prices and capital outflows, real GDP is estimated to have contracted by 3.2

percent in 2020 amidst the pandemic-related lockdown,” the IMF said.

Read Also: Banks show resilience but rising credit exposure, NPLs are concerns – IMF

Under Article IV of the IMF’s Articles of Agreement, the IMF holds bilateral discussions with members, usually every year. A staff team visits the country, collects economic and financial information, and discusses with officials the country’s economic developments and policies. On return to headquarters, the staff team prepares a report, which forms the basis for discussion by the Executive Board.

In the report, the IMF recommended a gradual and multi-step approach to establishing a unified and clear exchange rate regime with the near-term focus on allowing for greater flexibility and removing the payments backlog.

The IMF commended the authorities for the measures taken to address the health and economic impacts of the COVID-19 pandemic which have exacerbated pre-existing weaknesses.

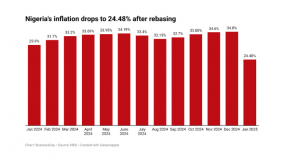

However, Nigeria’s economy remains in a precarious situation. Headline inflation rose to 14.9 percent in November 2020, a 33-month high, reflecting core and food inflation increases emanating from supply shortages due to the lockdown effected to curb infections, alongside the land-border closure and continued import restrictions.

The unemployment rate reached 27 percent in the second quarter of 2020, with youth unemployment at 41 percent.

IMF is concerned that “socio-economic conditions have deteriorated, with rising food inflation, elevated youth unemployment, mass protests in October 2020, and surveys show worsening food insecurity with a significant impact on the vulnerable”.

It further notes that “risks are tilted to the downside and include the resurgence of the pandemic, security situation and unfavourable external environment”.

“Capital outflow risks arise from the record-low domestic interest rates and large foreign holdings of domestic securities. On the upside, recovering oil prices and completion of the Dangote oil refinery could catalyse more domestic crude oil production and boost growth,” it said.

The fund, however, commended the authorities for acting swiftly to adopt a pandemic-related support package equivalent to 0.3 percent of GDP in the 2020 revised federal budget despite limited fiscal space. This includes accessing the IMF $3.5 billion emergency financial assistance under the Rapid Financing Instrument, last April, to help cushion the impact of the pandemic.

Looking ahead, the IMF emphasised the need for urgent policy adjustment and more fundamental reforms to sustain macroeconomic stability and lift growth and employment.

While welcoming the resilience of the banking sector, they called for continued vigilance to contain financial stability risks.

They noted that COVID-19 debt relief measures for bank clients should remain time-bound and limited to those with good pre-crisis fundamentals.

Notable reforms undertaken in the fiscal sector, including removal of the fuel subsidy and steps to implement cost-reflective tariff increases in the power sector, also received commendation.

However, there is the need for significant revenue mobilisation to reduce fiscal sustainability risks, relying initially on progressive and efficiency-enhancing measures with higher tax rates awaiting a more sustained economic recovery, according to the IMF.

The fund equally highlighted the need for improved social safety nets to cushion potential negative impacts on the poor, welcomed recent progress in structural reforms and called for continued reforms aimed at promoting economic diversification and reducing the dependence on oil and increasing employment.

In addition, it encouraged strengthening governance and anticorruption frameworks, including compliance with AML/CFT measures.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp