…Liquidity ratio more than double CBN benchmark

…. Excess liquidity outpaces lending to businesses

A Nigerian creative entrepreneur spent months knocking on the doors of banks in search of financing to grow her business. One after another, lenders turned her away until she finally found one willing to take a chance on her.

“I refused to take no as an answer, and I fought all the banks until I found the bank that supported me,” she recalled. “I built my business case, I built my personal brand, I built a product they could not ignore, and they were forced to give me money when I needed money.”

Her experience mirrors the reality facing many Nigerian businesses, particularly small and medium-sized enterprises, which continue to struggle to access bank credit despite lenders sitting on their strongest liquidity position, following a successful regulatory-imposed recapitalisation exercise in March.

The banks successfully raised N4.7 trillion ($3.4 billion) in fresh capital, but the gains of the capital raise are lost on the small businesses that power the economy of Africa’s most populous nation.

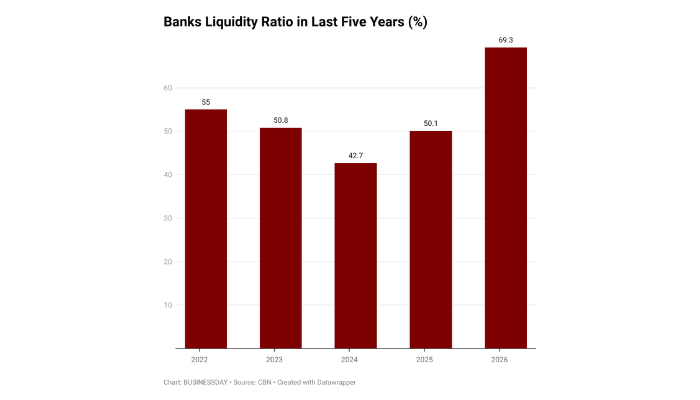

Latest data from the Central Bank of Nigeria (CBN) showed the banking sector’s liquidity ratio climbed to a record 69.27 percent in February 2026, more than double the regulatory minimum of 30 percent and the highest level ever recorded. The last time the liquidity ratio was this high was in 2012 when it stood at 68 percent.

The latest figure represents a sharp increase from 50.09 percent in February 2025, 42.66 percent in February 2024, 50.80 percent in February 2023 and 55.0 percent in February 2022, highlighting the rapid accumulation of liquid assets across the banking industry.

While the stronger liquidity position underscores the resilience of Nigeria’s banking sector and its ability to withstand funding pressures, economists say it also reflects banks’ growing preference for investing in Treasury bills, Open Market Operation (OMO) bills and Federal Government bonds rather than extending credit to businesses, where the risks are significantly higher.

According to Muda Yusuf, chief executive officer of the Centre for the Promotion of Private Enterprise (CPPE), the liquidity ratio does not mean banks are holding unusually large volumes of cash.

“It is important to clarify that when we talk about the liquidity ratio, we are not referring only to cash. Cash is just a small fraction of the liquid assets that banks hold.

“Treasury bills, for instance, are classified as liquid assets. My suspicion is that banks are currently holding more Treasury bills because the yields have been very attractive. Over time, they have also increased their investments in government bonds for the same reason.

“Rather than extend credit to businesses, where the risks are much higher, many banks appear to prefer investing in Treasury bills, OMO bills and Federal Government bonds. These instruments offer relatively high returns with much lower risk.

“I believe this preference for government securities may explain the high level of liquidity. The liquidity is not necessarily in cash but in other liquid assets held by the banks.”

As Muda Yusuf explained, the liquidity ratio includes Treasury bills and other liquid assets, not just cash.

The liquidity ratio measures banks’ ability to meet short-term obligations using liquid assets such as cash, Treasury bills and government securities. The CBN requires commercial banks to maintain a minimum liquidity ratio of 30 percent. At 69.27 percent, the industry’s liquidity position is more than twice the regulatory benchmark, underscoring the resilience of the banking sector but also raising concerns about weak financial intermediation.

The stronger liquidity position comes at a time when many businesses, particularly small and medium-sized enterprises, continue to complain of limited access to bank credit despite easing monetary conditions. Faced with lending rates that remain elevated and stringent credit conditions, many firms say financing expansion has become increasingly difficult.

Banks continue to earn attractive risk-free returns from government debt instruments while lending to the private sector remains constrained by high credit risk and elevated borrowing costs. CBN data showed banks’ maximum lending rate stood at 34.78 percent in May 2026, while the prime lending rate was 19.10 percent.

The apex bank continued to actively manage liquidity during February through Open Market Operations. It offered N1.80 trillion worth of CBN bills, while subscriptions reached N6.35 trillion and allotments stood at N4.77 trillion at an average stop rate of 20.42 percent. Following maturities of N4.62 trillion, the operations resulted in a net liquidity withdrawal of N150 billion.

The Federal Government also sustained its domestic borrowing programme through Treasury bills and bond issuances. Treasury bill subscriptions remained robust, while investors also showed strong appetite for reopened seven-year, nine-year and 10-year Federal Government bonds, reflecting continued demand for sovereign securities.

Despite the CBN’s liquidity management operations, banking system liquidity strengthened further. Average system liquidity rose by 23.69 percent to N3.08 trillion in February from N2.49 trillion in January, supported by fiscal injections, maturing Treasury bills and FGN bonds, Remita inflows and foreign exchange sales.

The improved liquidity was reflected in banks’ use of the CBN’s standing facilities. Placements at the Standing Deposit Facility rose to N61.07 trillion during the month from N50.69 trillion in January, while requests at the Standing Lending Facility dropped sharply to N0.25 trillion from N1.87 trillion, indicating that banks relied less on the CBN for short-term funding.

Ayodele Akinwunmi, chief economist at United Capital, said maintaining strong liquidity enables banks to strengthen their financial position, meet customers’ daily funding needs, comply with regulatory requirements and take advantage of emerging business opportunities. He added that adequate liquidity also enhances the sector’s ability to withstand economic shocks and preserve long-term financial stability.

However, the Financial Markets Dealers Association (FMDA) noted that stronger liquidity and improved foreign exchange inflows have yet to translate into stronger lending to the productive sector, suggesting that banks remain cautious in extending new credit.

That caution was evident in the latest CBN credit data. Private sector credit rose by just 0.57 percent to N81.04 trillion in May, indicating that businesses remained reluctant or unable to take on fresh debt despite the CBN’s earlier monetary easing. In contrast, credit to the government increased by 1.97 percent to N40.38 trillion as public sector borrowing continued to absorb available liquidity.

Members of the Monetary Policy Committee have also highlighted the disconnect between the banking sector’s robust liquidity and weak credit expansion.

In his personal statement after the committee’s May meeting, Bandele A.G. Amoo said the banking system remained sound, with liquidity and capital adequacy ratios comfortably above regulatory thresholds. He, however, expressed concern that credit intermediation remained suboptimal, limiting financing to key productive sectors of the economy.

Another MPC member, Raymond O. Omachi, said the financial system remained resilient and well positioned to support the government’s domestic borrowing programme. He added that the ongoing bank recapitalisation exercise would further strengthen market stability and enhance banks’ capacity to finance economic growth.

Yusuf also expressed confidence in the outlook for Nigeria’s financial markets, citing stronger bank capitalisation, improved corporate earnings, enhanced regulatory oversight and sustained institutional participation. He added that improved domestic refining capacity and higher crude oil production should support fiscal revenues, foreign exchange earnings and overall macroeconomic stability.

At its May 2026 meeting, the MPC retained the Monetary Policy Rate at 26.5 percent, while leaving the asymmetric corridor at +50/-450 basis points. The committee also retained the Cash Reserve Requirement at 45.00 percent for Deposit Money Banks, 16.00 percent for Merchant Banks and 75.00 percent for non-Treasury Single Account public sector deposits.

Olayemi Cardoso, governor of the CBN, said the committee’s decision reflected its assessment that recent inflationary pressures were largely driven by temporary external shocks and that existing policy settings remained appropriate to sustain the disinflation process.

Supporting that position, MPC member Aku Pauline Odinkemelu said maintaining current policy settings would allow previous policy actions to continue working through the economy while preserving the CBN’s inflation-fighting credibility. She added that the combination of high reserve requirements and the apex bank’s liquidity management framework would continue to anchor banking system liquidity and safeguard financial stability.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp