The Central Bank of Nigeria’s (CBN) proposed banking reforms could quietly end one of the biggest structural distinctions in the country’s banking industry by requiring standalone lenders such as Zenith Bank, United Bank for Africa (UBA) and Fidelity Bank to adopt financial holding company (HoldCo) structures.

For more than a decade, Nigeria’s banking industry has operated under two distinct corporate models. Institutions including Access Holdings, GTCO, First HoldCo, FCMB Group, and Stanbic IBTC Holdings have reorganised into non-operating holding companies, allowing them to own commercial banks alongside insurance, pension, payments, asset management, and other financial services businesses.

Others, including Zenith Bank, UBA, and Fidelity Bank, have largely retained the traditional banking structure, with the operating bank sitting at the apex of the group and directly owning its banking and non-banking subsidiaries. The CBN’s latest exposure draft suggests that distinction may soon disappear.

According to the Renaissance Capital Africa report titled “Nigerian Banks: More Capital, Declining Returns,” Section 4.6 of the proposed guidelines requires closely linked entities to be housed under a single non-operating holding company.

Although the draft does not explicitly mention standalone banks, the investment bank says there is no exemption for institutions that own non-bank businesses or foreign subsidiaries, effectively bringing them within the HoldCo framework.

From optional strategy to regulatory expectation

The HoldCo structure was introduced by the CBN in 2014 following sweeping banking reforms that separated commercial banking from other financial services businesses.

Rather than allowing banks to directly own insurance companies, pension managers, payment firms, and investment businesses, the framework created a non-operating parent company that oversees all subsidiaries while leaving banking operations within a separately regulated institution.

The structure has since been adopted by some of Nigeria’s largest financial groups. Access Bank transitioned into Access Holdings in 2022, GTBank became GTCO in 2021, FBN Holdings recently rebranded as First HoldCo, while FCMB Group and Stanbic IBTC Holdings have operated under similar structures for years.

Those institutions expanded beyond traditional banking into broader financial services using the HoldCo model. Zenith Bank, UBA and Fidelity Bank, however, remained outside that framework, continuing to operate with the banking entity as the parent company.

The exposure draft signals that the regulator now wants a single governance model for banking groups.

Foreign subsidiaries move to the top

One of the biggest changes proposed in the draft is the transfer of ownership of foreign subsidiaries.

Rather than sitting directly under the Nigerian operating bank, overseas banking operations would be owned by the HoldCo or an intermediate holding company established specifically for international subsidiaries.

According to Renaissance Capital, this fundamentally changes the role of the operating bank because it would no longer control the group’s foreign operations.

The investment bank argues that once foreign subsidiaries are transferred, the rationale for maintaining an international banking licence at the operating bank level becomes significantly weaker.

It therefore expects many banks with sizeable African operations to eventually downgrade from international banking licences to national licences, which require significantly lower minimum capital.

Standalone banks face a two-step transition

For Zenith Bank, UBA, and Fidelity Bank, compliance would begin with corporate restructuring rather than capital raising.

Renaissance Capital expects the lenders to establish non-operating HoldCos through share swap arrangements, allowing shareholders to exchange shares in the operating bank for shares in a newly created parent company.

Only after that restructuring would the new HoldCos become subject to the proposed capital framework, requiring holding companies to maintain capital equivalent to 1.2x of the combined paid-up capital of their subsidiaries.

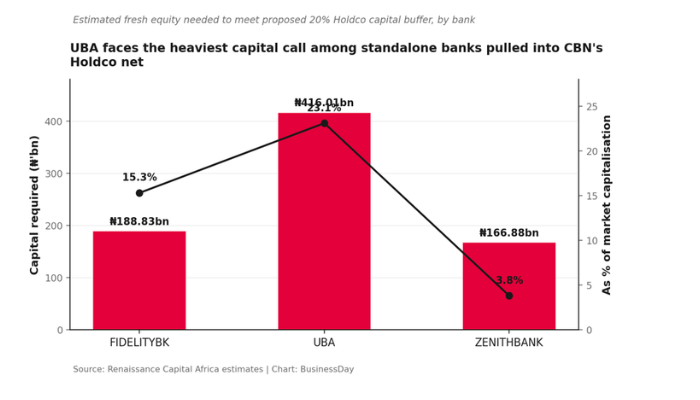

Based on its analysis, Renaissance Capital estimates that UBA could require about N416 billion in additional equity, Fidelity Bank around N189 billion, while Zenith Bank may need approximately N167 billion to comply with the proposed framework.

“This will lift each group’s Holdco capital coverage ratio from 0.9x, 0.7x, and 0.9x today to the prescribed 1.2x. This is the mechanism through which the guidelines would ultimately draw banks that currently operate outside a holding company structure into the additional capital requirement.

“We see ZENITHBANK clearing the hurdle comfortably, its NGN166.88bn raise equating to just 3.8 percent of market capitalisation, whereas UBA faces the heaviest lift given its larger absolute requirement,” the report added.

Existing HoldCos are not spared

While Zenith Bank, UBA, and Fidelity Bank would first have to create holding companies, banks already operating under the model also face significant implications.

Access Holdings, GTCO, First HoldCo, FCMB Group, and Stanbic IBTC Holdings would not need to undertake another corporate restructuring, but they would still be required to meet the proposed 20 percent HoldCo capital buffer.

Renaissance Capital estimates that Access Holdings faces the largest capital requirement under the proposal at approximately N669 billion, followed by FCMB Group with N267 billion, First HoldCo with N243 billion, GTCO with N211 billion, and Stanbic IBTC Holdings with about N84 billion.

The proposed requirements come barely months after Nigerian banks completed the CBN’s latest recapitalisation exercise, raising fresh equity to meet new minimum capital thresholds.

The biggest question remains unanswered

Although downgrading to national banking licences could potentially free up excess regulatory capital, Renaissance Capital says the proposal leaves one critical issue unresolved.

It remains unclear whether banks will be allowed to recall and redeploy the excess capital released from their operating banking subsidiaries once foreign businesses have been transferred to the HoldCo.

“The key open question is whether the excess capital of the banks would be recalled and used as cash for redeployment across the group or returned to shareholders, or whether it remains trapped at the subsidiary level,” the report said.

According to the investment bank, the answer could determine whether the new framework enhances shareholder value or simply results in more capital being locked inside non-operating entities.

Join BusinessDay whatsapp Channel, to stay up to date

Open In Whatsapp