Safeguarding Fintech Platforms against security breaches.

In order to ensure the safety of our fintech platforms in Nigeria, we need to “Align digital payment innovation with proactive security investment: Regulators and financial institutions must implement integrated real-time monitoring, enforce automated AML compliance, and coordinate cross-institution intelligence sharing to ensure that rapid fintech growth does not outpace fraud prevention capabilities.”

“Nigeria’s digital payments boom is accelerating financial access and efficiency, but rising fraud risks expose critical weaknesses in security frameworks. As transaction volumes surge, the real challenge is whether safeguards can keep pace with innovation.”

Pacing ahead of most African counterparts, Nigeria’s digital payment network continues to grow rapidly. Across urban centres and smaller towns, mobile money agents provide essential financial services. Fintech platforms process millions of transactions daily, reflecting high adoption driven by central bank initiatives such as the cashless policy (CBN, 2024).

Efficiencies achieved in the financial ecosystem.

Deepening participation in the financial system has improved significantly. Greater financial inclusion has been achieved. Transactions are faster, collections are more efficient, and businesses benefit from streamlined payment systems. However, this rapid expansion has also exposed new vulnerabilities. Industry data shows that by 2024, banking sector fraud losses exceeded ₦52 billion, with online channels accounting for over ₦13 billion despite fewer reported incidents, according to figures released by the Nigeria Deposit Insurance Corporation (NDIC). Each case underscores the scale of systemic risk within the ecosystem and represents a significant financial burden, highlighting systemic vulnerabilities.

Nigeria’s digital payment network continues to expand rapidly, outpacing many of its African peers. Across urban centres and smaller towns, mobile money agents now provide essential financial services, while fintech platforms process millions of transactions daily. This growth has been driven in part by policy direction from the Central Bank of Nigeria, particularly its push toward a cashless economy.

The central challenge has shifted. Adoption alone is no longer sufficient; security frameworks must evolve to keep pace with new transaction methods and digital products.

Navigating the Nigerian digital payment system.

Electronic payment volumes increased more than 300% between 2019 and 2023, with the Nigeria Inter-Bank Settlement System processing trillions of naira monthly (CBN, 2024). Such volumes place immense pressure on existing control mechanisms. Without proportional investment in monitoring and risk management, payment systems expand faster than fraud prevention capabilities. This imbalance has contributed to rising financial losses in recent years.

Fintech firms play a critical role in broadening access to formal financial services. Digital wallets, agency banking, and mobile applications facilitate real-time transactions and economic activity across sectors. However, compliance frameworks often lag behind product deployment, introducing vulnerabilities within the ecosystem. Fraud is no longer limited to ATMs or branch access; it now occurs across mobile devices, applications, and online platforms (EFCC, 2024).

The Growth of Fintech Firms: Evolution of smarter financial technology.

Fintech firms have played a central role in expanding access to financial services. Digital wallets, agency banking, and mobile applications have brought millions into the formal financial system.

Speed and convenience drive adoption. Customers move funds instantly. Businesses settle transactions in real time. These improvements support economic activity across sectors. However, rapid expansion introduces risk. New entrants often scale faster than their control systems. In some cases, compliance frameworks lag behind product deployment. This creates vulnerabilities within the ecosystem.

The shift from traditional banking channels to digital platforms has also changed fraud patterns. Fraud is no longer limited to physical access points. It now occurs across mobile devices, applications, and online platforms.

Complexities of banking fraud in Nigeria.

Nigeria’s banking fraud has evolved from ATM card cloning to sophisticated social engineering tactics. Chip and PIN technology reduced card cloning, but fraudsters now manipulate customers into authorising transactions, exploiting human behaviour rather than system failures. SIM swap fraud, insider compromise, and authorised push payment scams are rising, targeting identity verification gaps. Data reveals fewer reported cases but significantly higher financial losses, indicating more targeted, valuable attacks. Cross-border networks add complexity, with foreign actors collaborating locally, complicating investigations and recovery.

Regulatory authorities have introduced several measures to strengthen fraud prevention. The Central Bank of Nigeria now requires financial institutions to take greater responsibility for certain categories of fraud, including authorised push payment transactions. In addition, stricter timelines for incident reporting and resolution have been implemented, alongside a transition toward automated anti-money laundering systems that support real-time monitoring and reporting.

The Nigeria Electronic Fraud Forum continues to play a coordinating role by promoting shared standards, centralised reporting, and industry-wide intelligence on suspicious activities.

Understanding the available Fraud prevention frameworks.

Nigeria’s Central Bank has strengthened fraud prevention through three key reforms. First, banks now share liability for authorised push payment fraud, creating stronger customer protection incentives. Second, mandatory timelines require prompt incident reporting and resolution. Third, automated Anti-Money Laundering systems replace manual processes, enabling real-time transaction monitoring, identity verification, and automatic suspicious activity reporting. The Nigeria Electronic Fraud Forum further supports industry coordination through shared standards, centralised reporting, and databases identifying suspicious individuals.

The evolution of financial risk management.

Financial risk management in Nigeria is shifting toward integrated systems. Institutions are expected to monitor risk across all channels in real time. This approach requires alignment between compliance systems, customer data, and transaction monitoring tools. Standalone systems are no longer effective in a high-volume digital environment.

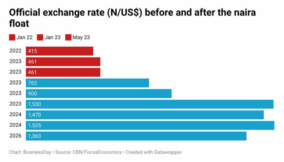

The image below shows the contrast between systems with weak controls and those with stronger risk management frameworks:

Institutions that operate with integrated systems detect fraud earlier and reduce losses. Those with fragmented systems remain exposed.

Governance and internal control gaps

Despite regulatory progress, internal control failures persist. Some institutions process transactions for non-compliant companies, creating entry points for fraud. Insider threats remain a concern, as employees with system access may bypass controls. Effective governance requires consistent enforcement of compliance and active, independent internal audit functions (NDIC, 2024).

Bridging the security gap

Nigeria’s reported fraud losses decreased notably in 2025, even as transaction volumes grew, suggesting that targeted interventions are having an effect. Strengthening the security framework across financial institutions remains critical. Real-time transaction monitoring, automated anomaly detection, and compliance enforcement tools are essential to identify suspicious activity and ensure adherence to Central Bank directives. Despite technological improvements, internet banking and digital commerce remain vulnerable to exploitation. Social engineering schemes continue to challenge institutions, highlighting the importance of continuous customer awareness campaigns. Regulatory requirements now emphasise ongoing education, multi-channel reporting, and cross-institution collaboration. Establishing a central alert system would improve industry-wide information sharing, allowing banks and fintechs to respond faster to emerging threats and prevent repeat attacks.

Emerging Threats in Nigeria’s Fintech Landscape.

As Nigeria’s fintech ecosystem expands, new vulnerabilities emerge alongside innovative services. Mobile banking apps, digital wallets, and peer-to-peer platforms create opportunities for financial inclusion, yet they also attract sophisticated fraud schemes. Cybercriminals increasingly exploit API weaknesses, unsecured endpoints, and third-party integrations to compromise accounts.

Phishing, malware, and business email compromise attacks have risen, often targeting high-net-worth individuals and corporate accounts. The adoption of cryptocurrency and blockchain-based payment methods introduces further challenges, as the decentralised nature of these platforms can hinder traceability. Regulators and financial institutions must anticipate evolving threats by adopting predictive analytics and artificial intelligence in monitoring systems.

Training staff to recognise atypical patterns, conducting regular penetration testing, and enforcing multi-factor authentication are essential steps. Additionally, partnerships with cybersecurity firms can enhance real-time threat detection and incident response. Without proactive measures, rapid fintech growth risks outpacing security controls, potentially reversing gains in financial inclusion and public trust. Strengthening the security architecture and integrating risk intelligence across all digital platforms is critical to sustaining a resilient financial ecosystem that can adapt to both technological advances and increasingly complex fraud tactics.

Collaboration and Data Sharing for Industry-Wide Resilience

Effective fraud prevention in Nigeria depends not only on institutional controls but also on robust inter-agency collaboration. Financial institutions, regulators, and law enforcement must share intelligence and coordinate responses to emerging threats. Currently, fragmented data systems hinder timely detection and response, allowing fraudsters to exploit gaps between institutions.

Establishing a unified reporting mechanism can centralise alerts on suspicious activity and improve transparency. Public-private partnerships can also strengthen capacity, enabling smaller banks and fintechs to access tools and insights available to larger players.

Data analytics platforms aggregating cross-institution transaction data can identify emerging patterns of abuse and predict potential attack vectors. Industry-wide drills, simulation exercises, and continuous knowledge sharing will help stakeholders respond more quickly to incidents. Furthermore, harmonising regulatory standards across federal and state levels ensures consistency in enforcement and reduces loopholes. By fostering collaboration and building an ecosystem of shared responsibility, Nigeria can enhance its defences, reduce repeat attacks, and create a resilient digital financial sector capable of sustaining growth while minimising exposure to fraud.

Conclusion.

Nigeria’s digital payments have expanded rapidly, unlocking efficiency and broader financial access, but security has not kept pace. While recent regulatory interventions show measurable progress, the system remains exposed to evolving fraud risks. The next phase of growth will not be defined by innovation alone, but by the strength of the controls that support it. Real-time monitoring, strict compliance enforcement, and coordinated intelligence sharing are no longer optional; they are foundational. Institutions that embed security into their growth strategy will lead; those that do not will bear the cost. The future of Nigeria’s financial ecosystem depends on closing this gap decisively.

References:

- Central Bank of Nigeria (CBN). (2024). Annual report on payment systems and financial inclusion. Abuja: CBN.

- Economic and Financial Crimes Commission (EFCC). (2024). Banking fraud statistics report. Abuja: EFCC.

- Nigerian Deposit Insurance Corporation (NDIC). (2024). Fraud risk assessment in Nigerian banks. Abuja: NDIC.

- Central Bank of Nigeria (CBN). (2025). Digital payments and fraud mitigation report. Abuja: CBN.

For more information, clarifications and support, Contact Prof. Prisca Ndu on +234 902 148 8737 or [email protected]

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp