Nigeria’s economy grew at its slowest pace in 15 months in the third quarter as the oil and manufacturing sectors shrank amid mounting woes.

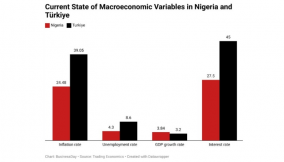

The country’s Gross Domestic Product (GDP) grew by 2.25 percent (year-on-year) in real terms in Q3 2022, down from 3.54 percent in Q2 and 4.03 percent in the same period last year, according to data released by the National Bureau of Statistics (NBS) on Thursday.

“The reduction in growth is attributable to the base effects of the recession and the challenging economic conditions that have impeded productive activities,” the NBS said.

“However, quarter-on-quarter, real GDP grew at 9.68 percent in Q3 2022, reflecting a higher economic activity in Q3 2022 than the preceding quarter. In the quarter under review, aggregate GDP stood at N52,255,809.62 million in nominal terms,” it added.

Analysts say the inability of the Nigerian economy to sustain the growth momentum in Q1 and Q2 of this year indicates that the economic performance in the last quarter and the first quarter of 2023 might not be different from what was recorded in Q3.

The crude oil and gas sector shrank by 22.67 percent in Q3, compared to 11.77 percent in the previous quarter on the back of low production occasioned by theft and vandalism.

The manufacturing sector was hobbled by foreign exchange challenges, high energy costs and high cost of capital owing to interest rate hikes. It contracted by 1.91 percent in Q3 for the first time since Q4 2020, when the country managed to emerge from the COVID-19-induced recession.

“We have started seeing the impact of production costs on manufacturing output – elevated energy costs, currency pressures, and higher interest rates. So it’s not surprising that the manufacturing sector declined in Q3, although base effects also underpinned the contraction seen during the period,” Abdulazeez Kuranga, a macroeconomist with Cordros Securities, said.

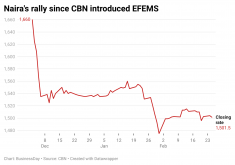

The surge in diesel prices and the further depreciation of the naira against the dollar pushed up manufacturers’ operating costs.

“In Q3, the manufacturing sector turned from a major driver to a drag on the headline growth rate. Following the growth of 3.2 percent y/y in Q2, manufacturing GDP fell by 1.8 percent y/y last quarter,” Capital Economics, a London-based economic research firm, said.

It said the services industries posted robust growth, which prevented the headline rate from slowing even more sharply. “GDP in the finance and insurance sector rose by 12.7 percent y/y, and the equivalent figures for the ICT and the trade sectors were also strong, at 10.5 percent y/y and 5.1 percent y/y, respectively,”

The agricultural sector contributed 29.67 percent to GDP in Q3, up from 23.24 percent in Q2 and 22.36 percent in Q1. The sector grew by 1.34 percent in real terms, compared to 1.20 percent in Q2 and 3.16 percent in Q1.

Industries contributed 18.37 percent to GDP, lower than 19.40 percent as of Q2 and 21.47 percent in Q1, while the services sector contributed 51.96 percent as against 57.35 percent in Q2 and 56.17 percent in Q1.

Read also: Experts say Nigeria’s economy needs national policy, technological transfer to scale up investment

The nation’s transport and storage subsector recorded the highest real growth rate of 41.59 percent, contributed mainly by the growth in the road transport subsector. Water transportation saw a boost as its real GDP grew by 19.48 percent while air transport recorded 14.58 percent real growth.

Other sectors that recorded double-digit real growth rates include quarrying and other minerals, 39.61 percent; metal ores, 36.24 percent; motion pictures, 22.41 percent; water transportation, 19.48 percent, among others.

“We don’t expect GDP growth to pick up markedly over the coming quarters. Admittedly, fiscal loosening ahead of the elections in February is likely to support demand. But we suspect that will prove insufficient to lift the economy as a whole in the face of mounting headwinds,” Capital Economics said.

It added that the woes in the oil industry are not likely to ease anytime soon even as it is projected that international crude oil prices could begin to slide while distortionary FX policy and demonetisation will weigh down on the manufacturing sector.

“While the latest figures mean that growth in 2022 will come in a bit stronger than we had previously anticipated, we still think that a sharp slowdown in 2023 is on the cards,” Capital Economics added.

“For Q4, we expect growth to be at current Q3 levels as the October flooding will impact Q4 agric output, manufacturing should grow primarily due to favourable base effects, and services expected to maintain its momentum, albeit slowly,” Kuranga said.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp