Foreign Direct Investment inflows in Nigeria declined by 35.2 percent in the first quarter of 2024 as more multinationals continued to exit the country.

According to the latest capital importation report by the National Bureau of Statistics (NBS), FDI fell to $119.2 million in Q1 from $183.9 million in the previous quarter. But it rose on a year-on-year basis by 150.4 percent from $47.6 million.

The country’s harsh business environment which was worsened by the removal of petrol subsidy and naira devaluation has forced seven multinationals to exit one of Africa’s biggest economies in the last 11 months. This situation could affect the country’s $1 trillion economy target by 2030.

Direct investment reduced due to high operational rates and insecurity challenges in Nigeria which are waning investors’ confidence, said Adeola Adenikinju, president of Nigerian Economic Society (NES).

“Since the macroeconomic conditions are stifling, investors outside go for portfolio investment because it’s less risky and it allows them to quickly take away their money. But in the long term, we need FDI for a stronger economy,” Adenikinju added.

The Economics professor stated that the government needs to focus more on stabilising the economy, especially exchange rate volatility and inflation while fixing infrastructural gaps and insecurity concerns in the country.

Read also: Revamping an ailing economy through FDI

“The decline in FDI inflows to Nigeria in recent years is primarily due to a challenging macroeconomic environment, reduced investment by international oil companies, infrastructure deficits, and ongoing security challenges,” analysts at FBNQuest Capital Research said in a note on Wednesday.

The analysts noted that the government’s reforms and announcements of investment pledges might not see FDI grow immediately, “however, these commitments are anticipated to gradually translate into actual investments and yield results in the medium term”.

A breakdown of the NBS report revealed that FDI recorded the lowest of the total capital importation even as total foreign investments tripled and hit a four-year high of $3.38 billion in Q1.

Further analysis revealed that of the 36 states in the country, Lagos, FCT, and Ekiti were the ones attracted to investors with each recording $2.78 billion, $593.58 million, and $12.7 million respectively.

“Foreign Direct Investment recorded the least with $119.18 million (3.53 percent) of total capital importation in Q1,” the report stated.

“Portfolio Investment ranked top with $2,075.5 billion, accounting for 61.4 percent, followed by Other Investment with $1,181.3 billion, accounting for 34.99 percent,” it added.

“The NBS data shows an increase in Portfolio investment which is short-term liquidity. What our economy needs majorly is FDI and the exodus of multinationals in the past months must have resulted in its drop,” a developmental economist who wishes to remain anonymous said.

The source added that the government must continue to reassure investors that the country’s economic environment is viable for investments, asserting that through the government’s business-friendly policies, foreign direct investments will troop in.

Samuel Sule, chief executive officer of Renaissance Capital Africa said the drop in FDI is attributed to the exit and limited entry of direct investors into Nigeria.

He asserted that the decline will, in the long run, lead to scarce capital and less economic activity in the country.

President Bola Tinubu, who took the helm of Nigeria’s affairs in May 2023, stoked foreign investors’ interest with some of his policies including declaring an end to the costly fuel subsidy and the liberalisation of the FX.

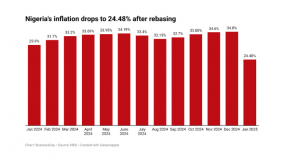

However, these reforms are yet to change the narrative of the frailing economy, instead, they worsened inflation, currently at a near three-decade high. The rising inflationary pressures have weakened the purchasing power of consumers, even as businesses grapple with higher operating costs.

In May 2024, Nigeria’s headline inflation rose for the 17th straight time to 33.95 percent up from 33.69 percent in the previous month.

BusinessDay reported on Monday that business activity in Nigeria dropped to the lowest in seven months in June 2024, according to Stanbic IBTC Bank Purchasing Managers’ Index (PMI).

Findings by BusinessDay have shown that most multinationals that are exiting Nigeria, mostly American and European companies, are being taken over by Asian companies.

Turkish firm, Hayat Kimya’s premium diaper brand, Molfix, is taking the void left by P&G’s withdrawal. Tolaram Group, a Singaporean firm, acquired Diageo’s stake in Guinness Nigeria.

A group of Nigerian investors, Renaissance Group had purchased Shell’s onshore holdings when the oil giant decided to restrict its activities to the offshore market. EnjoyCorp Limited bought Heineken’s majority stake in Champion Breweries.

Meanwhile, Segun Ajayi-Kadir, the director general of the Manufacturers Association of Nigeria (MAN) contended that the recent exit of some multinational companies from Nigeria offers a golden opportunity for homegrown manufacturers to thrive with proper government empowerment.

“I think there is a strong lesson to be learned here. The big ones leaving are the multinationals, which should send a clear signal to the government,” he stated in a recent media chat.

“We need to be strategic in what we promote. That is why we say the foreign direct investment is excellent, but it should come secondary to empowering the local investor, the existing manufacturers because that is what is enduring.”

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp