Recently, I was opportune to listen to a presentation titled “Nigeria’s Economic Prospects” by one of Nigeria’s foremost Economists, Dr Ayo Teriba. He articulated Nigeria’s current economic woes and situated them in the global context of the Post COVID era, European geopolitical tensions, and the resulting energy and commodity price crises. His overarching arguments and postulations are not only germane for a rethink of Nigeria’s economic trajectory but also a breath of fresh air in the current discussions on restructuring Nigeria’s economy for growth and prosperity.

This essay and a series of others to follow result from the need to rethink our economic structure for productivity, in line with the global trend and current realities and not leave our economy to be decided by happenchance and outdated political economy theories, reminiscent of the industrial revolution era instead of the knowledge economy built more on innovation, than on production.

Three of the leading presidential candidates for the 2023 general elections are talking of increasing productivity and export as the critical drivers of economic growth. A review of their economic thinking shows that they all believe Nigeria should engage in more agricultural and manufacturing production for internal consumption, import substitution and export.

They emphasise production and the resultant increase in productivity and employment of human and natural resources as the blueprint for Nigeria’s economic growth. As simplistic and direct as this economic thinking is, the existing economic structure and the ones proposed by the presidential candidates are insufficient to put Nigeria on a growth trajectory.

Presidential candidates need to tell us more about how they plan to incentivise innovation to unlock growth in both income and wealth

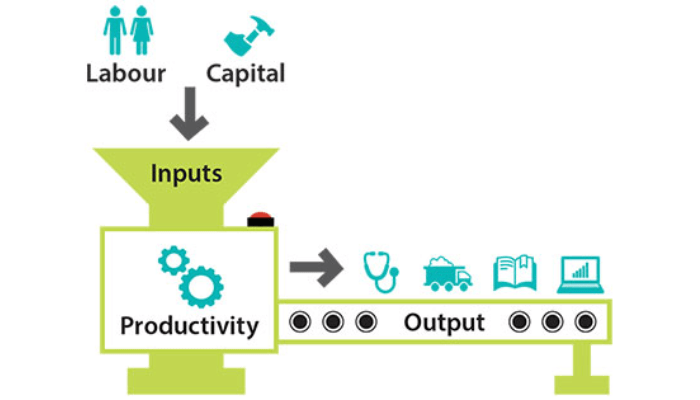

Nigeria must leapfrog industrialisation and connect with global innovation and financialization trends to succeed. Financialization is eclipsing industrialization. Financialization, according to Thomas Polley of the Levy Economics Institute, refers to a process whereby financial markets and institutions gain greater influence over economic policy and outcomes. Productivity in the post- industrial economy goes beyond income-centric optimization of production transactions for largest margins from local and foreign sales that was the hallmark of the earlier stages of industrialization. It is now much more about wealth- centric optimization of tangible and intangible asset portfolios for maximum balance sheet values that is the hallmark of financialization.

The world has moved away from the past in which global commodity prices (crude oil inclusive) dictated the pace of growth of items on income statements into a new reality in which global equity prices play the bigger role of dictating the pace of wealth growth on balance sheets. Global wealth has been growing much faster than global income since 2000, and this trend is largely expected to continue in the foreseeable future.

The mixed outlook of the two global asset prices over the next half- decade underpins those expectations. The IMF projects that commodity prices, including crude oil, currently elevated by geopolitical tensions will fall steadily back to 2021 levels from 2023 to 2027, while we expect equity prices to continue the solid upward trajectory in the last decade through 2027.

If the asset prices follow the projected paths, global exports could rise by about 50 per cent from US$22.4 trillion in 2020 to US$33.1 trillion by 2027, while FDI stocks could surge twofold from US$41 trillion in 2020 to US$79 trillion by 2027. Over the medium-term balance sheet gains look set to remain three to four times as large as income statement gains.

It is in this context that it becomes more important for the presidential candidates to say more about what they plan to do about getting a fair share of the growing global pie of global FDI stock into idle public assets in Nigeria that spread across corporate, real estate, and infrastructure.

We now must define productivity to include innovations that optimizes asset portfolios in addition to those that optimizes output transactions. The transaction model of productivity relies on the quantity and quality of goods and services produced and the revenue generated through internal consumption and export. Global trends now transcend this by embracing asset productivity. Optimizing assets involves unlocking liquidity from publicly owned place-based, space-based, and skill- based assets littered across corporate, real estate, and infrastructure sectors.

So, instead of relying solely on products and income from agriculture, industry, and service, we should go after the place-based, space-based, and skill-based assets that are needed to generate output in these production-based sectors. Government should allow the inflow of FDI into the innovation sectors of the economy that the productive sector rely on to thrive. We see this in Nigeria’s Fintech sector, where small and medium industries attract billions of dollars as FDI. The government should collaborate with the private sector to open other innovation sectors for FDI.

Read also: Africa can attract investments on back of AfCFTA – VPs, PMs assure

Saudi Arabia exemplifies this trend. The country has historically focused on creating wealth through income-centric optimization production and exports, not caring much about creating wealth through optimization of asset portfolios. But the weakening of global commodity prices since 2014 in the face of strengthening global equity prices prompted the country to take steps to financialize its public asset portfolio from 2016.

It was in this process that it listed ARAMCO in the market through an initial public offering in 2019. The market value of ARAMCO is more than $2 trillion now, making it one of the biggest companies in the world. Considering that Saudi Arabia’s GDP is only about US$850 billion now, it is fair to say that Saudi Arabia’s balance sheet now contributes more to its national wealth and net worth than its income statement.

We can also see this with American technological behemoth, Apple. It takes direct control of the upstream/conception and downstream/distribution phases of its value chain where its growing stock of tangible and intangible skill-based, and space-based assets (including patents, brands, creative designs, and it’s closed digital marketing platform) differentiates its offerings but outsources the midstream assembling/production stages of its devices, where operating procedures are hard to differentiate, to third parties offshore. Apple is worth over $2 trillion.

The next is the place-based optimisation. All stakeholders must unlock liquidity by optimising the market value of public spaces, real estate, cities, transit routes, tourist centres, farms, factories, and other physical capital. Government should review its real estate holdings to unlock the liquid value attached to them. It may make sense to commercialise real estate with substantial commercial value due to its location rather than keeping them as government buildings serving a need that count for less.

For example, the British government moved prisons from inner cities across the UK to more economic locations and repurposed the old sites for redevelopment into luxury residential or commercial real estate as part of their efforts to get the best value from public real estate portfolio.

Dubai is another example. It developed its real estate market, tourism, and business centres to attract people from around the world to visit, work and live in Dubai. Optimization of Dubai’s portfolio of place- based assets contributes more to its wealth and net worth than producing and exporting oil. Unlocking the value in place by Amenitizing leisure and leisure activities is essential.

Optimising spaces also fuels productivity. Companies obtain ownership rights, patents, licenses, connectivity, digital platforms that create significant values for other producers and consumers. Companies like Google, Facebook, Airbnb, Uber are owners of space-based assets that others who wish to produce, sell, or buy cannot do without. They are multi-trillion- dollar companies in equity value and generate huge revenues from the financialization of their spaced-based assets.

Likewise, optimising skills and knowledge development is an excellent part of productivity. Global skill shortage is fuelling an unprecedented wave of talent migration. The Philippines is a leading supplier of seafarers, caregivers, and domestic workers in the world. The culinary skills of the Chinese help to differentiate Chinese restaurants worldwide. We can debate whether diners are paying a premium for the skills or for the products.

The need for healthcare workers in developed countries is an opportunity to train and export the skills of Nigerian youths to the rest of the world, so also ICT skills .Investors worldwide highly value skills, brands, trademarks, recipes, talents, innovations, and knowledge.

There is a need for rethinking productivity in Nigeria. The presidential candidates should not only understand the problems of Nigeria and how to solve them, but they should have a sharp vision of the destination they are taking Nigeria to. According to Seneca the Younger, ‘If a man knows not to which port he sails no wind is favourable’. The February 1887 Magazine of American History teaches that ‘You cannot make much of a wind, but you can choose a wind, trim your sails to it, and attain the haven you select by its push and inspiration”.

Presidential candidates need to tell us more about how they plan to incentivise innovation to unlock growth in both income and wealth. Innovation is a crucial enabler of productivity. Innovation and productivity drive living standards. The capacity to generate innovations is the defining factor of productivity, not necessarily the goods you produce.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp