Analysts have expressed their views on when Nigeria can tap the Eurobond market this year to raise funds in a bid to boost external reserves and improve foreign exchange inflows.

They said the potential benefits of taking advantage of lower interest rates in developed markets could drive investor interest in Nigeria’s Eurobonds and potentially lead to an increase in credit rating.

A Eurobond is a fixed-income debt instrument (security) denominated in a different currency than the local one of the countries where the bond is issued.

Last month, Wale Edun, minister of finance and coordinating minister of the economy, revealed that the country may tap the Eurobond market later in the year if rates move sufficiently lower.

In an interview with Bloomberg TV on the sidelines of the World Economic Forum in Switzerland, Edun said the major issuers and the book runners had told them that there should be a window for Nigeria in the Eurobond market.

“I believe the time is almost right for Nigeria to consider the Eurobond market for many reasons. The country can consider an issuance in the second quarter of this year. The inflows would boost our reserves, provide a bit of confidence for foreign investment, and could also provide some optimism for the FX market,” Temitope Omosuyi, investment strategy manager at Afrinvest Limited, said.

On the reasons why Africa’s biggest economy should tap into the market, he said the country has a “Eurobond maturity due next year amounting to $1.2 billion, which would add to over $1.0 billion typically used to service external obligations annually”.

“Secondly, the massive oversubscription for the Ivory Coast auctions this year shows commendable investor appetite for the African Eurobond market. Yields are still very attractive in this market compared to advanced economies. Nigeria can leverage this appetite to explore the market,” he said.

He added that the expectation is that yields will still decline further as interest rates go down in advanced economies. “It therefore means that Nigeria is better placed to borrow at a relatively low cost in the market.”

Omobola Adu, senior economist at BancTrust & Co, said Nigeria can go into the market most likely in the second half of the year, once global markets start easing interest rates.

“There isn’t pressing external debt repayment needs for Nigeria to force them to go to the market; the only compelling reason is to support FX liquidity conditions,” he added.

The last time Africa’s most populous nation tapped the international debt market was in March 2022, when it raised $1.25 billion through a seven-year Eurobond.

“I would advise they do it early in Q2 because the global market in the last three years has had unanticipated shocks e.g. the Russia-Ukraine war,” said Damilare Asimiyu, a Lagos-based macroeconomic strategist.

“Raising Eurobond will help strengthen our reserves because other sources of raising reserves are not looking good like foreign portfolio investments. So, for the sake of FX, we need to tap into that market fast,” he added.

Tajudeen Ibrahim, director of research and strategy at Chapel Hill Denham, said opting for the Eurobond market now would likely entail higher interest rates, potentially in double digits.

“So, I think there is a need for Nigeria to wait for a dovish monetary policy rate from the US and also improvement in credit rating before we begin to think of going to the market,” Ibrahim said.

The continued decline in the country’s foreign exchange reserves followed low revenue from crude oil sales and increased demand for FX, among other factors.

Data from the Central Bank of Nigeria (CBN) showed that external reserves, the stock of foreign assets held by the apex bank, declined to $33.2 billion as of February 15, 2024 from $36.8 billion a year earlier.

In June, the apex bank merged all segments of the FX market into the Investors and Exporters window and reintroduced the willing buyer, willing seller model.

The liberalisation of the FX regime as part of measures to revive the economy led to a large devaluation of the naira.

The currency depreciated from N463.38/$ to N1,574.6/$ as of February 19. At the parallel market, the naira depreciated to 1,800/$ from 762/$.

Considering the oversubscription of Eurobonds in the African market, the government may opt to delay bond issuance until later in the year, as this strategy aligns with expectations that the central banks of advanced economies would start reducing rates, said Sesan Adeyeye, a Lagos-based financial analyst.

“This strategy aligns with expectations that as central banks of advanced economies start reducing rates, emerging markets may become more appealing to foreign investors. With a strong appetite for emerging market investments, it’s deemed advantageous for Nigeria to raise bonds in the latter part of the year,” he said.

Ayooluwade Ogunwale, a fixed income analyst at Cordros Securities, said the issuance of Eurobonds is likely to be in the second half of 2024 largely due to global interest rates and expectation of lower yield.

“I anticipate that the Eurobond issuance will probably occur in the latter half of the year, primarily driven by global expectations of lower yields in the second half. This timing would enable the country to raise the bond at minimal cost, especially considering the absence of any USD commercial debt maturity this year, which enhances the country’s position,” he said.

Ogunwale added that before the second half of this year, there should be an uptick in credit ratings from foreign rating agencies which will make the country raise debt in the latter half of the year.

Joshua Joseph, a fixed-income trader at CSL Stockbrokers Limited, pointed out that while the government must address the FX issue by entering the Eurobond market, they have also been assertive in the local market.

Benin Republic’s first-ever dollar-denominated bond – a $750 million issue – was oversubscribed to the tune of $5 billion on February 7 as investors lapped up the debt of the small West African nation.

The bond sale by Benin Republic comes two weeks after Ivory Coast raised $2.6 billion at a rate of between 8.5 and 8.75 percent in an oversubscribed Eurobond auction.

A recent report by BancTrust & Co. said Ivory Coast’s auction potentially signalled the re-opening of the international bond market to issuers in Sub-Saharan Africa.

“While the reopening is still subject to how the new issuances trade in the secondary market as well as the individual fundamentals of potential issuers, we believe a potential market re-opening would broadly be a positive for the region,” the report said.

It added that Angola, Kenya, and Nigeria have over the last 12 months indicated a willingness to issue, dependent on market conditions while Ghana continues negotiations on its external debt restructuring goals.

“The timing and size of potential new issuances from the names mentioned above are still subject to debate as most Eurobonds are still trading a considerable distance away from levels Ivory Coast issued as well as the respective nation’s most recent issue levels.”

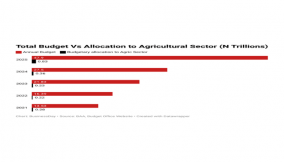

According to Nigeria’s budget document, the overall budget deficit is N9.18 trillion for 2024. This represents 3.88 percent of GDP, and the government is betting on debts (N7.83 trillion) and proceeds of privatisation (N298.49 billion) and drawdown on multilateral and bilateral loans secured for specific development projects (N1.05 trillion) to finance the deficit.

An outlook on the Nigerian fixed-income market by Comercio Partners noted that regarding foreign borrowings, the expectation is that global interest rates will remain prohibitively high in 2024.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp