The Central Bank of Nigeria (CBN) raised the lending rate from 13 percent to 14 percent on Tuesday, July 19, 2022, citing increased inflationary pressure brought about by the Russia-Ukraine war, and the need to correct financial imbalances in the economy.

Other reasons for the rate hike decision were to drive economic recovery and respond to the global interest rate hike, as shown by the 75 basis point increase carried out by the Jerome Powell-led US Federal Reserve Bank. The US Federal Reserve agreed that an interest rate hike would help to mop up excess money in circulation and drive attention towards strengthening the US dollar.

The the CBN’s raise does not only represent a 100 basis point increase but marks the second time an adjustment in interest rates will be used as an effective weapon to achieve its objectives in six years.

Just as the US Fed chairman did, Godwin Emefiele saw the need to raise this interest rate to address accelerating food inflation, which the National Bureau of Statistics (NBS) regarded as the highest in ten months.

Nigeria’s economy responded to the rate hike as expected, with the manufacturing sector complaining of an upward adjustment to the loan repayment. Apparently, both the cost of production, the amount paid by consumers for finished goods and dollar scarcity has hit hard the economy.

Read also: CBN rate hike ignites sell pressure on stocks

“The adjustment, even though expected, will cause manufacturers to shift upwards their selling price,” Charles Eneanya, a macroeconomics research analyst at Reasearchitlive; said, believing that manufacturers will have to increase the selling prices of their goods.

He added that “they would find it challenging to service their debt commitment with the existing lending rate, following upward adjustments commercial banks will make to existing loans and future loans they give out.”

Investment in financial securities will become more rewarding following the rise in interest rates. With the upward review of the Monetary Policy Rate, interest on Treasury bills and other government short-term securities will rise, making it attractive for Nigerians to invest.

According to the CBN, as of Wednesday, July 27, 2022, the interest rate offered on the 91-day Treasury Bill was 2.8 percent a 5 basis point increase from the previous rate of 2.75 percent, while the 182-day and 364-day T-bills were 4.1 percent and 7.0 percent, respectively, a steady rise of 10 basis point for the 182-day bill with the 364-day staying unchanged.

“We can expect the increase in interest rate to continue in the next T-bill auction, especially since the higher borrowing costs are usually associated with higher offered interest rates for financial instruments,” Joel Ighodalo, financial analyst at FBNQuest, said, acknowledging the impact the adjusted interest rates will have on Treasury Bills soon.

Ighodalo believes that the government will be able to mop up so much money from the system through this singular exercise. After all, reducing the amount of money in circulation is its objective.

Another important point about the new interest rate is its impact on borrowing. The immediate effect is that it will push the cost of borrowing even higher. Borrowing costs from financial institutions such as commercial banks, discount houses, financial technology (FinTech) companies, and other uncategorised borrowing houses will increase as their interest rates go up.

Stanley Nwani, a senior economics lecturer at Pan Atlantic University, Lagos, said that the new rate would drive borrowing costs higher. “We expect interest rates on loans to increase,” Nwani said.

He agreed that commercial banks’ interest rates on market-determined loans would increase sharply. For example, the double-digit interest rate on loans would go up to accommodate the change in the CBN lending rate.

“I believe that most commercial banks will have to inform their customers, especially their micro, small, and medium-scale (SME) customers, of a change in interest rates,” he added.

“So, if your company is paying 18 percent as interest on an existing loan, then the company should expect a letter from the bank telling it that market conditions have changed and that the current rate will be moved upwards to accommodate this new rate from the CBN,” he explained.

Another outcome of the lending rate increase will be an interest rate fight between commercial banks and other financial institutions to offer better interest rates to those willing to save their money through fixed deposits (FD) and those willing to leave their monies in their savings accounts.

Before now, interest rates attached to most FDs in commercial banks were unattractive as people looked for better investment alternatives such as cryptocurrencies, stocks, and high-yield investment (HYI), a.k.a. Ponzi schemes, just to multiply their money.

“Expect the FD books for most commercial banks to increase because of the number of FDs that will be booked,” Ighodalo said, referring to the expectations most commercial banks will have on what should happen to their FD balances when the rate comes into full effect.

One outcome that is most likely inevitable is its impact on the prices of everyday food items. We should expect the price of everyday food items to go up.

Manufacturers will increase the prices of their goods sold in the market to cover the new interest rate. Not forgetting the already worsening situation most manufacturers are struggling with on a daily basis.

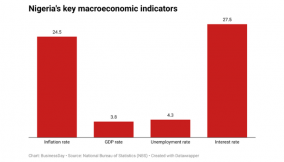

From the dollar shortage to the electricity challenge and others, this new rate will add to the cost of carrying out business. But one thing that is unavoidable is that food inflation of 20.6 percent, as reported by the Nigerian Bureau of Statistics, for the month of June,2022 will skyrocket further.

“One thing that we cannot run away from is the fact that things will become even more expensive following the changes this new rate will have,” Eneanya said about how he expects everyday food items Nigerians depend on to survive to increase.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp