Shareholders of Union Bank now have every reason to smile after a long wait to spanning 11 years for cash rewards on their investment following the announcement of a proposed dividend of 25kobo per 50k share for 2019 financial year ended 31 December.

Analysis of the recently released result shows that gross earnings grew 14.4percent to ₦166.5bn compared to ₦145.5bn recorded in full-year 2018, on the back of an increase in earning assets, Interest income was up 11percent to ₦117.07bn compared to ₦105.2bn in full–year 2018. Driven by growth in fees and commission income as well as recoveries, Non-interest income surged 24.7percent to ₦42.8bn against ₦34.3bn recorded in 2018. Profit after Tax surged 9.8percent to N19.87billion from N18.09billion.

During the period under review, gross loans increased 20percent to ₦595.3bn from ₦496.8bn in December 2018, customer deposits was up 5percent to ₦886.3bn from ₦844.4bn in December 2018.

Active users on Union Bank’s enhanced mobile and online banking platforms increased 60percent and 42percent- 2.1 million and 1.3 million users respectively. Coupled with increasing efficiency and growth in its traditional channels (e.g. ATM, POS), e-business income grew by 64percent to ₦7.7bn in 2019 from ₦4.7bn in 2018.

In line with the bank’s 2019 guidance, its non-performing loan ratio went down to 5.8percent from 7.8percent as at December 2018, while the capital adequacy ratio (CAR) remains well above the regulatory threshold at 19.7percent.

Union Bank raised N30billion bond program, the largest 10-year bond ever issued by a corporate institution in Nigeria. The ₦30bn Tier 2 bond was fully subscribed from the Nigerian capital market. The bank working in partnership with Atlas Mara, secured $200 million in funding from the US Development Finance Corporation (DFC) previously called OPIC, one of the largest investments made by the DFC in a financial institution in Nigeria and sub-Saharan Africa to date, for investments over the next ten years in digitization, on-lending to SMEs and funding for αlpher, women banking proposition.

In a bid to drive cost optimization and ensure optimal operational efficiency, the bank introduced the Long Term Efficiency Acceleration (LEAP) Programme, this has saved the bank N2.4bn in recurring expenses helping drive overall cost down notwithstanding double-digit inflation and an increase in nondiscretionary cost.

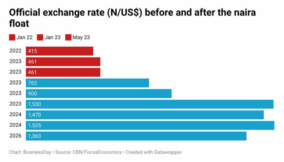

Since the 2005 recapitalization exercise, Nigerian banks have continued to face an uphill task of meeting series of tough regulations from the Central Bank of Nigeria (CBN) coupled with weak macro-economic with revenue and bottomline coming under intense pressure.

The tier-2 lender in January announced it has entered a share sale and purchase agreement to divest its 100percent equity stake in its UK subsidiary. According to the management of the bank, this is to align with Union Bank’s strategy to geographically streamline its business operations to focus on growth opportunities in Nigeria.

“Following a competitive bid process, MBU BidCo Limited, an acquisition vehicle wholly owned by MBU Capital Limited, was selected as the preferred bidder,” the bank said in a notice.

The completion of the sale is subject to regulatory approvals from the relevant regulatory authorities in Nigeria and the United Kingdom.

Taking advantage of the currently low-interest rate in the debt market and following the successful registration of its N100 billion Commercial Paper Programme in 2018, Union Bank announced the commencement of its series 3 and 4 CP issuance. The offer closed on January 21, 2020, with a target issuance size of N20 billion across 180-day and 268-day tenors. The CP offer was targeted at institutional investors including pension and non-pension asset managers, as well as eligible high net-worth investors.

Industry laden with regulatory landmines

Nigerian banks’ current regulatory crises have their roots in the 2014 oil price crash. The resultant pressure on government revenues that led to the CBN being called upon to fund the deficit (CBN overdrafts to the federal government of Nigeria [FG] ballooned 10x between May 2015 and September 2019), the CBN maintained a fixed FX stance despite underlying depreciation pressure, it has significantly scaled up its OMO issuance programme to attract more foreign investors and mop up liquidity. 56percent of the growth in CBN liabilities between January 2016 and September 2019 was driven by CBN bills – mainly OMOs, CBN bill issuances, of which OMOs are now 73percent, have grown 5x between May 2015 and September 2019, while imposing increasingly higher cash reserves on the banks, which provides the CBN with zero-cost funding to help offset the high and rising cost of FX defence.

Also the slew of 2019-2020 regulations that have forced the banks to achieve a higher loan-to-deposit ratio pushed local private and institutional investors out of the OMO market, and hiked the cash reserve ratio (CRR) to 27.5percent, have enabled the CBN to raise even more zero-cost funding from the banks. This helps to not only support FGN lending, but also, according to the banks, multiple CBN development finance initiatives targeted at different sectors. Thus, the banks are likely to continue to bear the cost of macro stability.

Outlook

Going forward, the challenge for Nigerian banks such as Union Bank would be to deliver sustainable growth and good return on investment for shareholders amid the difficult macro-economic and tough regulations. To mitigate these risks, analysts have urged banks to build low-cost business models to penetrate the bottom of the pyramid.

According to the World Bank, half of all Nigerians work in the agriculture sector, while half of the people working in agriculture belong to the poorest 40percent of the population and 64percent of all poor lived in rural areas and 52percent of the rural population lived below the poverty line in 2016. This implies that growth benefits from the bottom of the pyramid cannot happen while ignoring the agricultural sector and rural areas, a low-cost business model can successfully crack this space at scale.

Banks can also evolve to a holding company model with sizeable subsidiaries in fast-growth sectors.

This in addition to giving Nigerian banks a route to explore earnings growth outside of the challenging banking sector, it would serve as a room to explore cross-selling opportunities across a larger group, one key benefit to investors from a bank adopting this structure is the earnings see-through it gives.

It allows investors to value the group on a sum of the parts (SoTP) basis. Scale growth in extant operations outside Nigeria.

Over the past few years, Nigerian banks have spread their networks to a wide range of countries, much to investors’ disappointment. However, scale achievements in some locations appear to finally be yielding meaningful fruit at group level. Scale is not only critical to returns delivery but if a niche or non-banking business line, scale within that vertical is equally important.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp