As of today, the nation’s capital market is in the negative territory as bearish sentiment hovers around investors’ decisions. Despite the uncertainties in the capital market, some private and institutional investors are betting on equities as they anticipate a future rise in prices.

Based on the alpha capture in April 2019 in the report prepared by analysts at Rand Merchant Bank (RMB) Nigeria Limited—a leading African corporate and investment bank, the report focused on the key elements that will tip the balance of their banking coverage for investors to leverage on in 2019. The bank which has over 10 years of transactional experience outlined 4 major factors that might affect stability in the equity market in 2019:

• declining yields on government securities

• the recent 50bp cut in the Central Bank of Nigeria’s Monetary Policy Rate (MPR)

• the outlook for cost of risks coverage

• regulatory uncertainty

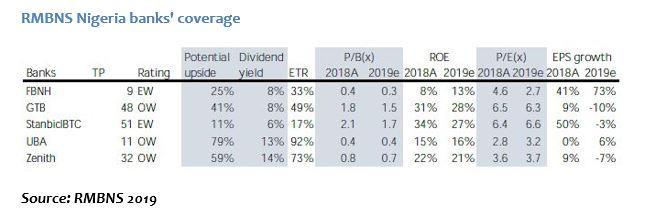

Although, it is believed that the current valuation of Nigerian banks is unjustifiably cheap, these stocks hold much prospect when compared with Kenyan banks which have 1.2x and 19 per cent of return on equity (ROE). Consequently, RMB’s five coverage banks which are First Bank of Nigeria Holdings (FBNH), Guaranty Trust Bank (GTB), Stanbic IBTC, United Bank for Africa (UBA) and Zenith Bank remain attractive at 0.9x for 2019e Price to Book ratio (P/B) and 21 per cent ROE even as it anticipates an average total return of 53 per cent inclusive of a 10 per cent dividend yield.

Opportunity exists for investors as the coverage banks have a P/B range of 0.3x for FBNH and 1.7x for Stanbic IBTC. It should be noted that FBNH with a target price of N9 has potential for growth subject to the resolution of its case with Atlantic Energy (AE).

“We also think FBNH (Equal Weight(EW), N9) is a stock that investors should keep an eye on given its potentially strong earnings growth and profitability contingent on the resolution/write-off the AE loan”, said analysts at RMB.

RMB Analysts’ forecasts showed that the valuation of assets would appreciate to N11 when the cost of risks was reduced from 6 per cent to 4.5 per cent; and even to a higher N13/share when the cost of risks was normalised at 2.5 per cent over the forecast period.

Treasury and asset yields environment have already been priced lower in 2019e as a 100bp year-on-year (YoY) declined in average yields to 14.7 per cent was modelled even as treasury assets accounted for 53 per cent of the coverage banks’ interest-bearing assets.

In 2019, he cost of risks is expected to be higher by 40bp to 1.6 per cent; normalised earnings showed 10 per cent growth while 2 per cent decline in earnings is expected with exclusion of FBNH and Access Bank within the coverage universe. The aforementioned banks currently trade on an average of 2019e, P/B of 0.9x with an average 2019e ROE of 21 per cent.

This trails the Kenyan banks’ valuation for 2019, P/B of 1.2x, ROE at 19 per cent, Middle East and Africa (MEA) banks which have for 2019, P/B of 1.3x and ROE 18 per cent.

Valuation of Nigerian banks in comparison to Kenya’s and MEA

Using ROE as the major driver of valuation, findings by analysts at RMB revealed that banks trade at a discounted 38 per cent and 29 per cent to fair value based on MEA and Kenyan banks’ ROE-adjusted valuations.

Analysis from the table above revealed that the most undervalue banks are FBNH at -60 per cent discount, UBA at -64 per cent discount and Zenith at -48 per cent discount.

On the assumption that the risk-free rate of Nigerian and Kenyan markets are similar, the analysts believed that Kenyan banks are closer comparable to the Nigerian banks with both countries having a 10-year bond yield of about 13 per cent and 14 per cent respectively. This informed the conclusion that the Nigerian banks remain cheap from relative standpoint, despite the headwinds.

With preference for GTB that is trading at a 2019e, P/B of 1.5x with an expected ROE of 28 per cent, Zenith Bank, trading at a 2019e, P/B of 10.7x with an expected ROE of 21 per cent, and UBA that is trading at a 2019e, P/B of 0.4x with an expected ROE of 16 per cent.

This is due to the overweight (OW) rating with a TP of N48, N32 and N11 respectively, on a risk-adjusted basis over the next 12 months with potential upsides of 41 percent, 59 percent, and 79 percent respectively from the current levels. While FBNH, equal-weight (EW) with a TP of N9 is a stock to watch based on observable milestones relating to AE credit resolution, it also has an upside from the sale of Ontario downstream assets.

The current valuation prices of these banks are attractive as potential total returns inclusive of dividend yield on GTB hover about 8 per cent; Zenith, 14 percent, and UBA with dividend yield of 11 percent could post returns as much as 49 percent, 73 per cent and 92 per cent respectively.

Although the three banks are OW, GTB has strong profitability despite normalising income; Zenith is under-priced with decent yields and UBA African subsidiaries are expected to drive strong loan growth in 2019.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp