If you ask the average Nigerian about his or her understanding of infrastructure, you are likely to get a response that depicts something tangible,like airports, railways, roads, etc. This is not wrong; however, it is not exhaustive.

By definition, Infrastructure is the underlying systems and services, such as transport and power supplies, that a country or organization uses in order to work effectively. In short, infrastructure is the bedrock of any economy – it is just as hard to imagine traveling from Lagos to London without an airport (physical infrastructure), as it is to imagine civilization without laws and regulation (intangible infrastructure).

Financial services play a key role in economic growth: one cannot emphasize how important it is that scarce resources are channeled to its most efficient use, or the role of banking plays in economic prosperity. But what is the current state of Nigerian banks? Banks stay profitable mostly by fees and commissions, and income from investment securities rather than their core business, lending.

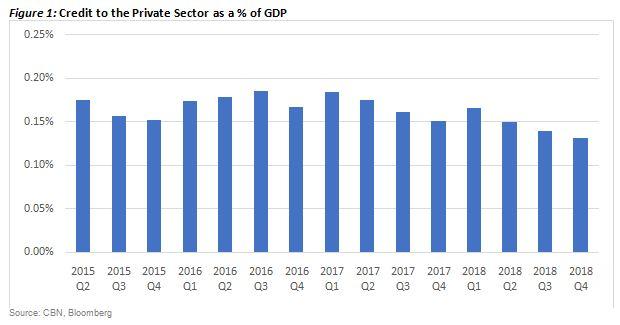

Persistent negative loan growth, and a corporate-concentrated loan book, for most banks, suggests that credit needed for economic expansion is not being extended to you and me, the everyday person, seeking capital to foster business and entrepreneurship. Figure 1 shows that credit (when considered as a percentage of GDP) to the private sector in recent times has been meager.

To some extent, it is hard to blame the banks; only just recovering from an industry plagued by poor asset quality and non-performing loans, most bankers play safe by extending risk-free investments to the Federal Government at high double-digits interest rates while they shy away from creating risk-assets. You have to ponder: what can be done to address this? First, let’s consider the opportunities that lie in the Nigerian retail loan market.

How big can retail lending be?

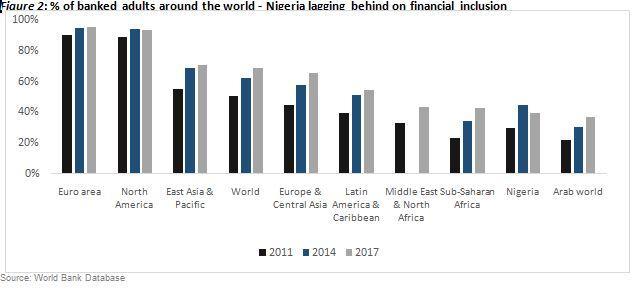

In the United States of America, the retail market is estimated US$1.49 trillion in a US$19.3tn economy. Using the same inference for Nigeria, with an economy a fifth of the US (US$375bn), we can extrapolate about $28bn or approximatelyN10.2tn. This is a quick and rough estimate. Of course, some form of country discount will have to be applied to this number as most Nigerians have no access to banking and financial services, see Figure 2. However, it shows the potential of Nigeria’s retail loan market if things can be done right.

As I said earlier, lenders hedge credit risks by lending to few big reputable corporates and invest the rest of their liquidity in risk-free fixed income instruments. This means most individual borrowers are denied credit.

If you have ever tried to secure a loan from your bank for business, then you probably know that most, if not all banks, require an arm, a leg and one of your kidneys before they are comfortable giving a line of credit to individuals. But this should not be the case in an ideal, business-friendly, and growing economy.

In a nutshell, banks are generally averse to lending to individuals and SMEs without an established reputation. The reason is simple: just the way the cost of power (fueling and maintaining a generator) is a massive headache to most businesses, the cost of due diligence, credit assessment, and setting up legal checks for unsecured lending make unrealistically expensive sense to banks – this is the bane of consumer lending.

The government has failed to change this paradigm in many ways. On the one hand, the FGN crowds out private sector credit by persistently offering juices yields to local financial institutions. Secondly, and more importantly, our government has failed to set up the infrastructure needed to facilitate unsecured lending; especially a legal system to protect lenders and borrowers.

How can this be done?

It would be helpful for the CBN and the banks, to work closely with legal professionals, to take responsibility of fixing this challenge by developing a framework for retail, SME lending and loan recovery within the scope of their existing regulatory capabilities.

I dare say that our problems have already been partially solved with the introduction of the Bank Verification Number (BVN). The BVN is a unique identifier that links an individual’s bank accounts together and stores your personal and biometric data; think of it like a Social Security Number used in the US, but apparently not yet as elaborate.It is an elegant and modern identity infrastructure that has leapfrogged the Nigerian banking from rudimentary to top-class in just a few years.

This framework should serve as the legal backbone for lending, such that there is appropriate recompense for anyone who does not pay his loans as at when due.

Imagine that whenever a customer takes a loan and does not pay back as at when due, the lender is required to contact the customer and specify a grace period, perhaps three months, within which the borrower is to fulfill their outstanding obligation else they would be reported to a national registry of defaulters. Of course, banks must show evidence of this notice to the registry periodically.

This is expected to prompt the borrower to pay back his outstanding loans before the grace period elapses. If within the grace period the customer pays back, all well and right between the lender and borrower.

However, if the debt extends beyond this period, more aggressive measures will kick in. The bank will push the data to the national registry which will then act on it with an automated warning with details of the consequences should the borrower fail to oblige. Punishment for defaulters will include preventing all of the debtor’s bank accounts from any further debits – this will also apply to guarantors of defaulters.

Apparently, this will involve more details and a lot of fine tuning – we will also need a quick and reliable credit rating/scoring system – but it presents a possible view of how we can get the banks more comfortable with retail lending.

Furthermore, a lot needs to be done by the CBN and banks to ensure that potential borrowers are well informed about the benefits of taking loans and the consequences should they default. We recommend a campaign through various media platforms/outlets – analog and digital.

How could this impact the economy?

The potential cash injection to the retail and SME sectors will promote entrepreneurship, increase retail consumption which will subsequently drive manufacturing, wholesale, and retail distribution, etc.

There will also be the increased rate at which money changes hands (velocity of money) which ensures improved cash flow for many businesses– this increased value will grow jobs, reduce unemployment and slowly pull many of the populace out of poverty.

We all complain about that lousy road or local travel experience, or the lack of a rail system in a megacity like Lagos – this is valid and genuine issues regarding our infrastructure. But I don’t hear as much noise about how difficult it is to get a loan to start a business. Maybe we aren’t just looking at things right.

Nigerians are a vibrant bunch of, full of ideas and entrepreneurial spirit (just look at the amazing leaps of the entertainment industry), and all that we need is a system that will give the required platform to showcase this to the world.

As I said earlier, lenders hedge credit risks by lending to few big reputable corporates and invest the rest of their liquidity in risk-free fixed income instruments. This means most individual borrowers are denied credit.

If you have ever tried to secure a loan from your bank for business, then you probably know that most, if not all banks, require an arm, a leg and one of your kidneys before they are comfortable giving a line of credit to individuals.But this should not be the case in an ideal, business-friendly, and growing economy.

In a nutshell, banks are generally averse to lending to individuals and SMEs without an established reputation. The reason is simple: just the way the cost of power (fueling and maintaining a generator) is a massive headache to most businesses, the cost of due diligence, credit assessment, and setting up legal checks for unsecured lending make unrealistically expensive sense to banks – this is the bane of consumer lending.

The government has failed to change this paradigm in many ways. On the one hand, the FGN crowds out private sector credit by persistently offering juices yields to local financial institutions. Secondly, and more importantly, our government has failed to set up the infrastructure needed to facilitate unsecured lending; especially a legal system to protect lenders and borrowers.

(This article is written by Adedeji Olowe, CEO of Trium Networks Limited and Babatunde Makanjuola, Coronation Merchant Bank Limited)

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp