When the United Kingdom was weighing the decision of whether to exit or remain in the European Union, 300 leading business leaders came together to sign a joint statement published in the Financial Times of London.

In that statement they showed rare unison in calling for the UK to leave the EU. They argued that the EU’s red tape “stifles” the country’s businesses and Brexit would create more jobs.

Britain would eventually leave the EU, and that singular act of camaraderie by top CEOs in the country played no small role in convincing the authorities that leaving the EU was the right step for Britain.

Away from Britain to Africa’s most populous nation, Nigeria, and there’s a brewing socio-economic crisis that has the making of the worst crisis since 1999, when the country transitioned to democratic rule.

It may take an ‘unusual’ conglomeration similar to what happened in the UK during Brexit to drive the point home to the government that Nigeria is at the very precipice of a rare economic meltdown.

The signs that Nigeria is already facing the worst socio-economic meltdown of a generation are ominous.

Ibadan is the latest Nigerian city where protests are being held over the economic hardship caused by the bold but ill-thought-out economic reforms of President Bola Tinubu.

In the last week, there have been protests in several parts of the country from the second largest city, Kano, to south-western states Osun and Ogun over a cost-of-living crisis exacerbated by the removal of petrol subsidies and the freefall in the naira exchange rate.

Labour unions have declared a two-day nationwide mass protest slated for February 27 and 28 over the biting economic hardship in the country.

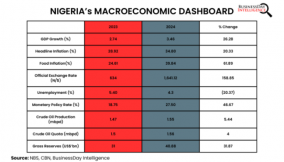

Latest unemployment data shows Nigeria’s unemployment rate rose yet again, and inflation numbers showed the prices of goods and services are moving at their fastest clip in over 18 years, hitting a record 29.9 percent in January, according to the National Bureau of Statistics (NBS). The cost of food, which Nigerians spend the bulk of their income on, rose 35.41 percent in January as against 33.93 percent in December.

Households are increasingly unable to survive and companies are declaring rare losses. Take Nigerian Breweries, the country’s largest brewer, which reported its first loss in at least six years in 2023 due to the 40 percent depreciation of the naira.

The currency has plunged by a further 30 percent this year, making it one of the world’s worst-performing currencies in 2024.

The naira crash has resumed this week after some days of stability following the Central Bank of Nigeria’s (CBN) measures to boost dollar liquidity. While the currency tumbled to N1,598 per USD in official trading on Monday, it fell to a new low of N1,730 per USD on the streets.

The gap between both rates, which had fallen to less than 2 percent last week, is widening again and is now over 10 percent, creating an incentive for round-tripping once again.

Business leaders expect exchange rate-related losses to pile up as the currency volatility persists.

Meanwhile, the insecurity in the North is fanning fears of a severe food shortage and only last week the Sultan of Sokoto, considered the spiritual head of Nigeria’s vast Muslim population, said the country was “sitting on a keg of gunpowder” in his description of the economic crisis in the country.

BusinessDay polled a number of top business leaders, experts and stakeholders to proffer solutions to the country’s economic mess.

Peter Englisch, global family business leader at PwC

“The insecurity is a real challenge and the full impact on businesses and investments is slipping under the radar. Perhaps it is time for the business leaders to come together with one voice to call for action from the government,” Englisch told BusinessDay.

Kingsley Moghalu, former deputy governor of the CBN

Moghalu argues that not much will work in Nigeria if the government does not lead by example and with the interest of the people at heart.

He said: “Whatever the economic argument for removing subsidies on imported petrol (now apparently restored through the back door to prevent further increases in the price at the pump) and forex, one subsidy stubbornly clings on: the subsidisation of Nigeria’s political class.

“As I commented at the time, spending around N160 million to purchase imported SUVs for each member of the National Assembly when Nigeria was seeking to borrow $1.5 billion from the World Bank sent the wrong signal to Nigerians and investors. Much about our economic problems is beyond economics.

“The subsidisation of the lifestyles of Nigerian politicians must end before Nigerians can be persuaded on the economics of subsidy. Again, as one has noted, there is of course a whole separate argument about how competently the subsidies removal was handled. Subsidising an effective nationwide public transportation system at a fraction of the cost of the petrol subsidy would have been the smart economic choice, given our poor fiscal situation. Most economically developed and emerging market countries of the world do this.

“The subsidies had to go because there was just no choice. But it’s not just about subsidies per se. It’s more about what is subsidised and how. N500 billion a year can subsidise a public transport system nationwide. That’s different from N5 trillion a year for a fraud-ridden scam,” Moghalu said.

Charles Robertson, an economist

Robertson, head of macro strategy at asset management firm FIM Partners, has been a long advocate of improving adult literacy in Nigeria to attract private investments and create badly-needed jobs.

He lauded the liberalisation of the FX market but cautioned against government borrowing from the CBN as it will further stoke inflation and worsen the plight of the poor.

He said: “The long-term answers are ensuring everyone can read and write and kids attend school until 18 and I’d argue, focusing health care provision on cutting child mortality and a government information campaign to explain that the old truth (big families make you wealthy because there are more hands to work in farming) is not true in a knowledge-based economy – fewer children with more education is what makes your family wealthier.”

“But in the short-term, I’d argue a very strong focus on basic security is essential. No one invests in a country where kidnapping is rife.

“Second, achieve a currency level that means Nigerians have to buy Nigerian goods, not imports. That has been achieved.

“Third, stop printing money to pay government bills — all this does is add inflation and makes the poor worse off and sends the currency weaker.

“Given Nigeria’s debt/revenues ratio, the government cannot do more to help, but maybe it can spend better, even if it can’t spend more.”

Kelvin Emmanuel, CEO of Dairy Hills

Emmanuel proffered a solution to increasing food supply and he had the following to say:

“We need to work on the implementation of the backward integration programmes for wheat, sugar, milk through the utilisation of the backward integration levy.

“We also need to work on developing horizontals and verticals for enterprise manufacturing to reduce the dependencies of consumer manufacturers on letters of credit for importation of inputs (a key focus should be on giving partial waivers for capital equipment imports, granting pioneer status, reforming the export expansion grant to only companies that beneficiate to a secondary derivative).

“Because transport cost plays an important role in the price of food (imported and locally produced), developing a railway network for moving cargoes is critical to balancing the cost of transportation across regions (diesel, road extortion, accident insurance, spare part changes).

“The solutions are not unknown. If the President is not getting results from the team he has entrusted to execute on these items above, maybe it is time to change them.”

Bill Gates, founder of Microsoft and world’s second richest man

Gates argues that the government needs to deploy its limited capital better by investing in people and infrastructure.

“To anchor the economy over the long term, investments in infrastructure and competitiveness must go hand in hand with investments in people. People without roads, ports, and factories can’t flourish. And roads, ports, and factories without skilled workers to build and manage them can’t sustain an economy,” he said.

A business leader

As a solution to the severe dollar shortages that have resulted in the sharp fluctuation of the naira, a notable business leader who did not want to be named recommended that Nigeria should consider tapping the International Monetary Fund (IMF).

“I think we should go to the IMF, borrow $30 billion from them and institute a comprehensive reform program. All this drip feeding of incremental reforms isn’t it.

“In the meantime we can start seriously fighting inflation (which we aren’t doing now), temper government expenditure, make the country more friendly to business, be serious in tackling insecurity and develop a proper long term growth plan.”

A business leader

Another anonymous business leader was of the view that better coordination of fiscal and monetary policies will deliver better economic results. He went on to recommend setting up a global economic advisory team that includes notable Nigerians in diaspora.

“There needs to be better coordination of fiscal and monetary policy. There is need for full transparency from NNPC in terms of actual production figures and the amount that is encumbered in forward sales.

“We need to also consider setting up a global economic advisory team that will include people like Adebayo Ogunlesi, and Ngozi Okonjo-Iweala.”

Everyone polled in our survey agreed that Nigeria was indeed flirting with the worst social crisis since 1999 but were convinced the government can avert the situation with the right policies if only action is taken urgently.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp