Nigeria’s sweeping economic reforms have reignited investor confidence and earned praise from global institutions, but the toll on the nation’s poorest citizens has cast a shadow over the gains.

As Africa’s largest economy charts a new course towards fiscal stability, the International Monetary Fund (IMF) has sounded a cautionary note — urging the government to cushion the reforms’ harshest impacts with targeted social investments.

During her first visit to Nigeria, Gita Gopinath, the IMF’s First Deputy Managing Director, commended the government for implementing long-overdue measures such as the liberalisation of the foreign exchange market and the removal of fuel subsidies.

However, she warned that the benefits of these reforms could be undermined if social protection programs are not accelerated.

“The removal of fuel subsidies, while necessary, has exacerbated hardship for many Nigerians, with the poverty rate rising to 47% in 2024,” she said in an exclusive interview with BusinessDay. “The government needs to rechannel the savings from subsidy removal into social safety nets for vulnerable households.”

Read also: Nigeria’s GDP per capita down to $835 in 2025 – IMF

A double-edged sword

The removal of fuel subsidies, which had cost the government billions of dollars annually, was widely regarded as an unavoidable step to curb unsustainable public spending.

However, the immediate consequence has been a sharp rise in the cost of living, the worst in a generation, pushing more Nigerians below the poverty line.

Similarly, the naira’s devaluation following the liberalisation of the foreign exchange market, while positive for attracting foreign investment, has led to higher inflation, especially for food and imported goods.

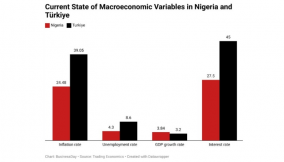

Inflation has remained one of the most visible indicators of economic distress.

Although the rebasing of Nigeria’s inflation index by the National Bureau of Statistics (NBS) brought the official rate down to 24 percent in January 2025 from 34 percent in December 2024, the perception on the streets tells a different story.

“Inflation at over 20 percent is still very high, and it’s no surprise that people feel the squeeze,” Gopinath said. “Tight monetary policy will be essential, along with efforts to stabilize the currency and avoid central bank financing of fiscal deficits.”

Lessons from peers

Nigeria is not the first country to undergo painful economic reforms.

Countries like Egypt and Indonesia have implemented similar subsidy removals and exchange rate liberalisations in recent years — but both balanced their reforms with social investment programs.

Egypt’s Takaful and Karama cash transfer programs expanded rapidly in the wake of subsidy cuts, reaching millions of vulnerable households. Indonesia, too, ramped up direct cash transfers and healthcare subsidies alongside energy price reforms.

What is Nigeria doing?

At a meeting with the IMF’s Gopinath, in Abuja, the Minister of Finance and Coordinating Minister of the Economy, Wale Edun, outlined the government’s transition to a biometric-based system aimed at improving transparency and efficiency in social investment programmes.

The shift, he said, is expected to enhance accountability and ensure that support reaches those who need it most.

Edun also outlined key economic policies which focused on tax reforms, revenue assurance mechanisms and digitalisation to improve domestic revenue generation. He noted that Nigeria’s crude oil production has risen from 1.2 million to between 1.7 and 1.8 million barrels per day, significantly boosting national revenue.

The revenue puzzle

A critical factor that will determine the success of Nigeria’s balancing act for reforms and social protection is the government’s ability to raise domestic revenue. With government revenue standing at under 10 percent of GDP — one of the lowest in the world — there is little fiscal space to fund large-scale social programs.

“Raising domestic revenue through better tax collection, reducing exemptions, and improving tax administration will be key,” Gopinath advised. “Transparent and efficient tax systems will be critical to unlocking higher revenues.”

The ongoing tax reforms, which include automation of tax administration and a reduction in tax waivers, represent a step in the right direction. However, analysts say much more needs to be done to broaden the tax base and ensure that wealthier Nigerians pay their fair share.

A path to inclusive growth

Ultimately, the success of Nigeria’s reforms will be measured not just by macroeconomic stability or investor confidence, but by how much they improve the lives of ordinary Nigerians.

Sustained investments in health, education, and infrastructure, alongside targeted social protection programs, will be crucial to breaking the cycle of poverty.

“These reforms must be sustained consistently over many years to yield meaningful results,” Gopinath warned.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp