Reaction of investors to the stocks of Airtel upon listing on the London stock exchange market (LSE) is believed to signal a likely behaviour of Nigeria’s high net worth individuals (HNI) and institutional investors towards firm’s listing on the Nigeria stock exchange market (NSE).

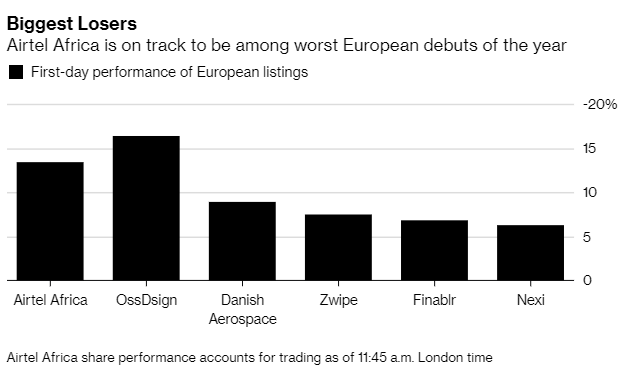

As at the close of trading on Friday, stock price of Airtel Africa slumped steeply by 16 percent on its first day of trading, hence joining the list of worst debuting stocks in Europe.

Airtel stocks which were valued at 80 pence dipped to 67 pence as at the close of trading on Friday on the LSE.

“The sad decline of the first day of trading reflects lack of interest in the stock. This can be attributed to a number of factors ranging from their historical performance in which they have recorded losses,” Gbolahan Ologunro, Research Analyst at CSL; stockbrokers told BusinessDay.

“Also they have high financial leverage which is higher than its peers when we look at their debt to equity ratio,” Ologunro added.

While Airtel may have highly leveraged balance sheet compared to peers, analyst believe that a more attractive valuation multiple could have bred a better response from investors towards shares of the telecommunication firm.

Against the expectation of a similar excitement towards the shares of MTN Nigeria on that of Airtel, analysts believe that the negative reaction from foreign investors on the LSE is an eye opener for Nigerian investors who are largely driven by sentiment on the possibility of Airtel’s share being pricey.

Concerns have been raised over the possibility that investors perceive a threat to future earnings of the company on the back of an issue which isn’t sufficient enough to improve the finance cost of the firm, hence hinder anticipated returns.

Airtel Africa, a unit of India’s Bharti Airtel Ltd, last week set a price range of N363-N454 per share for its IPO on the NSE where it aims to issue 501 million to 716 million new shares and selling about 500 million shares on the London stock exchange (LSE) market with 10 percent over allotment option.

The proposed listing of Airtel is said to imply a TTM EV/EBITDA multiple of 6.3x – 6.8x, implying that for every N1 EBITDA made investors are willing to pay between N6.3 to N6.8 own the shares.

Airtel had claimed it planned to raise $750 million, despite highly leveraged with a debt-equity ratio of 2.0x and an outstanding debt obligation of about $3 billion.

This means that its debt obligation when shares are fully subscribed to will drop to about $2.25 billion while debt to equity to about 1.7x.

“This is still very high and doesn’t make a difference, now leverage stocks in the market generally trade at a discount to peers because of the leverage risk and impact on ROE,” Ayorinde Akinloye, equity research analyst at CSL Stockbrokers explained.

Meanwhile the big question remains whether or not Airtel is under-priced or pricey.

Amongst peers like Safaricom with Return on Equity (ROE) OF 46.6 percent and EV/EBITDA of 8.6x, Vodacom (20.8%, 7.8x), Airtel with an ROE of 18.5 percent suggests to be traded at a price lesser than that of Safaricom and Vodacom.

Also, compared to MTN Nigeria with a ROE of 65.4 percent higher than ROE of MTN group at 6.8 percent, this suggests MTN N should be priced at a premium to Airtel but currently trades at 6.2x EV/EBITDA which is discount to that of Airtel stated earlier.

“For foreign investors who are holding or bidded for Airtel shares on the LSE, they may want to cash out in the Nigeria upon listing hence reduce the extent of their lost since it’s a dual listing,” Ologunro stated.

David Ibidapo

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp