African economies are facing renewed cost pressures after Iran closed the Strait of Hormuz again on Saturday, April 18, reversing a reopening that lasted less than a day and briefly eased global oil markets.

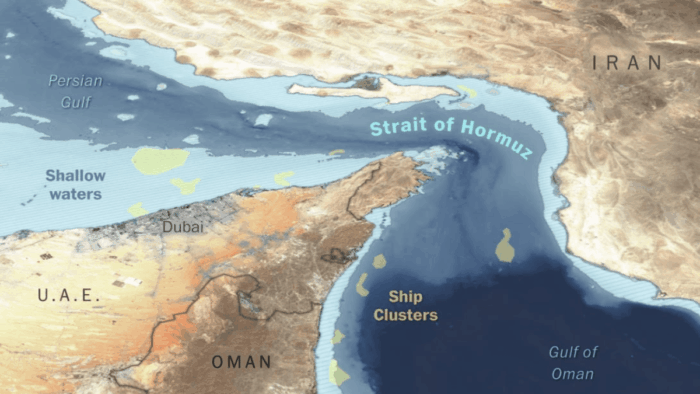

The latest escalation follows a rapid sequence of events tied to a wider conflict that began on February 28, when fighting between Israel and Lebanon intensified and spread across the region. Since then, the Strait of Hormuz, which carries about 20 percent of global oil supply, has emerged as a central pressure point in the crisis.

On Friday, April 17, Abbas Araqchi, Iran’s foreign minister, announced that the strait was “completely open” to all commercial shipping during a ceasefire linked to Israel’s agreement to halt fighting with Lebanon. Iran said the passage would remain open for the duration of the truce.

Markets reacted immediately. US crude fell 9.4 percent, while Brent crude dropped 9.1 percent on the day, as traders priced in reduced supply risks. The sharp decline marked one of the steepest single-day drops since the conflict began.

Donald Trump, US president, welcomed the development, writing that the strait was“Completely open and ready for business.” However, he added that a US naval blockade targeting Iranian exports would remain “in full force” until negotiations were concluded.

That optimism proved short-lived. By Saturday, April 18, Iran reversed course, announcing it was closing the strait again, citing what it described as US “breaches of trust” linked to the continued naval blockade. Iranian forces moved to restrict access, sharply escalating tensions within hours of the earlier reopening.

Read also: World in Brief: US seizes Iran ship, Canada warns on reliance, Kenya seeks bailout and other stories

According to reports, Iranian gunboats fired on tankers attempting to pass through the waterway, while US forces responded by firing “several rounds” at an Iranian-flagged vessel. The US military later seized the cargo ship Touska, according to US Central Command.

Trump described the action as a “violation” of the ceasefire, stating that “our blockade has already closed the Strait of Hormuz.” Iran’s military warned it would retaliate, calling the seizure “armed piracy.”

Markets reacted swiftly to the renewed disruption. US crude rose 5.6 percent to about 88 dollars a barrel, while Brent crude climbed 5.3 percent to above $95 a barrel. By Monday, April 20, Brent was nearing $97, and US crude was around $90 as traffic through the strait remained severely restricted. No tankers crossed the route on Sunday, according to shipping data.

For Africa, the consequences are immediate and far-reaching.

Most African economies are net importers of refined petroleum products, leaving them highly exposed to global oil shocks. Rising crude prices feed directly into higher fuel import costs, currency pressure, and broader inflation.

In Nigeria, inflationary pressure is already building as import costs rise, with recent figures showing inflation at 15.38 percent. Across East Africa, the strain is more visible.

In Ethiopia, Abiy Ahmed, the Prime Minister, has urged citizens to conserve fuel as shortages deepen. The government has directed public institutions to scale back operations, placing non-essential workers on leave. The country consumes about 103,000 barrels of oil per day and spends more than $4.2 billion annually on fuel imports.

Read also: US-Iran ceasefire puts pressure on Maser Group’s $150m Oil trade

In Kenya, Opiyo Wandayi, Energy Cabinet Secretary, warned against fuel hoarding, calling it “an economic crime,” as authorities attempt to contain price increases. In Tanzania, regulators have raised petrol price caps by 33 percent, while in Somalia, fuel prices have nearly doubled, pushing up transport and food costs.

Economists say the stop-start disruption in the Strait of Hormuz is particularly damaging, creating volatility that makes it difficult for import-dependent economies to stabilise fuel pricing.

Fuel sits at the centre of economic activity. Higher oil prices increase transport costs, raise the cost of electricity generation, and push up the price of basic goods, including food staples such as bread.

With a fragile US-Iran ceasefire set to expire this week and tensions still high, uncertainty remains elevated. The reopening on April 17 offered brief relief. Its closure on April 18 has reinforced a harsher reality.

Global shocks may shift quickly, but their impact on Africa’s cost of living is slower to fade.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp